If you've read any of our other articles that go into detail about various techniques or strategies to address retirement income planning, you’re probably not shocked that we believe it is a significant discussion. And quite honestly, we believe this is one of the biggest boondoggles for financial advisors, investment companies, and life insurance companies.

The financial services industry has largely dropped the ball with educating and informing consumers on how to think about retirement income planning.

The demand for knowledge, strategy, and tactical advice about retirement income planning has never been greater than it is today. Our industry must help our clients distribute their accumulated wealth conservatively, so as to maximize how long their money will last. And we must also help our clients manage their retirement income efficiently so that they are able to minimize the impact of taxes.

Planning Retirement Income Should Be Your Focus

For years, nobody talked about it…at all. The industry was laser-focused on gathering assets and helping folks accumulate wealth. As we mentioned many times before, incentives matter, and the incentives have been that the industry largely generates revenue by gathering and accumulating not by helping clients plan for retirement income distribution.

When you look at the issue of income distribution in retirement income planning, there are actually a couple of broad issues at play here:

- Help clients determine their longevity risk—how long will the money last

- Assist them in the distribution of their assets in the most tax-efficient way possible—which pile do I draw from first

Back in 2012, we took a look at a study completed by Conning Research & Consulting. The study was titled, “The Big Payout: Individual Retirement Income Opportunities”.

The data that has been released from the study is fascinating, and I’ll admit that I was a bit surprised by some of the numbers.

Their study concludes that almost half (46% to be exact) of all defined contribution assets (think 401k, 403b, etc.) are currently held inside of individual annuity and group annuity contracts. With the dominance and pervasiveness of the mutual fund industry in the last couple of decades, I didn’t expect that high of a percentage of defined contribution assets to be held in annuities.

Now, while all that information is fascinating, it’s just the beginning of the story in my opinion.

Strategies for Retirement Income Planning

Life insurance companies, agents, and brokers have a tremendous opportunity in front of them. We have a chance to help our clients turn those buckets ‘o money into the income they’ll need when they punch the clock for the last time before strolling off into the sunset.

Certainly, we're biased here but…

The insurance industry clearly has the advantage in this war for managing the retirement income streams of our baby boomer clients. We have the products that will guarantee lifetime income and control market volatility. These are two distinct problems that retirees face. Life insurers and their products win both battles—no contest.

Make no mistake though…

The mutual fund industry, investment managers, and big wall street firms are all gunning for the chance to win this fight. They will continue to support ideas like the 4% rule as it benefits them for you to keep your money invested so they can charge asset management fees. We’re talking about trillions of dollars at stake here. Please remember, incentives matter.

99% of the financial websites out there push the investment industry’s agenda (mutual funds and ETFs primarily). Guess who sponsors their content?

Why Life Insurance Companies Win Retirement Income Strategy

Two big reasons life insurance companies can win this battle:

- Life insurance companies offer solutions that guarantee lifetime retirement income. Keep in mind, the purpose of accumulating a large bucket of retirement assets is to generate income during retirement. Don’t be swayed by the advisors and agents out there whining about the fact that annuity yields are too low! Yes, the interest rates and cap rates are low but your focus should be on producing income. You should spend a little time learning how to create your own pension so that you approach retirement with a focus on producing income.

- All life insurance-based solutions, be it, cash value life insurance, fixed annuities, SPIA’s, and/or fixed index annuities help you avoid market volatility. If you haven’t ever studied data concerning the effects of market volatility on retirement income…keep reading. It can absolutely devastate an otherwise happy retirement.

Don’t Allow the Sequence of Returns to Destroy Retirement Income

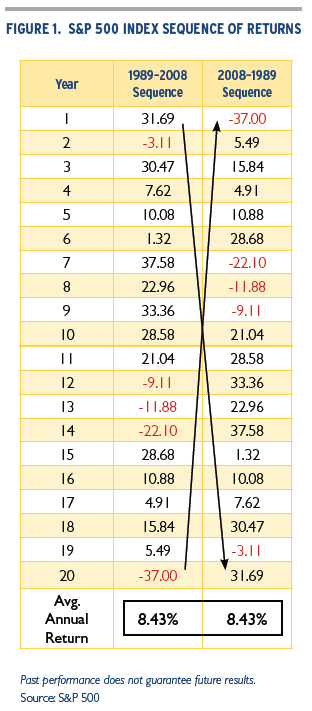

Below you will find a useful graphic to illustrate the detrimental effect sequence of investment returns can have on your future retirement. Take a look at this chart that displays the sequence of returns year by year of the S&P 500 from 1989-2008.

Notice that the average annual rate of return doesn’t change despite the order of returns here.

Simple math…right? Everyone learns in elementary school how to calculate averages.

If you are in the accumulation stage of life, no big deal what order the returns come, you’re not drawing any money out of the market.

But consider the reverse scenario. If you retired in 2008, you would have been down -37%. That means you had three years of losses within your first ten years of retirement.

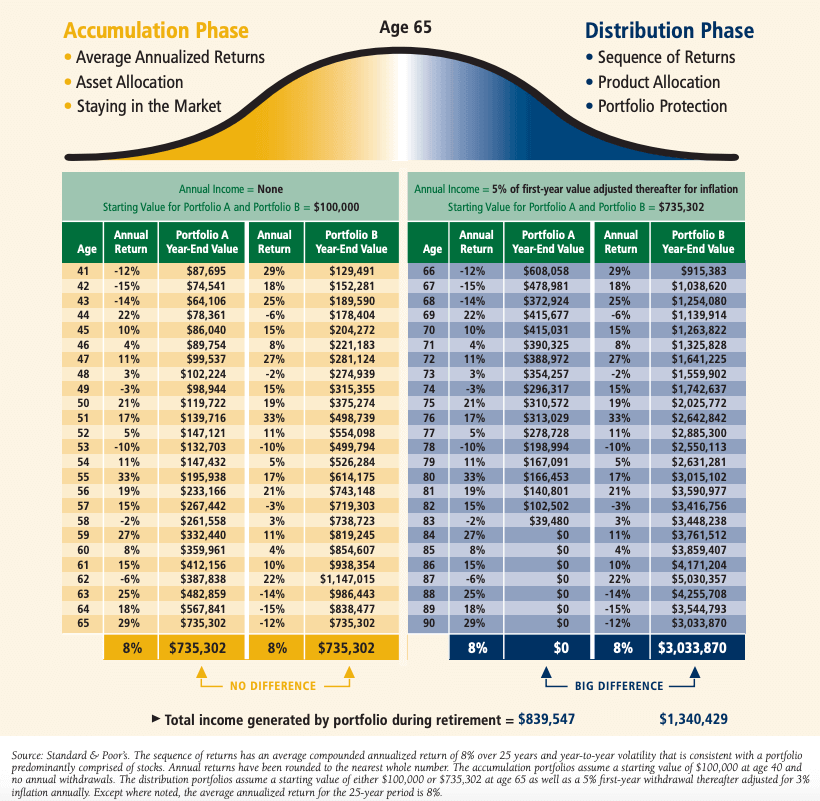

Take a look at the second graphic (credit: John Hancock) here to see what happens to an investment portfolio that is taking retirement income and how the sequence of returns can impact it.

This one is really interesting because you can see how the order of returns inverted has no impact on overall return when you are accumulating retirement wealth. On the right, you can see that when you take the accumulated balance of $684,848, take 5% from the portfolio as an income withdrawal beginning at age 66 and increase the withdrawal for inflation by 3% each year thereafter you run into trouble if the sequence of returns goes against you early in your retirement.

As we’re fond of saying, this idea works until it doesn’t. And in the example depicted in this graphic from John Hancock, sometime between ages 81 and 82, you run out of money.

Do you know what the sequence of returns will be in the future?

Guaranteed Retirement Income Is a Winner

The battle for who wins the retirement income hearts of America is far from over. Using fixed insurance contracts—whole life insurance, fixed annuities, deferred income annuities, single premium immediate annuities, and fixed indexed annuities with guaranteed minimum income withdrawal benefits ensure that scenarios like the one displayed in the charts above never happen to our clients.

Any decent fixed index annuity with a good GLWB (guaranteed lifetime withdrawal benefit) can provide similar if not superior income and with a guarantee that you will never outlive it, in spite of market volatility or the government-engineered low-interest-rate environment we have today.

If you’d like to learn more about how we can help you fight this battle, get in touch with us. We’ve got the tools, expertise, and resources to help you plan for your future retirement income strategy.