If you own a business, you need a clear template to follow for your buy-sell agreement that details the triggering events, how you will fund it, the agreed-upon value of the business, and the structure of the arrangement. But what’s even more important, is that you need to be sure that you fund the agreement with life insurance that is not paid from the corporate checkbook. You could roll the dice, ignore the issue entirely, and just go into business with your partner’s wife when they die but I’ve seen this happen on several occasions—not pretty.

Most who have experience with this predicament would liken it to water-boarding, it won’t kill you but it will most certainly make your life miserable.

Many business owners who haven’t funded their buy-sell agreement fail to do so because they fear the expense of the life insurance policies that are needed to properly fund the agreement. But this should not be a reason to delay the purchase, in fact, the cost of a funded buy-sell (life insurance premium) is peanuts compared to the benefit it provides.

And without one a family business or closely-held business can be in for serious financial and tax pain upon the death of an owner. The life insurance premiums are far less expensive than the potential financial pain.

What is the Advantage of a Cross-Purchase Buy-Sell Agreement?

Please understand that the legal document detailing a cross-purchase buy-sell agreement is very specific and detailed. As such, here we are seeking to offer an accessible explanation at a high level and are not looking to explain all of the many legal facets. The only buy-sell discussion here is the cross-purchase agreement.

This is the most basic type of agreement and it’s a good place to build your foundational knowledge on the subject. It is also the most commonly used buy-sell agreement that we have seen in 20+ years.

Overview of a Basic Cross-Purchase Plan

In a basic cross-purchase agreement, when a business owner dies, the surviving owners agree to buy the deceased owner(s) shares of the business. Each owner agrees to purchase the interest of the other in the event that one of the owners dies.

So, in this scenario, every owner is an applicant, a premium payor, a beneficiary, and an owner of insurance policies on the lives of each of the other business owners.

There’s a graphic below with an example that will help sort it all out for you.

When one owner dies, every surviving owner/beneficiary will receive the insurance policy death benefit. Then each surviving owner pays cash to the deceased owner’s estate or family (depending on how the agreement is set up) and in exchange the estate transfers the deceased owner’s shares of the company.

What results is that the family’s illiquid shares of the company are magically turned into cash and the owners that are still living own all of the business. Everybody wins, the family of the deceased owner gets cash and the surviving owners of the business aren’t forced to be in business with the deceased owner’s family.

What is the Structure of the Agreement?

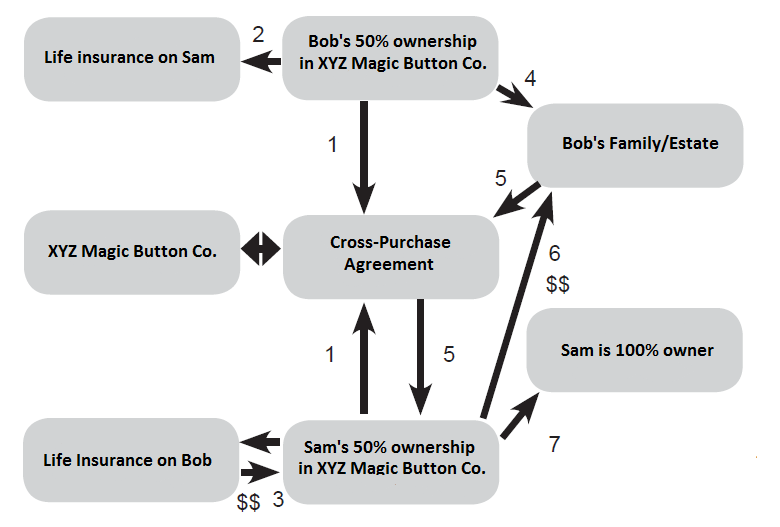

Let’s use Bob and Sam as our example. They own XYZ Magic Button company.

- Bob and Sam establish a cross-purchase agreement between themselves.

- Bob and Sam apply for a life insurance policy on each other. Each one of them is the owner, beneficiary, and premium payor of a policy on the other’s life.

- Let’s assume that Bob dies, the life insurance company pays Sam the death benefit.

- Bob’s shares of XYZ pass to his estate/family.

- Bob’s estate/family sell their shares to Sam under the pre-arranged cross-purchase agreement.

- Sam uses the life insurance proceeds to pay Bob’s family cash for Bob’s shares in XYZ.

- Now Sam owns 100% of XYZ Magic Button Co.

Here’s a picture to illustrate how that happens.

Establishing a Value for the Business

This is one of the most important aspects of the agreement, Sam and Bob have to sit down and fix a value for their company. In order for them to both be sure that the arrangement is properly funded, they both need to have enough life insurance coverage on each other to the “date of death” value of the deceased owner’s shares. There are several ways for them to arrive at a business valuation:

- An appraisal value—which is determined by an independent appraisal at the time the business interest is actually sold

- The Capitalized Earnings Approach—value is determined by an income-based model. It derives the value of the business by dividing the selling party’s discretionary earning by the capitalization rate.

- Specific Fixed Price—the owners fix the price on a regular basis by agreement

- Formula Value—determined formula comprised of several factors that owners agree to in the cross-purchase

- Book Value—the actual book value of the owners’ shares on the date of death

What is the Advantage of a Cross-Purchase Plan?

Well, besides the obvious advantages that I’ve already discussed, there are others that are much more concrete in nature. If Bob dies and Sam purchases all of Bob’s shares per the cross purchase agreement they had in place, Sam receives an increase in the cost basis of the acquired shares that equals the full purchase price.

This is a very good thing for Sam. If later on down the road, he decides to sell all of XYZ Magic Button Company at least half of his shares will have a much higher cost basis which will lessen the capital gains pinch.

Also, there are at least two other advantages that are related, the business is not involved in the buy-sell agreement in any official capacity at all which means

- The business is not forced to reflect the value of the life insurance on its balance sheet. This would cause the value of the business to increase.

- Because the business is not a party to any of the transactions, the life insurance is not subject to Alternative Minimum Tax (AMT) calculation.

Are there any disadvantages?

There are a couple of the things that could complicate matters and make a cross-purchase type of buy-sell agreement not so fabulous.

- If there are too many owners, there can quickly become an obscene number of policies that have to be purchased to make the agreement work. The formula to calculate the number of policies need is N(N-1), where N equals the number of owners. Example: If there were five owners, 20 policies would have to be purchased…seriously? That gets a little out of hand.

- The owners could violate transfer-for-value rules if, in order to fund subsequent buyouts, the decedent’s estate transfers all the remaining policies over to the surviving owners. But there’s much more to this that I just can’t get into here as it’s a topic unto itself.

In the end, it’s always best if you have a competent attorney and/or tax advisor involved in the process of deciding upon the right type of buy-sell agreement your business should have. But if you have a small business with two owners, the cross-purchase buy-sell agreement is probably your best bet.