When a term life policy matures the original premium payment agreement expires and now the policy owner must either pay a higher premium or find another life insurance policy. The overwhelming majority of term life insurance policies issued today are level term policies. These policies have a guaranteed level payment period. Maturity occurs at the end of this level payment period. When this happens, most policies allow the policy owner to continue coverage, but at a substantially higher premium.

Example of 20 Year Term Policy Before and After Maturity

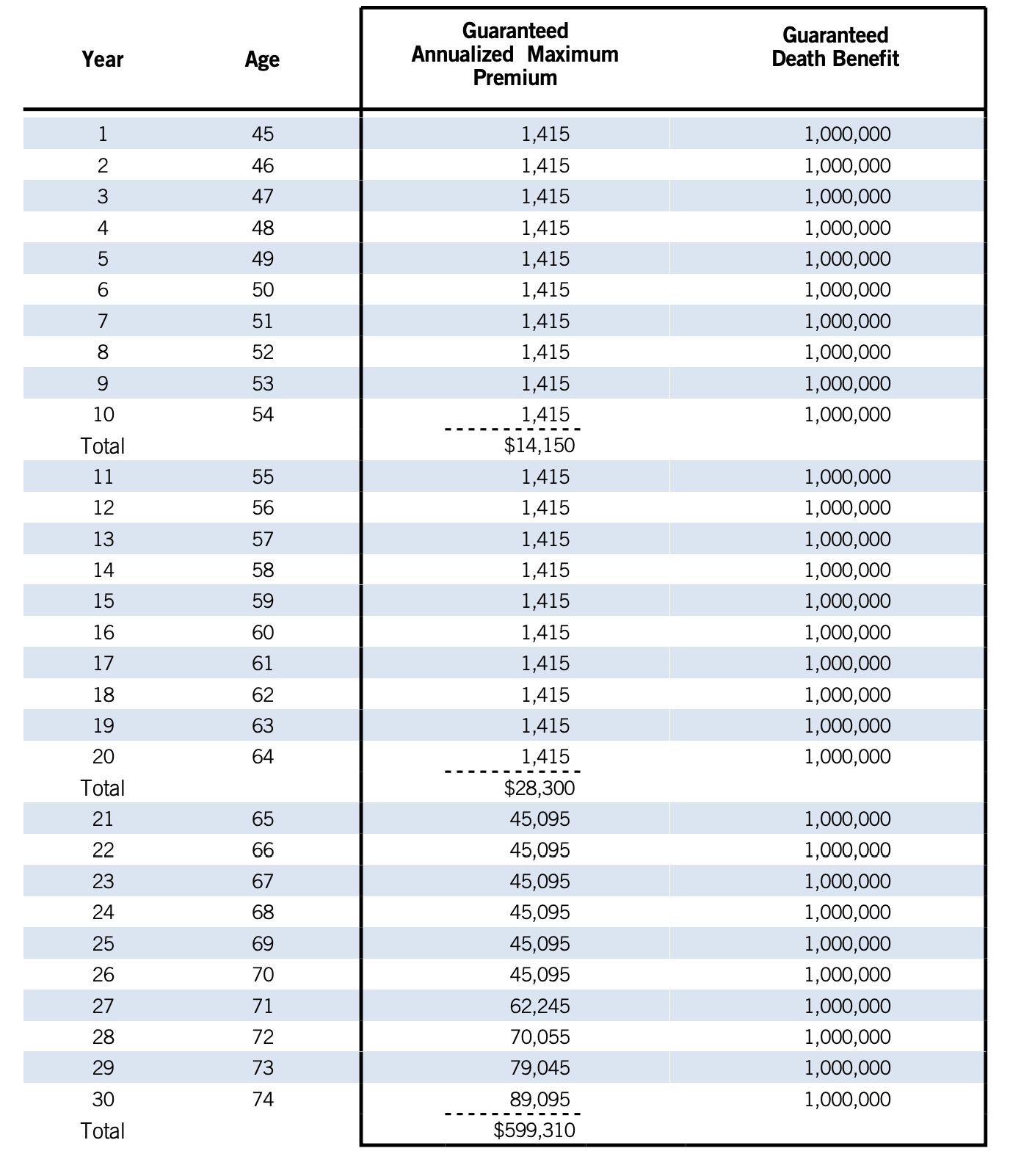

We'll use a male age 45 in our example who is looking for a $1 million death benefit. With one major life insurer, the 20 year guaranteed level premium is $1,415 per year. He can pay that same annual amount for 20 years and he'll keep his $1 million death benefit. After year 20, his guaranteed level period expires and his new premium in year 21 jumps to $45,095. Here's a ledger that details the increases in premium:

Here you can see, this coverage becomes substantially more expensive when the guaranteed level period expires. The policy owner is free to keep the policy going and continue to pay the new (much higher) premium. He'll keep his $1 million death benefit coverage if he continues to do this.

Here you can see, this coverage becomes substantially more expensive when the guaranteed level period expires. The policy owner is free to keep the policy going and continue to pay the new (much higher) premium. He'll keep his $1 million death benefit coverage if he continues to do this.

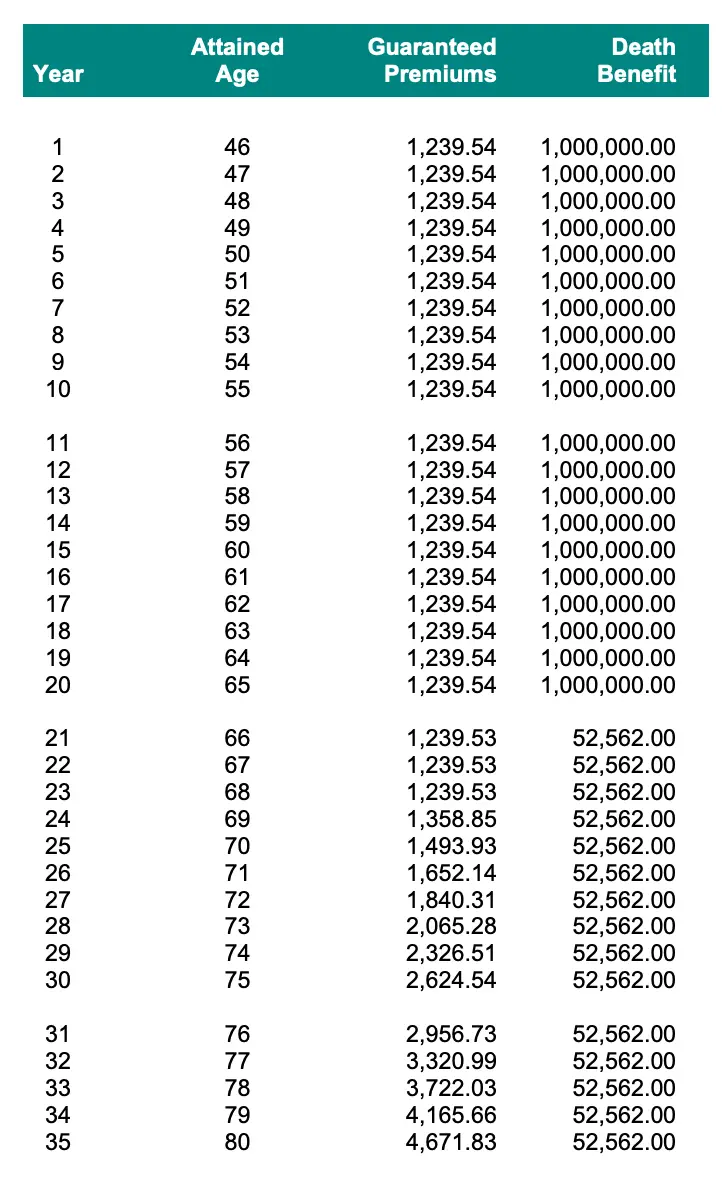

Alternatively, some companies now issue term policies that keep the premium level even after the guaranteed level period, but they adjust the death benefit to an amount that this smaller death benefit would buy at the newly attained age of the insured. Here's an example of how this works:

In this case, the $1 million death benefit cost the insured $1,240 per year. After the 20th year, the premium remains the same, but the death benefit drops to $52,562. The policy owner has the option to keep his coverage at this new lower amount and pay the same premium. But notice that eventually, the premium increases even on this smaller death benefit amount.

Do you get your Money Back when Your Term Policy Matures?

You do not get your money back when your term policy matures. Term life insurance does not offer a nonforfeiture benefit and therefore does not give the policy owner any of his/her money back at maturity.

The premiums paid remain with the life insurance company and the policy owner insured knows that during this time he/she had life insurance coverage that would have protected his/her loves ones' financial interested had he/she died.

There is, in some limited situations, an option to purchase Refund of Premium term life insurance. This specialized form of term life insurance offers to give all the premiums paid back to the policy owner if the insured does not die during the guaranteed level period. This product comes with a higher premium cost than traditional level term insurance.

But if you do not have Return of Premium term insurance, you've reached the end of your level period, and you choose not to keep paying the much higher premium, your death benefit coverage ends and you receive no money back.

Should you Convert to Permanent Life Insurance?

For those with the option to convert a term life policy to a permanent life insurance policy, this may or may not be a good idea for those nearing the end of their level term life insurance period.

Conversions are an option some life insurance companies make available on their term life policies. They allow policy owner to exchange their term insurance to a permanent life insurance policy (e.g. whole life or universal life insurance) without going through the application process for the permanent policy.

If you are looking to keep your death benefit protection, and applying for new coverage isn't an option, then a conversion to a permanent policy is likely your best option.

You should understand, however, that not all conversions are equally great. Some companies limit the permanent product options a term policy owner has when exercising the conversion feature. You should understand the type of policies to which you can convert and if they guarantee the death benefit with the new premium you'll be paying.

Can you Outlive Affordable Life Insurance

When buying term life insurance, you should plan for the eventual reality that you could outlive period of purchasing affordable life insurance. As you age, and the overall probability of your eventual death increases, the price of life insurance increases accordingly. For a healthy young individual, the probability of death is small, and as such the cost of life insurance (term life insurance especially) is very low.

But with each passing the year the probability of dying increases a bit and the cost of a new life insurance policy also increases to account for this. Eventually, you'll likely reach an age where buying a new life insurance policy is prohibitively expensive. If you opt for term life insurance, which is only intended to last temporarily, you'll lose your coverage before the probability of death becomes high.

This is fine so long as you plan for this eventual reality. Planning for this eventual circumstance is a core requirement to the buy term and invest the difference philosophy.

I am going through this as we speak, I’ve been in a 41 Year term life policy that expires on my 65 birthday when it matures without no incentive to convert or continue policy? Bum luck any suggestions

Hi Jeffrey, if you do not have a conversion option then the only other suggestion, if you want to keep a death benefit in place, is to begin applying for life insurance elsewhere.

Does payout of term life always remain same How much can premium increase after maturity Is theee anyway to her cash value from term policy If we discontinue current policy because payment is so high so we have no insurance

Hi Brenda, the insurance company can provide you with the premium increase schedule. There is no cash value for term life insurance.