Podcast: Play in new window | Download

Looking back on our years of selling life insurance, we see a past of lessons learned. Some of these lessons taught us about the methods best avoided regarding life insurance selling. Other lessons solidify some truths we came to understand through years of watching them play out again and again like nighttime re-runs of major sitcoms long since wrapped.

Today I want to share the five things I'm sure most of you heard an insurance agent at one time or another, and I want to validate their validity. Take this blog post as my attempt to be a disinterested third party. If at one point you listened to an insurance agent tell you any of these five things, I vouch for their correctness.

#1 You Don't have Enough Life Insurance

I know what you're thinking. Sure sure, this is just how insurance agents sell more life insurance. I'm fine. I have 2.5x my annual salary as a benefit through my job and that's more than enough for my wife et. al. to run off and find someone else and live happily. Maybe that's not exactly what you are thinking, but I'll bet a majority of you are some close iteration.

The truth is, dying is expensive, and being the survivor of a family with a premature death is even more expensive. I have first hand experience with this one. What seemed like an adequate sum in theory turned into a quickly drained account with little to show for in a scary short amount of time.

There are numerous rules of thumb I could throw at you right now regarding how much life insurance you need, but none of that is helpful. The experts agree on very little when it comes to the specific individual, so I won't waste your time with the same nonsense you can find at any number of novice attempts to write an article about life insurance needs.

Instead, I'll ask you to consider the following…

If you die prematurely, who is going to pay for:

- Your funeral

- The mortgage

- Home maintenance (not just landscaping, but upkeep to the home as things wear out or become damaged by normal weather wear)

- New home furnishings

- Braces (for the kids)

- College

- Cars

- Emotional support for the grieving

- Childcare

- Emotional support for your now single parent spouse

Let's focus in on that car question for just a second. How much will the average cost of an automobile be in 2030? Just so you know, I don't know the answer to this question. But I have a haunch that it will be more than the current average in 2020.

Now, you may tell me that you have a spouse who earns a good living and is completely capable of living independently on his or her own income if you're gone. You might be right. But once your spouse lives alone without you, the risk of his/her losing a job magnifies all the consequences associated with such an event. What if your spouse is suddenly unable to work due to illness or injury? Where does this perfectly independent wage earner turn when his/her independence creator fails?

Further, is your spouse capable of living independently with his/her income and solely supporting the family you built together? Are you being honest when you tell me yes? Or are you trying to sell yourself just as hard as you're trying to sell me? Keep in mind, it makes no difference to me if you are right or wrong. I don't have to live with the consequences of your actions on this one.

As of 2018, the average amount of individual life insurance purchased was $168,000. This is probably adequate for someone who makes around $8,000 per year. I suspect that is no one reading this blog post right now. The vast majority of your are woefully underinsured and the truth is many of you can get life insurance for less than you pay towards any other insurance policy you no doubt have (e.g. car, homeowners, and health insurance).

Insurance agents tell you that you don't have enough life insurance because you don't have enough life insurance. You can put the armor down in your resistance to this conversation. Your agent is most likely correct.

#2 You Really do Need that Disability Insurance

The prize for most under appreciated insurance policy hands down goes to disability insurance. The product holds the most positive consensus among financial professionals as a must have, and yet so very few people actually bother to buy it.

Now, I'll readily admit that acquiring disability insurance is tricky. Underwriting is extremely discerning in most cases. This is due to the massive risk disability policies pose to insurance companies. Disabilities (i.e. events that prevent you from working to earn an income) are astronomically more likely than premature death. And they tend to be significantly more expensive to insure. Without boring you to tears with the precise answer, simply understand that accounting rules that changed in the 90's put substantially higher reserving requirements on insurers when it comes to disability insurance. This ties up way more capital than disability insurance used to, and led to a number of insurers making the decision to terminate new business for their products.

Additionally, disability insurance often appears expensive, but can result in substantial cash payments to the insured. Consider the following example:

[thrive_text_block color=”blue” headline=”Disability Insurance Cost Example”]Ben is looking to buy individual disability insurance and receives a quote from an insurance agent. Ben's monthly benefit for the policy is $5,000. The policy is in effect until Ben reaches age 65, comes with a 3% COLA increase if Ben triggers the benefit, and will also cover him for partial disabilities. The monthly premium for this policy is $227, which is considerably more expensive than the $65 per month Ben is paying for term life insurance. Ben is a bit hesitant to spend so much money on disability insurance. [/thrive_text_block]

Any insurance agent who actively discusses disability insurance with clients or prospects has experience with the above example. A lot of people look at the monthly benefit, compare it to the premium of the disability policy, and pump the brakes noting how expensive it seems. But think about what this disability policy represents in terms of liability to the insurer (or payout to Ben).

Suppose Ben is currently 30 years old. If he buys the policy and permanently goes on claim soon after purchase for the complete monthly payment, Ben will end up receiving a little over $3.6 million in total payments from the policy. Let's assume Ben goes on claim 10 years after he purchases it. He still receives almost $2.2 million in total payments.

Disability insurance can appear pricey because it can easily result in benefits far in excess of the premiums collected.

Lastly, we shouldn't ignore just how critical ones ability to earn an income affects their financial well being. For the vast majority of people, income is the key driver behind their economic achievements throughout their life. Protecting the ability to earn an income when faced with a serious illness or injury makes a lot of good sense.

#3 Long Term Care Insurance is Also a Good Idea

Piggy backing a bit on the disability insurance discussion, long term care insurance is another under appreciated insurance product that many agents mentioned, but often face rather quick dismissal. Here too, price plays a major role in the objection. Long term care insurance can appear expensive, and again, we have to consider what the product promises to protect.

Needing long term care is an expensive endeavor. Factor in the likelihood that you will need long term care and the price of long term care insurance begin to make more and more sense.

A lot of people choose to lie to themselves about the solution when looking at the price tag. They default to a “hope I won't need the care” strategy that is really just a decision to ignore the problem until they can't.

The really really really good news concerning long term care insurance that the insurance industry innovated several ways to address this problem under substantially different product approaches than traditional long term care insurance.

For example, many life insurance products now come with a feature that gives the owner of the policy access to a portion of the death benefit to help cover some of the costs associated with long term care. While these benefits are traditionally less comprehensive than a bona-fide long term care insurance policy, this life-insurance-linked approach can go a long way in helping to bridge the gap when it comes to financing long term care needs.

#4 Insuring your Kids is a Good Idea

I hear the collective gasp as you read that headline. Yes Brandon just said buying life insurance on your kids is actually a good idea. But doesn't this conflict with years of statements that seemed to point to the contrary? Let me explain what I regard as my most misunderstood position on life insurance.

Most people vaguely understand that insurance cost rises with age. They take that understanding and apply it universally across all insurance products and all possible ages to incorrectly assume that buying permanent life insurance on children is the best way to maximize the cash value growth inside a life insurance policy. Let's look at an example to compare policy values:

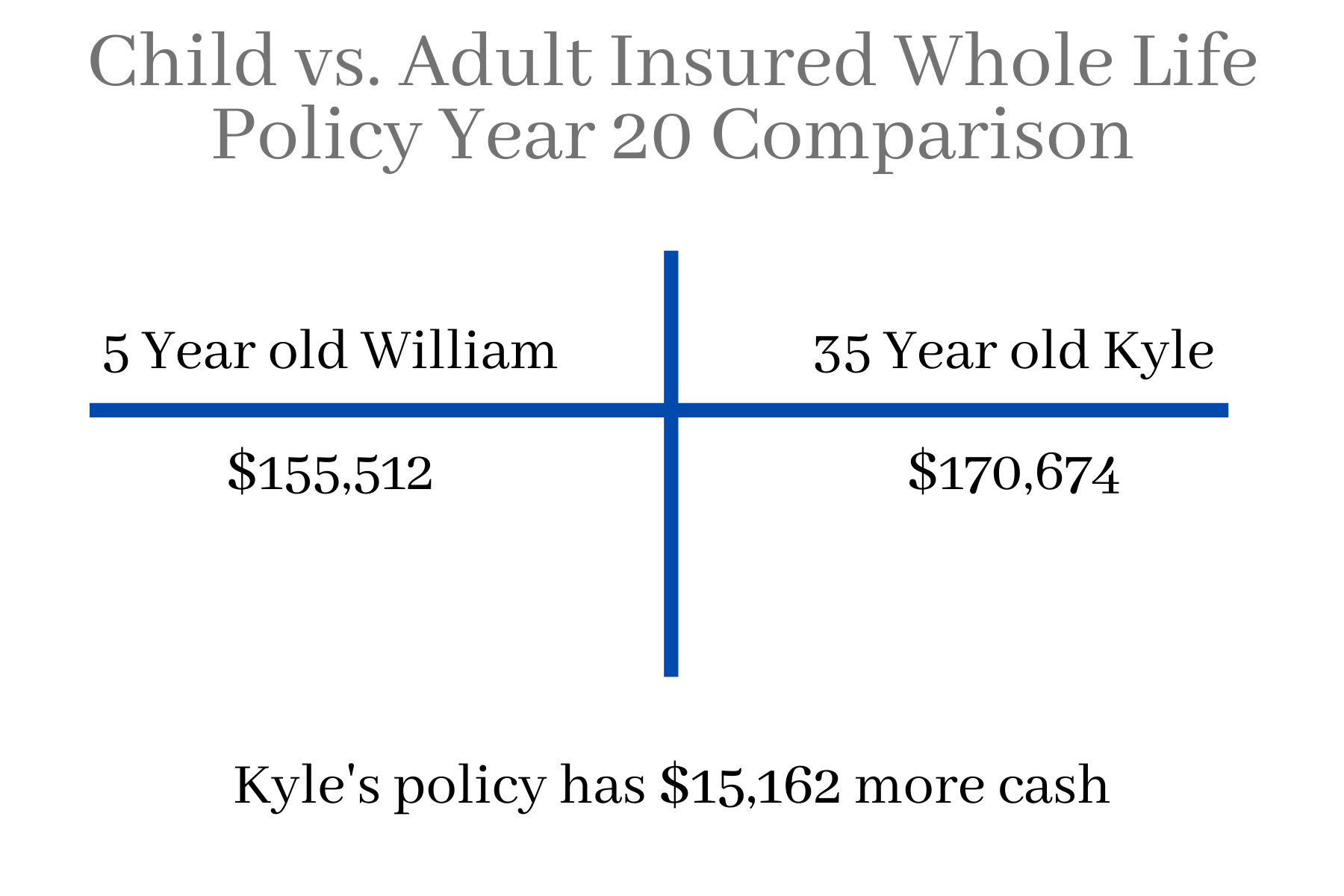

[thrive_text_block color=”blue” headline=”Child vs. Adult Insured Whole Life Policy”]Kyle is looking to buy a whole life policy with a $5,000 premium. He thinks he understand life insurance costs structures and thinks it will be a better deal if he insures his son William instead of himself. Kyle is 35; William is 5. [/thrive_text_block]

Here's how the policy values of these two possible policies compare at year 20:

How is this possible? William is 30 years younger than Kyle. William's cost of insurance should be considerably lower than Kyle's. How could Kyle's whole life policy designed to maximize cash value outperform William's equally designed to maximize cash value policy? It appears insurance isn't quite a straightforward as some of you hoped.

Juvenile policy pose considerable risk to life insurers. They have little medical background off which they can base an underwriting decision and there will likely be years of additional risk the insurer must assume when placing life insurance on such a young life. Insurer know this. Insurers have known this for decades. So they have polices that intentionally build in costs to offset this risk.

My argument was never that life insurance on children was always bad. My argument was simply that life insurance on children instead of parents when the goal was cash value optimization was usually bad. I'll hedge a bit, because we are well known for doing that, and note that extenuating circumstances can and do exist that would green-light a juvenile insured policy seeking cash value optimization. But when both options are open, opt for the parent whenever possible.

Now that we took that little detour to clarify a point, let's get back to insurer children for the simply sake of life insurance…

Juvenile deaths are uncommon. There's no argument from me on that front. However, when they do occur, they are life altering events that leave parents bereaved possible forever. Life insurance on children is not about financial dependency on them–that's an incredibly rare circumstance. It's about having the emergency funds necessary to appropriate process and deal with a life altering tragic event. And…it's an incredibly inexpensive thing to do.

In addition, we don't know what will ultimately happen to the health of children. They will hopefully grow up to be normally healthy adults. But not all of them. Some will face health challenges that will forever alter their lives and their ability to buy life insurance when they reach adulthood. While a small juvenile policy will likely fall well short of the life insurance needs of a health compromised child in adulthood, it will at least give them and their future family some protection they cannot otherwise acquire.

#5 Your Plans Probably Won't Go as Planned

Insurance has always been a focus on planning for the things you don't want to happen. Burying your head in the sand and pretending that you have some super special way of avoiding it isn't a plan, it's childish behavior seeking to avoid addressing the real issue.

If you told 24 year old me where 34 year old me would be, I wouldn't have believed you. I'm sure a lot of people can relate. Some times where we land is considerably better than we imagined. Others wind up in a different direction. This message specifically seeks to catch the attention of the younger crowd.

We all observe those older than us and pick out their mistakes. We tell ourselves that we'll be better off because we can learn from their mistakes and simply not make them. If only life was truly that easy.

Talking about insurance requires we focus on the plan not going as planned. People have a tendency to want to reject this notion. Sure things are perfect right now, but they will be, just you wait and see. I've watched incredibly successful friends and clients face financial ruin. I've watched down-on-their-luck friends and clients achieve incredibly improved success. To steal a tired cliché: the only constant in life is change. I'm not even all that old at this point.

Life insurance agents focus on a lot of the negative things that can happen in your life. None of us want them to. We hope results will play out better. I know of no insurance agent who takes pride in being right about unfortunate circumstances unfolding–insured or not.

We cannot ignore these potential hazards. We have to acknowledge them and seek out a plan to mitigate their impact whenever possible. There's a chance you will die much younger than you planned. There's a greater chance that you will get sick or injured and be unable to work for a while. There's a really good chance that as you get older, you will become more dependent on the help of others, and may one day require skilled care for your daily living.

If you have children, they will most likely grow up and reach adulthood, but there is a small chance they won't make it. There is also a great chance that other things in your life will go in a direction other than what you planned. More years ahead of you means more chances for things to go great and equally go terribly. You can't dwell on the possibility of negative events–that's unproductive. You can, however, do your best to prepare yourself for them if they do unfold.

Bonus #6 That Financial Guru isn't Talking to you Specifically

Financial gurus dispense lots of quick digestible tidbits of information. It's often non-specific or precisely focused on a unique circumstance. Despite this, a lot of us choose to apply this non-personal information to our own lives through various adaptations of interpretation of the advice.

This seems logical. The advice appears solid enough to alter a bit in order to make it fit my life, priorities, and goals. But is that really a good substitution for more tailored advice? Probably not.

Bloggers and radio personalities that focus on personal finance can be entertaining, but that's generally the end of their usefulness. They can help start the thought process of what you need to do, but these people are rarely subject matter experts. They are entertainers with a hobby-level interest in personal finance. They do not possess the hands-on experience or formal training in the field of actually guiding people to an appropriate plan of action relating to their financial lives.

The things they say or write about do not specifically apply to you, and you shouldn't take this information as definitive advice for your specific circumstances. They all use disclaimers that make this very statement.

It's perfectly okay to consume the content created by these gurus. It can be very helpful in pointing you in a certain direction to investigate in more detail. You just need to be careful about putting too much fait in what they have to say and incorrectly assuming that you can develop universal thoughts about financial planning or one of its many facets based solely on a 5 minute segment or a blog post that covers only a tiny portion of a much broader subject.