Podcast: Play in new window | Download

The best whole life insurance policy for infinite banking® is one that uses the most optimal design for the accumulation of cash value. Today I'm going to walk through this as well as guide you on some other important factors concerning any plans you might have to purchase a whole life insurance policy to implement any of the self banking strategies.

The majority of today's list focuses on attributes or fact patterns that must exist to ensure the best potential outcome from using Infinite Banking®, Bank on Yourself®, etc. This includes not only what the whole life policies needs, but what needs to exist in your personal circumstances.

Paid-Up Additions

The whole life insurance policy that you buy absolutely must make maximum use of the paid-up additions feature of your whole life policy. This means you should both use the dividend option to purchase paid-up additions and the paid-up additions rider.

The dividend option part is easy. You simply ensure that the dividend option selected is to purchase paid-up additions. The rider part is much more nuanced. When you look at the premium you intend to pay each year, you want the paid-up additions rider to comprise a larger percentage of this overall premium.

For example, if you intend to buy a policy with a $10,000 annual premium, at least 50% ($5,000) of that premium should be the paid-up additions rider. More ideally the paid-up additions rider amount would be $6-7,000 per year. There aren't any quick reference sources you can turn to determine what the maximum allowable paid-up additions rider amount is for any specific product at any specific company, so you can use this rule of thumb as a good guide. Alternatively, you could always seek out a consultant to review the policy in question and help guide you on its PUA adequacy.

Also, you should know that there are some companies issuing products that some of the sales force will claim don't need paid-up additions because the product uses some sort of internal cash maximization feature. You should avoid these products. They either produce large immediate cash value at the loss of long term performance, or they offer a sort of meh overall rate of return on cash value when compared to the type of policy I'm helping you piece together in this article. That's not to say these types of policies are never a good idea. They simply aren't indicated for this specific context.

Term Rider Blend

I know this appears strange. Here I am recommending the best design to optimize cash value in a whole life policy, which intuitively infers the minimization of the death benefit. However, I'm recommending that you add a term life insurance rider to the whole life policy? What gives?

The term rider is not here to give you additional death benefit. Its purpose is the drive down the base whole life death benefit (because paying for it is expensive), which will give you greater capacity to use the paid-up additions rider and remain Modified Endowment Contract compliant. We call adding a term rider to a whole life policy “blending” because you are blending whole life with term life insurance.

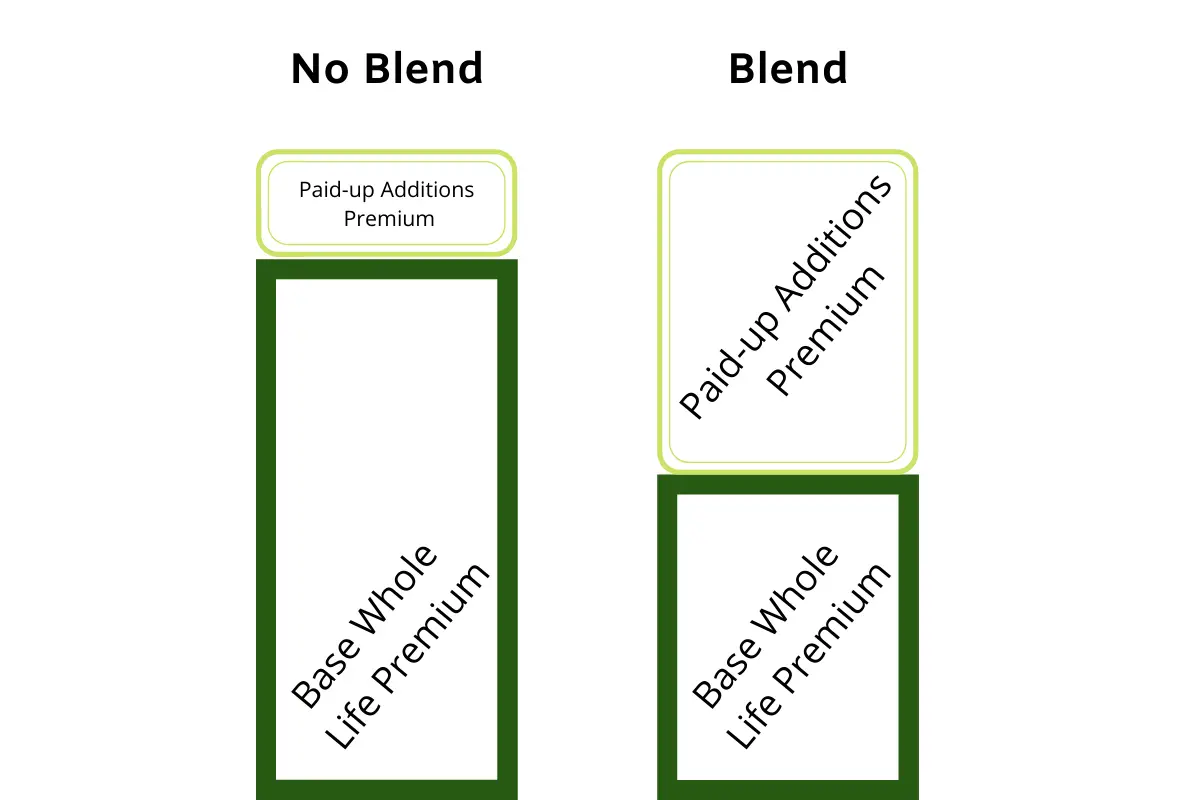

Here's a graphical depiction of what we accomplish with a blended whole life policy:

Without the term rider blend, we have little capacity to add paid-up additions to the whole life policy before we reach the MEC limit. With the blend, we keep the same death benefit we had before, but now we have a much smaller whole life premium. This allows us to fill that space back in with paid-up additions, which will create more cash value and a better return on our premium dollars.

Term riders do come in different forms so it's difficult to say universally how this will work on a whole life policy. But here's what you do need to know: you do not want a level term rider with a specific expiration date.

Most term riders have an indefinite expiration date (up to some advanced age like 95). The problem with shorter terminal term life riders is they can create MEC violations unwittingly. How exactly this happens will force us to take a huge detour, but the really short (and probably not super helpful in terms if mastery level understanding) answer is, the reduction can very likely take place within a seven-year time span from the last material change in the policy.

This action creates a MEC violation if the new death benefit (post-reduction) has a corresponding 7 Pay Premium with an amount lower than any payment made since the last material change. So the really easy way to solve this problem is to avoid policies with term riders that have specific terminal dates like a 20-year term rider.

Your Personal Health

You have to be healthy to be a candidate for cash value life insurance when the focus is on maximizing the return on the cash value. This is especially true for any self banking strategy.

Now, when I say healthy, I don't mean marathon runner or a lipid profile cardiologists would fawn over. I simply mean you have to come in at a standard or better rating from the life insurance company. Below that, and you'll wrestle with a lot of added expense that simply won't make sense.

Now, some of the self banking gurus suggest that if your health or personal circumstances make a life insurance policy on yourself a no-go, just insure someone else and you can own the policy. Why would you do that? Because if you own the policy, you control the cash value.

The problem is that it's easier said than done. Yes, you have some liberty to insure a spouse and (to a much MUCH lesser degree your children), but outside of these options, there's usually nowhere else to go.

Not surprisingly, life insurance companies aren't all that crazy about the idea of insuring someone else's life just so you can have the cash value in the policy. As such, a lot of rules now exist in the underwriting guidelines to prevent this sort of “workaround”.

Highly Rated Insurers

Choosing to invest your hard-earned dollars in a life insurance policy with an eye on accumulating cash values for your own personal use requires a strong vote of confidence in a life insurer as well as an extremely long term commitment. You need an insurer that not only masters the requirements set forth to be engaged in the business of life insurance, but also one that excels at generating cash while doing it.

Ratings are a tricky metric because they mostly depend on the capital adequacy of a life insurer (i.e. its ability to liquidate and pay its obligations to policyholders). Most ratings place little weight on an insurer's cash flow. Additionally, ratings issued by major agencies are not uniform among each other so an A+ rating at one agency means something very different at another.

This can be a tough sea of information to navigate for the layperson, but there is one metric that can serve as a quick and dirty way to evaluate insurers and compare their overall financial strength against each other.

The analytics company Ebix has its Comdex score, which it assigns to all life insurers. The Comdex is a percentile ranking Ebix uses to rank insurers from 100 (strongest) and down. While alone it's not the most comprehensive way to evaluate life insurers, it is a good way to get a quick feel of how one might compare to another.

Dividend Recognition?

Many self banking practitioners make a big deal out of whole life dividend recognition. They exclaim that non-direct recognition is the only way to successfully implement such a strategy. While this may be true in the most theoretical context of the discussion, once we introduce the practical element of how life insurers actually pay dividends to policyholders with either dividend recognition method, we discover that it usually makes little difference.

Policies that use direct recognition are not fatally handicapped the majority of the time (despite what you might hear). If you'd like an extremely deep dive analysis into this very subject, there is a webinar/case study we did that's part of the Predictable Profits course.

The important thing to understand here is that dividend recognition is a bit nuanced and the variations from company to company matters enough to require a look beyond dividend recognition and to understand other facets of the policy that might matter more when it comes to policy loans.

These are features like the loan interest rate, the timing of loan interest accumulation, the actual dividend adjustment in the case of direct recognition, and how dividend recognition (either type) might impact the company's willingness and ability to pay dividends overall.

That being said, I'll give you one quick rule of thumb to help add some insight on any prospective whole life purchase. If your agent is telling you that you must buy a specific whole life policy and not another because of dividend recognition without any detailed elaboration on why… run away.

Remember, the most important metric to evaluate when you are trying to choose the best whole life policy for infinite banking, pay close attention to the internal rate of return (IRR) on your cash. It's the most telling detail of the overall value that your policy is delivering to you.

Editor's Note: Infinite Banking and Bank on Yourself are registered trademarks. The Insurance Pro Blog does not own these trademarks, nor do we have any business relationship with either entity. This article does not seek to endorse either entity nor does it intend to imply either entity's endorsement of the Insurance Pro Blog.

The age at which a person is to old for this concept to work effectively.

Hi Philip,

Somewhat tricky answer since the time one plans to let pass might make this a reasonable strategy for people in more advanced age. That said, the likelihood that they will actually use IBC-like features after reaching age 70 (not to mention the potential underwriting problems) becomes low.

Hi Brandon. Thanks for another helpful article. I have 3 policies, the first of which started over 14 years ago. So I have a passing familiarity with many of the terms you’re using here.

Of course, my agent claimed that my policies have all the features you mention. To what extent, I’m unsure and I’ll probably never know, since my final payments happen next year and it’s too late to change or improve them. I have my doubts that they’re the best they could have been, but maybe they’ll end up to be good enough.

One surprise in your article: when you mentioned how difficult it is to insure another person. My policies insure me, except for one, which insures my brother while I’m the owner.

Maybe I got away with this because it was roughly 13 years ago. But do you anticipate the company having any problem with this particular policy (since you say there are rules against this now) as I enter the stage in life where I need to start using the money I’ve accumulated?

Also, I’ll have to see if I can figure out the IRR on my policies. I’ll probably be in for a rude awakening, but like I said, they are what they are and too late to improve now. Thanks again!

Hi Ken,

“Insurable interest” is the insurance concept at play when it comes to insuring someone that is not you as the policy owner. Life insurance companies can only reject a policy on insurable interest grounds at application time. In other words, if the insurance company had no problem with the insurable interest when you applied and it issued the policy, the ship has sailed for them to take issue with it afterwards.

Additionally, insurable interest does not affect your ability to use cash value in the policy.

Thanks for the reply. Very reassuring. I never gave insuring my brother a second thought until I read your article. Good to know I’ll be able to use the cash value. Thanks!

This is a remarkably an unremarkable episode.

A.) Use a large quality dividend paying policy.

B.) Use 2 to 1 PUA to Base Ratio. (This is a bold and fantastic claim.)

C.) Whole Life will not change your life. And peril does not exist where sales people say it does.

D.) Chill on Direct v Non Direct recognition.

E.) After 400+ Podcast episodes… there are still audio issues they can’t figure out how to edit out… awesome.

F.) If you don’t have a good amount of money to save annually, which will not stretch your budget, buy some term… this is refreshing.

So I take it, you didn’t like the episode?

What do you think we should have said?

This was a great episode. I just can’t believe it has taken over a decade of reading and listening to industry experts to get the bottom line like you gave.

These points you made, and I summarized, would save a lot of buyers a lot of time. And advisors even more time running thousands of illustrations to find out the best policy design.

Does that make sense?

Brandon and Brantley.. please keep up the good work, I am recently licensed and have been digging deep into the policy software

Thanks for the feedback Adam.

Great content… I have reached out to several agents and most of them are not knowledgeable on how to structure these policies for maximum cash benefit… how do I get in contact with agents that are well versed in IBC or privatized banking?

Hi Ron, you can always reach out to us. Click here for the contact form.