Podcast: Play in new window | Download

Single premium life insurance functions just like it sounds. You pay one single premium and the policy remains in force forever. In somewhat more technical insurance-speak, it only takes one premium to satisfy the paid-up requirement of the policy.

This sounds pretty cool at first glance. You pay one premium and you can keep your death benefit forever and always with no need to make any additional premiums. I can hear many of you shouting “sign me up!” But if you go out hunting for this type of life insurance, you'll find it's a bit trickier to find than almost any other type of life insurance. Why this is the case and what you can do given that fact is the focus of today's blog post.

Life Insurance Before the TEFRA/DEFRA/TAMRA Decade

Prior to the 1980s life insurance enjoyed even more incredible tax features than it does today. If one bought single premium life insurance during this time, he/she enjoyed all of the tax favorable treatments we associate with life insurance today. But this fact left the door wide open for a tax sheltering loophole that Congress sought to close through several legislative acts in the 1980s. The long and the short of it is that single premium life insurance lost several tax favorable benefits.

However, after the dust settled, single premium policies did keep one extremely important tax efficiency. The death benefit remained income tax-free to the beneficiary. This preserved a strategy some people use to augment cash set aside for heirs while using life insurance to make the transfer extremely quick and efficient.

[thrive_text_block color=”blue” headline=”Single Premium Life Insurance Legacy Example”]Rose set aside $100,000 she intends to leave to her four grandchildren when she dies. At the moment the money sits safe and sound in a CD at the local bank.

Rose learns that she could take the $100,000 and purchase a single premium life insurance policy and this will give her a death benefit of $160,000 and require no future premiums to keep at least this initial death benefit. The policy is a dividend-paying whole life insurance policy, so there's a strong likelihood that she will earn dividends that could increase her death benefit if she chooses the option to purchase paid-up additions.

Rose has no plans to use the money, but she'll still have about $80,000 in cash value when she buys the policy that will also grow over time. She especially likes the idea of leaving at least $40,000 to each grandchild instead of $25,000.

She also likes that the life insurance policy will pay the cash to the grandkids almost immediately upon her passing and she no longer needs her Will to stipulate the payment to the grandkids.[/thrive_text_block]

The power to leverage the money you intend to leave to someone gives single premium life insurance a strong reason to consider it, but losing the ability to shield sums of money from taxes if you chose to take money back out of the policy definitely set this product back in terms of attractiveness. Unfortunately, because of the sweeping changed brought about in the 1980s, all bonafide single premium life insurance policies (excluding some 1035 exchange situations) are Modified Endowment Contracts.

Lower Interest Rates Affect Availability of Single Premium Life Insurance

You are probably well aware that interest rates are lower now than they were a little over 10 years ago. Following that the 2008 Financial Crisis, the Federal Reserve pumped so much money into the U.S. Economy that we've seen nearly zero percent interest on some fixed assets.

Some questioned if we'd enter negative interest territory like some other foreign nationals. Though interest rates did rise over the course of the past couple of years, they still remain significantly lower than the levels they reached during the '00s.

This low-interest rate environment places a squeeze on insurance company profits as some struggle to produce returns much beyond the guarantees offered in life insurance contracts. This becomes more problematic for certain types of life insurance and single premium life insurance is one such product.

Lower interest rates make it more difficult for life insurers to achieve the returns necessary to make the promises offered by single premium life insurance. Given the problems insurers face in finding returns comparable to most of the last decade, many insurers gave up on offering single premium life. The margins are too thin and the risks of failing to meet reserve requirements too great.

But that doesn't mean all is lost for the product or the idea. While low-interest rates certainly place a big impact on whole life insurance contracts that require only one premium, universal life insurance isn't affected in quite the same way. This largely stems from the fact that universal life insurance products can offer lower guarantees than whole life contracts.

So single-premium universal life insurance still exists, we just don't call it such. Most guaranteed universal life insurance contracts still offer a customized premium payment period as short as one year.

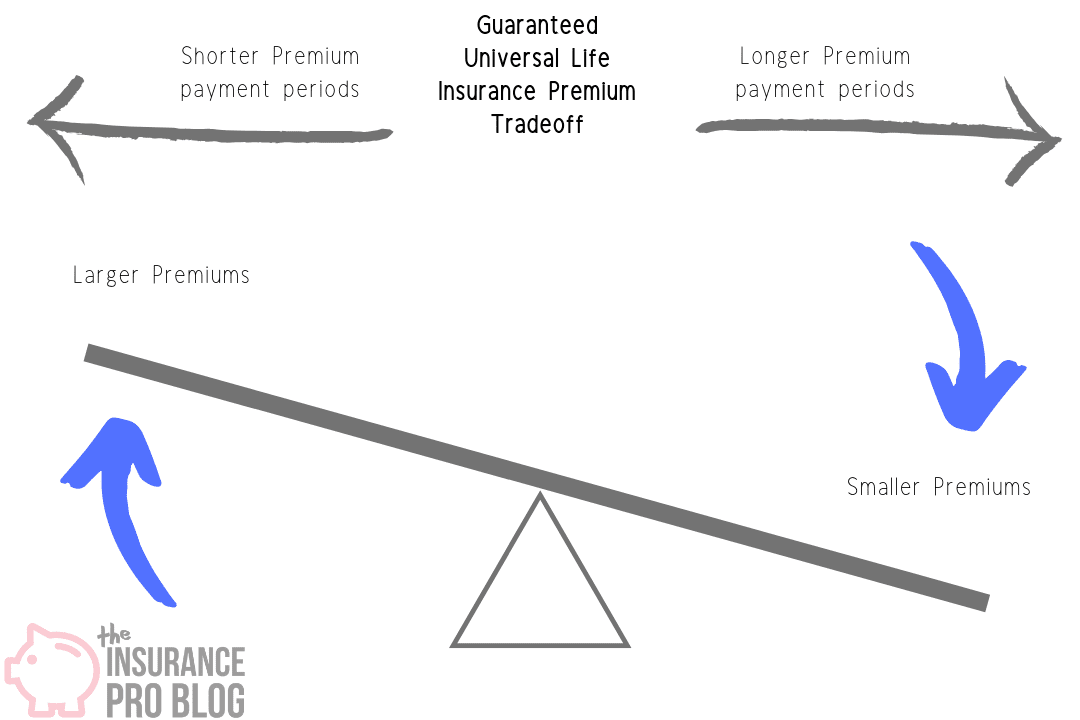

These products cut out most cash value access a policyholder has with a product in exchange for a guaranteed death benefit provided the policyholder meet an obligation expressed in premiums paid to the policy. Many contracts allow the policyholder to customize the number of premiums paid under the following seesaw-like stipulation: shorter premium payment periods require larger premiums while longe premium payment periods require smaller premiums.

You can infer correctly from this information that a single premium for one of these guaranteed universal life insurance contracts will require the largest premium possible in order to guarantee the death benefit remain in force. There are a couple of more advanced issues that come up when we try to design a single-premium guaranteed universal life insurance policy.

Namely compliance with the 7702 test given the large single premium. We often find that we need the Cash Value Accumulation Test to qualify the contract as life insurance instead of the usually more common Guideline Premium Test when designing universal life insurance. If all this terminology is new to you, you can find introductory information on it here.

While it is possible to effectively make a single premium universal life insurance policy that is not on one of these guaranteed chassis I've mentioned, I wouldn't recommend it. There's a lot that could go wrong when using such a product.

Effectively Single Premium Whole Life Insurance

While most life insurers that issue dividend-paying whole life insurance suspended their single premium whole life products several years ago, you can still find the product from smaller lesser-known life insurers. Or you can potentially create a policy that is not a bonafide single premium policy, but it'll function like one.

This is done through the incredible versatile design options whole life permits. Any skilled agent can help design such a policy for you. You should know that in most cases, this will be a modified endowment contract, though there are potentially ways to avoid this.

What about My Old Single Premium Policy?

If you're reading this knowing that many decades ago you bought a single premium life insurance policy and you're worried about its current tax status you should understand the following. Policies issued prior to the legislation that changed the tax status of single premium life insurance received grandfathered status for tax purposes. This means that the rules placed in the 1980s largely do not apply to your policy and you (lucky soul) have a single premium life insurance policy that enjoys bountiful tax benefits in a way unachievable today.

If you happen to be an agent looking at one of these very old policies and contriving a way to replace it in order to sell a new policy, you should probably stop where you are and look for new opportunities to sell life insurance. These policies enjoy a very special grandfathering that you'd be wise to leave alone.