Podcast: Play in new window | Download

For most agents, return of premium life insurance likely conjures up thoughts about term life insurance. This comes from the marketing hurrah over return of premium term life insurance now over a decade ago.

The success of that product wasn't smashing. However, that does not mean insurance consumers show zero interest in the ability to recoup their costs in buying life insurance.

Return of Premium Term Life the BIG Problem

Return of premium life term life insurance seemed like a killer idea. Term's biggest drawback is the fact that you can–and most likely will–outlive your term. If you do outlive the term, you paid all those premiums for seemingly nothing. Say nothing about the peace of mind the financial security blanket the death benefit afforded while you were paying those “meaningless” premiums.

So if you tell me I can get back all those “wasted” premiums, it seems we'd have a slam dunk. Why then didn't this idea explode with success? Cost.

Return of premium term life insurance was–and still is–expensive when compared to standard term life insurance. How expensive? I have numbers.

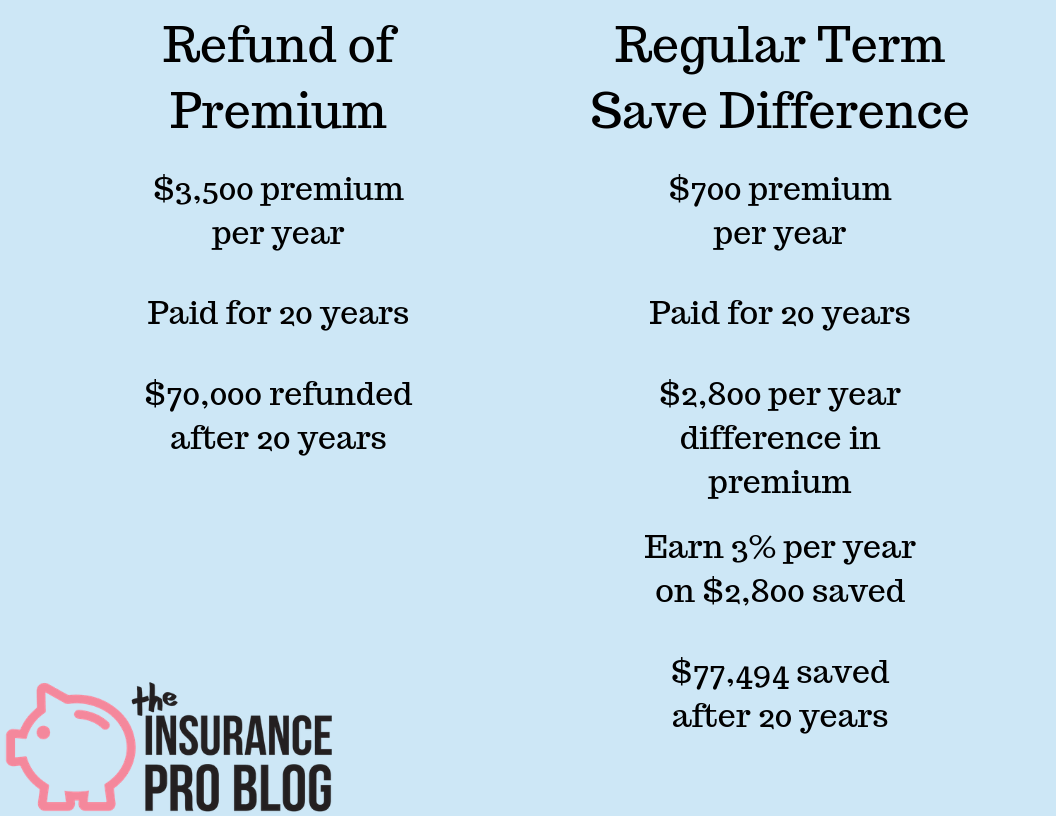

[thrive_text_block color=”blue” headline=”The Cost of Return of Premium Term”]Kyle is a 40-year-old male in good health seeking a $1 million death benefit. He looks at a 20-year level term policy that refunds his premiums if he lives for the next 20 years.

The annual cost of this policy is $3,500. [/thrive_text_block]

$3,500 is a lot of money for a term policy issued to a 40-year-old with a $1 million death benefit and a 20 year level premium period. What makes me say that? A standard term life policy with the same death benefit and the same 20 year level premium period but no return of premium provision costs $700 per year.

Now the lack of success for return of premium term comes into focus. You pay $2,800 more per year for 20 years to simply get your money back.

If instead bought the regular term policy and saved the $2,800 per year. Earning just a little over 2% per year on the $2,800 annual savings nets the same result as the return of premium life insurance policy. If you earn just 3%, you walk away with nearly $7,500 more.

Now I know this seems like I've warmed up a lot to the “buy term and invest the difference” idea. I'll remind you that BTID is an argument against a life insurance product that pays a lot of interest on the money you give the life insurer.

But the problem that we note about buy term and invest the difference persists in this situation. Most people aren't going to save that $2,800 they save when buying the regular term policy. There are people who would never save more money than the refunded term insurance policy will give them.

I'm not trying to pass judgment on them. A number of circumstances exist that make this their reality. In that case, return of premium term life insurance might be a good option.

Whole Life Insurance The Original Return of Premium Product

One of the original attributes of whole life insurance concerned complaints about term insurance premiums. People paid premiums for a life insurance policy that might result in no death benefit payment. Whole life insurance set out to give that premium back.

But insurance laws that evolved after whole life's inception required life insurers to share in the profits of collecting those much higher premiums. As a result, insurers pay interest on cash values in whole life policies.