As of late, it would seem that a great many people are engaged in a bit of retirement savings roulette and I’m afraid it’s not going to end well for them.

Just in case you’ve been living under a rock for the past four years or so, interest rates paid on traditional income generating retirement vehicles—i.e. CD’s, Bonds, Fixed Annuities, and Money Market Accounts is abysmal.

This of course has put a great deal of pressure on the retirement savings that most Americans have accumulated during their working years.

If you’re now at that point in life where you’re not generating income anymore, you most likely have a pot of money that you are counting on to spit out income on a regular basis.

Now, I’m not going to dive deep into all the ways you could do that, we’ve written extensively about that in previous posts. I’ll list some of those here just in case you’d like to learn more. I’ll also give you a hint about our philosophy…it’s not what you’ll typically find on other personal finance sites.

- Create Your Own Pension

- Retirement Income Opportunity

- How Much Money Do I Need to Retire?

- Use Cash Value Life Insurance to Create Retirement Income

I really want to address something that I read in an article yesterday on the CNBC site. The title of the article: Is it Safe to Chase High Yield in Retirement?

The article points out that our appetite as a nation has become quite ravenous when it comes to investing in fixed income—particularly investing in bonds. And even more specifically in high yield bonds.

Right about now you should be saying “uh oh”.

I have a feeling this is going to be a good deal for someone, but it’s not going to be for the investors. Big shock to you all I’m sure!

What’s more disturbing?

Evidently there are retirees who believe they have no other choice. The story actually quotes a retired school teacher who manages his own investments and says,

“You’ve got to put yourself at risk if you don’t want everything to be eaten up by inflation. I’m conservative, but I’m not going into a bunker here. Our portfolio needs to be growing”

Wow.

Now we all accept a certain degree of risk everyday with any of our investments but my contention is that when you are beyond your income generating years, you don’t belly up to the roulette table with your retirement savings. Just a really bad idea.

I don’t think that most people fully comprehend the high degree risk that’s involved with chasing yield in the bond market. Everyone tends to think of bonds as those things their grandmother bought down at the bank and gave to you on your birthday.

But not all bonds are created equal. And furthermore most of the investment in the high yield bond market is coming from mutual funds and ETF’s.

So why’s that so bad?

Well, I’d be willing to bet that most of the people who’ve invested in those funds have no idea what the fund managers are actually buying. Sound a little like 2008 all over again?

There’s no magic to getting higher yield in our current market. The only way to do it is to buy bonds that have a higher coupon and that means a higher risk as well.

What’s the risk?

That depends. I know that’s one of my favorite answers but I’ll tell you what I mean.

Of course every bond has default risk. That’s pretty straight forward. Typically a company who is forced to pay a higher interest rate on its bonds is doing so because their financials don’t look so hot and the market demands that they pay a higher rate. I think we all get that—people or businesses with poor or questionable credit history are asked to pay a higher rate.

But one of the major trends in fixed income investing over the last few years has been the purchase of bonds from emerging markets. Think India, Brazil, Venezuela, China etc.

On a relative basis to the balance sheet of developed nations, including the U.S., bonds issued in emerging markets look pretty attractive.

The CNBC story reports,

“Emerging market governments have become very responsible. In sub-Saharan Africa, for instance, the government debt is now 35 percent of GDP. For the G7, it's 120 percent of GDP,” notes Charles Robertson, global chief economist for Renaissance Capital Research

Those numbers look pretty good. I’ll tip my hat to those countries who’ve definitely done a better job than we have of managing their fiscal policy.

So am I just a xenophobe?

No not at all but I just think that people need to understand that many of those countries still have a great deal of geo-political risk involved.

What do I mean? Well you have to understand the politics of each country, how they differ etc. For example, the stability of the government and how ripe they are for some warlord to take power or some crazy radical who threatens to kill everyone who comes out to vote. This is risk that's a little harder to measure.

Financial risk is relatively easy to evaluate because math is universal. Political risk is significantly more nuanced.

My last point about risk is that let’s not forget what I said earlier. Most of the money that’s being plowed into bonds from retirement savings, is being done so in bond funds.

These funds are highly susceptible to interest rate risk and it takes a little bit of educating to understand it. But it’s a very simple concept, so hang in there.

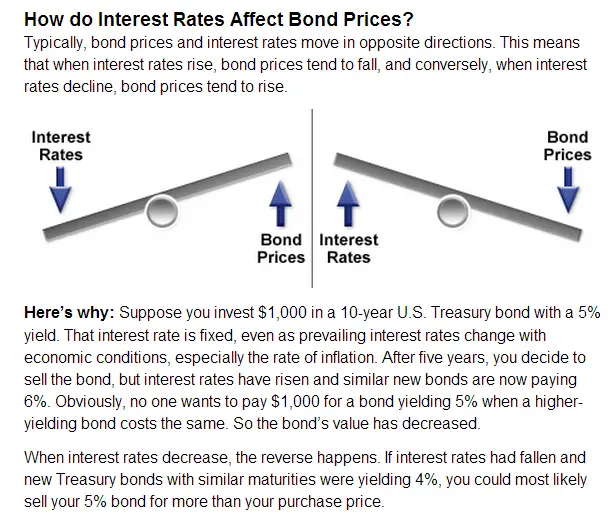

Have you ever heard of the bond see-saw?

The problem with bond funds is that they are continuously receiving new money that they have to invest. As part of their investment policy, the fund can only hold a certain percentage of their assets in cash at any given time (the specific number is in the prospectus of each fund).

This means they have to constantly find new sources of investment for the inflow of money. Right now the demand is overwhelming the supply. So this means fund managers are really scraping the bottom of the barrel to find yield.

The bottom line on Retirement Savings

When interest rates rise, all the bond that are currently held by the will be worth less than they are currently. So, what you’ll see is the dividend yield of your fund will increase but your market value will decline.

You should listen to our podcast episode where we talk about this very thing.

I’ve seen it in action back in the early 2000’s and I also had the pleasure of trying to explain it to clients. I think we could all agree that it’s not something you want to understand after the fact, it’s something you need to grasp right now. If you learn it after the fact, you’ve likely lost a boatload of money, particularly if you’re invested in a high yield fund where all market movements are amplified.

Brandon and I have said this many times in various iterations but it’s worth repeating.

Chasing higher returns is a poor substitute for having saved enough. If you don’t think you can generate the income you need from your retirement savings by using CD's, Treasuries, or Fixed Annuities with guarantees–perhaps you’re not ready to retire?