Podcast: Play in new window | Download

Northwestern Mutual is a huge mutual life insurance company in the United States. The company boasts an impressive policyholder count, an extremely large asset pool, and enviable profitability. These stats alone are a good reason to stand up and take notice of the Quiet Company.

With all signs pointing to a well-capitalized and profitable insurance company, it's easy to assume that the insurance policies might just write themselves. That, apparently, isn't the case.

Despite Northwestern Mutual's success, we find its sales agents sinking to new lows in their efforts to sell whole life insurance policies.

Northwestern Mutual and Blease Research…It Was the Best of Times

Northwestern Mutual and its sales agents never lack confidence when discussing the company's superiority. Our interactions with current and former agents of the company certainly underscore a culture of feeling special.

To most agents, Northwestern is best. There is no one better. No way. Now how.

And they even have third-party research to back it up!

Or they sort of did…

For a couple of decades, Blease Research compiled copious data on the life insurance industry. One such collection of data focused on actual whole life insurance performance over a 10 and/or 20 year period. Blease solicited–and received–data from life insurers about how a real policy unfolded given the actual dividend paid to policyholders.

Because there is no regulatory impetus for life insurers and the disclosure of policy results, the data was self-reported. That should raise some red flags, but it was the best crack at creating such a data set so we tip our hats to Roger Blease just the same.

The Blease data did at one time show Northwestern's whole life policy performing quite well over a 20 year period. Northwestern Mutual agents proceeded to beat anyone within arm's length over the head with this data to prove the company's superiority in the marketplace.

Sadly, Roger Blease the founder of Blease Research died young (48) in 2013. His death resulted in the closing of the company and no one has recreated a company similar to his.

You'd think that would end one of Northwestern's key substantiating arguments for why the company is awesome. With no update to the data, the agents at Northwestern lost the ability to use the report to help sell the company's whole life product.

Any reasonable person would assume that. But we'd all be wrong.

Why You Gotta Bring Up Old Stuff?

A couple years ago we received an email from a new client. He had recently cut ties with a Northwestern Mutual agent…or at least he tried. The agent relentlessly pursued him even after he decided he was moving on.

The email was a short one, but it contained a few attachments. The question from the client was something to the effect of, “is any of this true?”

Several attachments were Northwestern slicks that talked about Northwestern's assets size and lapse ratio. But one attachment, which the Northwestern agent did mention at length in his email, was a copy of an old report I hadn't seen in a while.

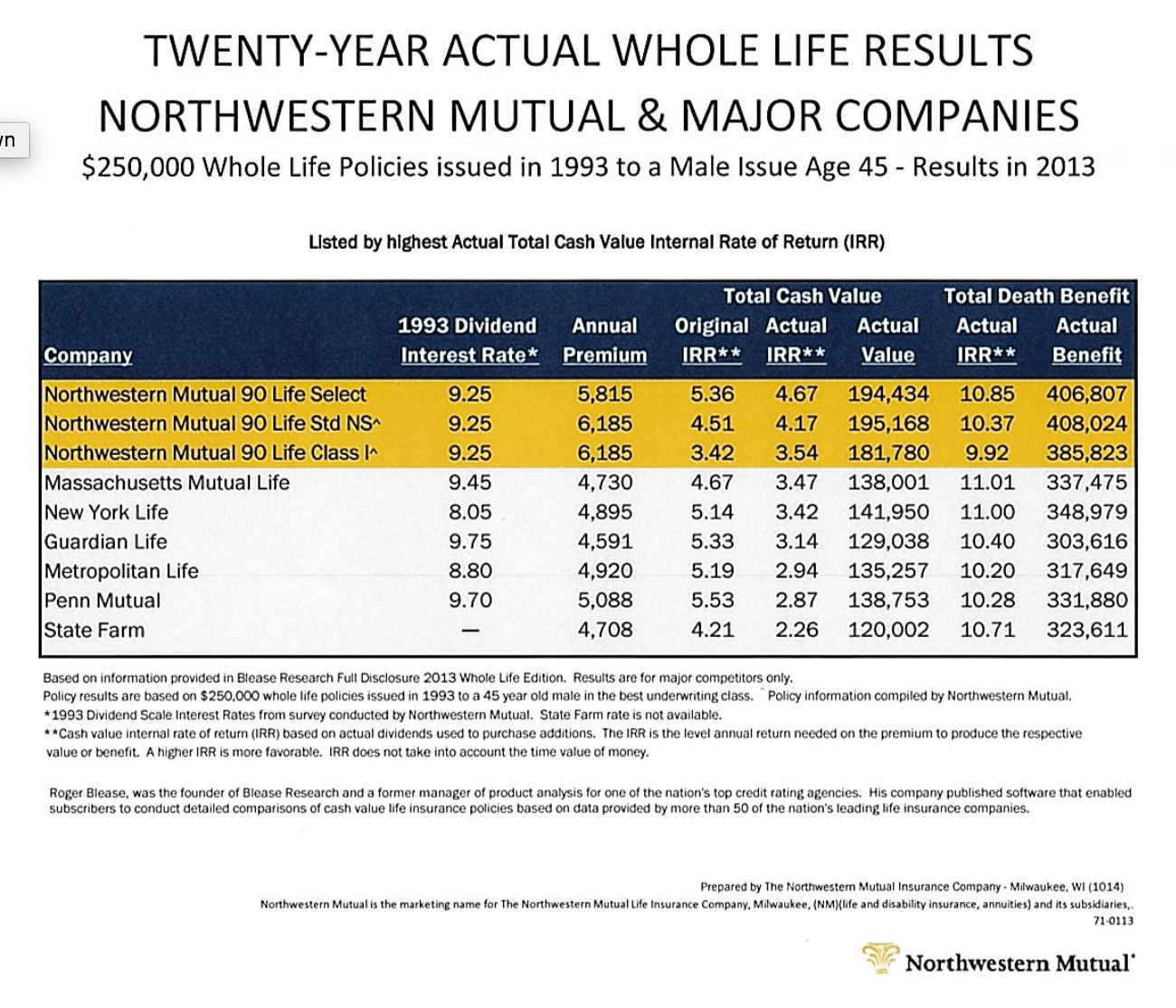

It was the 20-year historical data on whole life policies from Blease Research published in 2013. This was the very last report published before Roger's death and the shuttering of his company.

I laughed a bit when I opened the attachment. It was 2016 at the time so I found amusement in the use of a now-defunct report that was now three years outdated. I wrote a short but to the point reply taking issue with this exact subject and left things at that.

I guess three years outdated on a report that will never again have an update could make some sense. But sadly it popped up several times in 2017. Then again several times in 2018.

And then again a handful of times already this year (twice in the past 10 days). Every time it comes from a Northwestern Mutual agent and it's always the same report. The 2013 20-year historical policy results.

All presented as independent research that proves Northwestern's superiority over the competition.

Northwestern Mutual Apparently Has a Policy

We received word a little while ago that Northwestern Mutual has an internal policy that prohibits the use of this Blease Report because it is now significantly outdated. I'd like to think that this policy exists because Northwestern wants to rout out bad behavior.

But given the continued use of the report, I'm suspect that perhaps the policy exists to insulate Northwestern from liability should someone raise the issue at some point.

In either event, the policy appears ineffective at preventing the misleading use of outdated data to make claims and insinuations about what policyholder can expect from Northwestern Mutual whole life insurance.

In fact, in the years since 2013, the dividend interest rate at Northwestern Mutual has declined from 5.6% to 5%. Other life insurers have realized a reduced dividend interest rate over this same period. But most have experienced far smaller declines during this span.

What About the 10-Year Report?

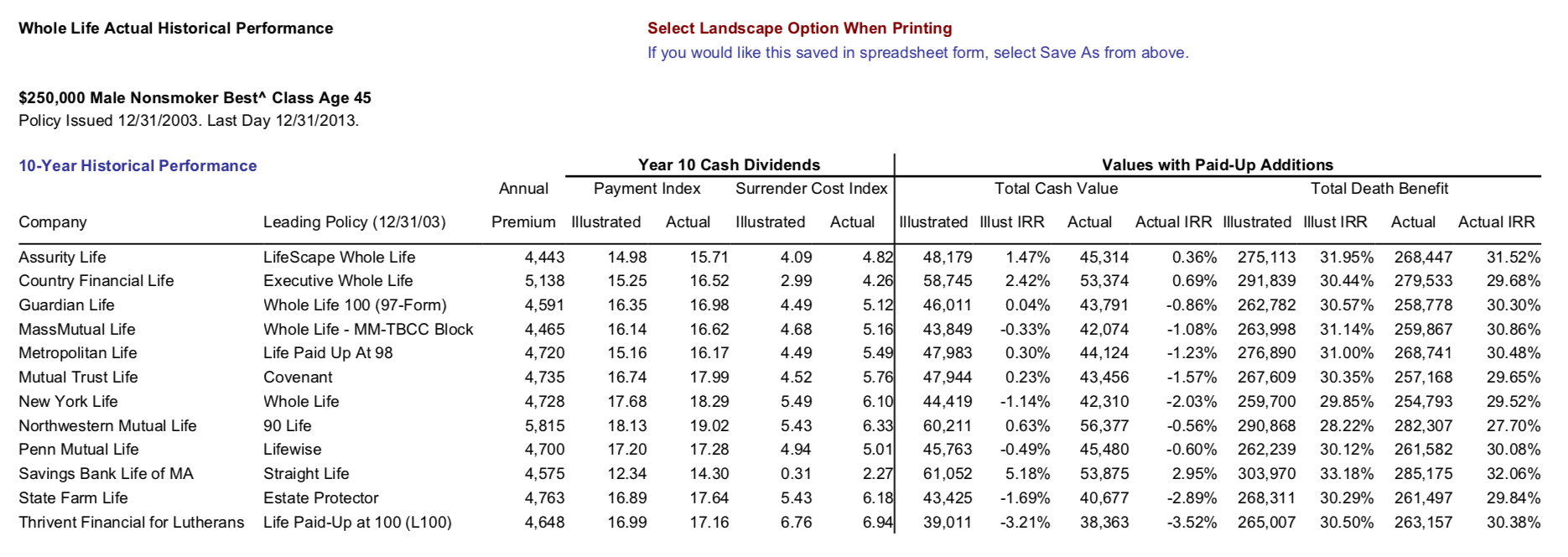

Earlier I mentioned the Blease released a 10 and 20-year report that showed actual cash value performance among whole life products. Northwestern delighted in the opportunity to discuss the 20-year report. The 10-year report…not so much.

Here's the presentation Northwestern created with the Blease data on the 20-year report:

And here is the last 10-year report generated by Blease Research:

Northwestern didn't fare as well in the 10-year report and rarely mentions it.

Look at those Premiums Though

Pay attention to the premium of such a whole life policy in this historical data. Northwestern is by far the most expensive. This matters because the cost of providing life insurance doesn't change much from company to company.

Your probability of death doesn't change if you buy whole life insurance from Northwestern Mutual or New York Life. Despite this, Northwestern charged its policyholder almost $1,000 more per year for the same amount of whole life insurance (see the 20-year table above).

If it didn't cost Northwestern any more money to offer the death benefit, why did it need the extra money? More importantly, what did it do with the extra money?

The most likely answer is Northwestern invested it. That extra capital led to more investment income, which most likely resulted in Northwestern's ability to return more dividends to policyholders. They say that in life there is no magic, just magicians.

Could policyholders at New York Life, Guardian, MassMutual, etc. achieve similar or better results if they gave their insurance company more money than it needed? That's a fundamental building block to blending whole life insurance.

Through paid-up additions, any policyholder can choose to give a life insurance company more money. This results in more cash value and a higher overall return on premiums paid.

Here's the Bottom Line

Northwestern Mutual agents' use of Blease data from 2013 is dishonest and/or foolish. There's a strong possibility it's both. While the company might have a policy prohibiting it, we continue to see this report used by Northwestern agents.

Northwestern is a huge mutual life insurance company. Its achievements regarding market share and brand recognition are noteworthy. But this standing comes with a certain set of responsibilities. If the company continues to engender a culture of dishonesty, the industry will pay for it.

premiums NW $ 5815 MM $ 4465 PM $ 4700. MM’s is 30 % less than NW’s and PM’s is 24 % less than NW’s. Taking that into account, the following is much better comparison. Add to your results reflecting that prem. diff. =

10 year #’s shows cv NW $ 56,377, MM $ 56,377, PM $ 56,400. all about equal. db NW $ 282, 307, MM $ 337,820, PM $ 353,617. conclusion PM is 26 % more than NW. MM is 20 % more than NW.

20 year comparison NW cv 11 % more than PM, NW 8 % more than MM. db NW is 7% less than MM, and 1 % less than PM. For, I don’t care much about 10 or 20 year comparisons. What I do care about are 60 year results starting at age 5 using the same annual premium on each, with PUA, plus a Term rider. The financial product that I feel is simply the best on the planet is whole on kids/grandkids. If you were to run the #’s as I have suggested, you will be amazed at the overall rates of return with respect to cash value and death benefit. Anybody that says whole life insurance is not a good investment is a liar. In fact, given the risk involved, there is no better vehicle out there. While I don’t have access to these 3 companies #’s, you do, I’m guessing the rate of return to be 6 % in cv, and 8.5 % in db. Best feature of all, there are no other decisions to make other than paying the premium. Would love your feedback. thank you

Hi Gary,

I’m interested in why you think that buying a policy on a 5 year old makes whole life insurance so much better. From experience, I don’t think the results will be quite as great as you are suggesting.

Buying whole life insurance on a child, but there are significant limits on the amount of premium one can pay towards such a policy, so what you can achieve with such a strategy is quite limited.

“If the company continues to engender a culture of dishonesty, the industry will pay for it.”

I came in the business June, 1970. NWM was no different than regarding their standing in the industry.

We’ve seen it with the intoduction of interest sensitive whole life, universal whole life, and now with IUL.

It was the late, but great, John Savage who said (and I’m paraphrasing), You’re better off with a great agent from a not so great company than a not so great agent from a great company.

Frank Bettger very wisely put it this way (again I’m paraphrasing), the companies today at the top of the heap may very well find themselves on the bottom twenty years from now.

By not policingvourselves better, we continue to open the door wider for the government to step in deeper and deeper.

BTW, with the passing of Blease, and no new comers, is this something you guys can take on?

Well said/paraphrased 😉

As much as coveted what Roger Blease did, I do not have the Rolodex he had nor the will to try and build the relationships I would need to collect the data he was able to get his hands on.

I am dealing with a Northwestern agent right now (among others) for a policy and he is constantly comparing them to everyone else and how they are head and shoulders better. The one thing he hits hard on is their “lower mortality cost because our underwriting is much stricter” which seems great on the surface but then how would they have such good growth lately if they were so strict? Also, I wonder if their costs are lower because a good deal of this new growth is younger clients who are healthier and if the sample period was stretched to 50 years or so (I don’t what time period he was using because he uses a bunch of different ones), they wouldn’t look much different. I appreciate your thoughts and I love your blog!

By cost I’m guessing he means to Northwestern, which put another way is Northwestern has fewer claims. That’s fine, but by how much and what is the quantifiable difference or meaningfulness of this difference? Has it resulted in a larger dividend payment for comparable policyholders at other insurance companies? Our data suggests the answer is no. If the NML agent can produce numbers that refute this, I sure would be interested in them.

The lower mortality experience/cost claim reminds me of the flashy health tips that report something like eating some undefined quantity of blueberries reduced cholesterol numbers in a 10 person sample study by some mostly meaningless amount. Accompanied by the obligatory claim that if you want a healthy heart, you should eat more blueberries–insinuating it’s because of the cholesterol-altering super-power unearthed by this study.

Perhaps Northwestern does and will have the lowest claims experience among all the life insurers presently issuing dividend-paying whole life insurance. Does that fact on its own make them the best option for whole life insurance? No.

How does NML’s lower claims experience balance out against investment yield, ratio of policyholder obligations to investment income, and/or business diversification outside of life insurance? To name just a few considerations equally important.

Northwestern is a solid company with okay products distributed by a proprietary career force, which it uses to overcome its competitive disadvantages in a broader marketplace. This is actually a great business model for Northwestern and likely the source of its better claims experience. It can charge most policyholders a little more through a sales procedure that isolates the buyer from the rest of the marketplace. That’s a great strategy for company stability and profitability if it can successfully execute–and NML has done just this for some time. But it’s not–in absolute terms–the best deal for the would-be policyholder.