Limited pay life insurance is a type of whole life insurance that has a shorter guaranteed payment period than a traditional whole life policy. There are several types of limited pay life insurance policies all with differing guaranteed premium payment periods. Despite these differences, all limited pay policies operate under an identical principle. I'll spend time today detailing the various types of limited pay policies available. Keep in mind that if your policy varies slightly from what I discuss, the same basic principles apply.

Formal Definition for Limited Pay Life Insurance

A large number of whole life policies issued today require premium payments lasting either to the insured's age 100 or 120. This payment schedule is typical of what we normally call regular whole life insurance.

There are times when an insurance buyer may desire a shorter payment period than his/her age 100+. The life insurance industry is well aware of this, and the solution is a whole life policy with a required payment period much shorter than the insured's conceivable lifetime.

Such a whole life policy is what we call limited pay life insurance. It's also common to hear insurance agents and companies refer to limited pay policies as short pay policies. While there are several types of policies that meet the limited pay definition, the most common types of limited pay policies issued today are:

- 10 Pay Life Insurance

- 20 Pay Life Insurance

- Paid to age 65 Life Insurance

Not too surprisingly, the name of these policies tells us almost everything we need to know about how they function. 10 Pay life insurance requires the policyholder to make 10 premium payments. After these 10 payments, the policy is guaranteed paid-up for the rest of the insured's life. 20 Pay life follows the same basic principle, only the policyholder will need to make 20 payments to reach paid-up status.

Paid to age 65 life insurance requires premium payments to the insured's age 65. There is a subtle uniqueness to this type of limited pay life insurance because the exact number of premiums varies depending on the age of the insured at policy issue. So unlike a 10 Pay policy where all policyholders will pay the same number of years, Paid to age 65 policies will have differing policy premium payment periods as the insured of the policy differs.

For example, a 42-year-old insured will pay fewer premiums than a 34-year-old insured. This is the case because both policyholders must pay premiums until he/she reaches age 65. You should know, however, that the 42-year-old insured will pay a significantly higher premium than the 34-year-old insured for the same death benefit, because of the 42-year-old will pay 8 fewer years worth of premiums.

There are also some limited pay policies that allow the policyholder to precisely dial in a number of premium payment years. The idea behind these policies is that they more perfectly fit someone's unique needs for premium payment years. These policies could look something like 17 required annual premium payments before reaching paid-up status or 9 required premiums. The policyholder chooses the number of required premium years at policy issue and cannot change them later.

Typical Characteristics of Limited Pay Policies

Because the limited number of premiums achieves a guaranteed paid-up status, term-limited life insurance is more commonly used when talking about whole life insurance. This is the case because whole life policies have built-in functionality to become paid-up once the policyholder satisfies a specific condition (i.e. making a required number of premium payments).

While limited pay life insurance most commonly refers to whole life insurance, there is a special type of universal life insurance that also meets the definition of limited pay life insurance. This product commonly goes by the name Guaranteed Universal Life Insurance (GUL). This type of universal life insurance policy can create a guaranteed death benefit after a certain number of required premium payments. Once the policy owner meets the required number of premium payments, the policy cannot be canceled by anyone other than the policyholder. But please note that very few of the additional benefits I'll talk about today concerning limited pay life insurance apply to Guaranteed Universal Life Insurance.

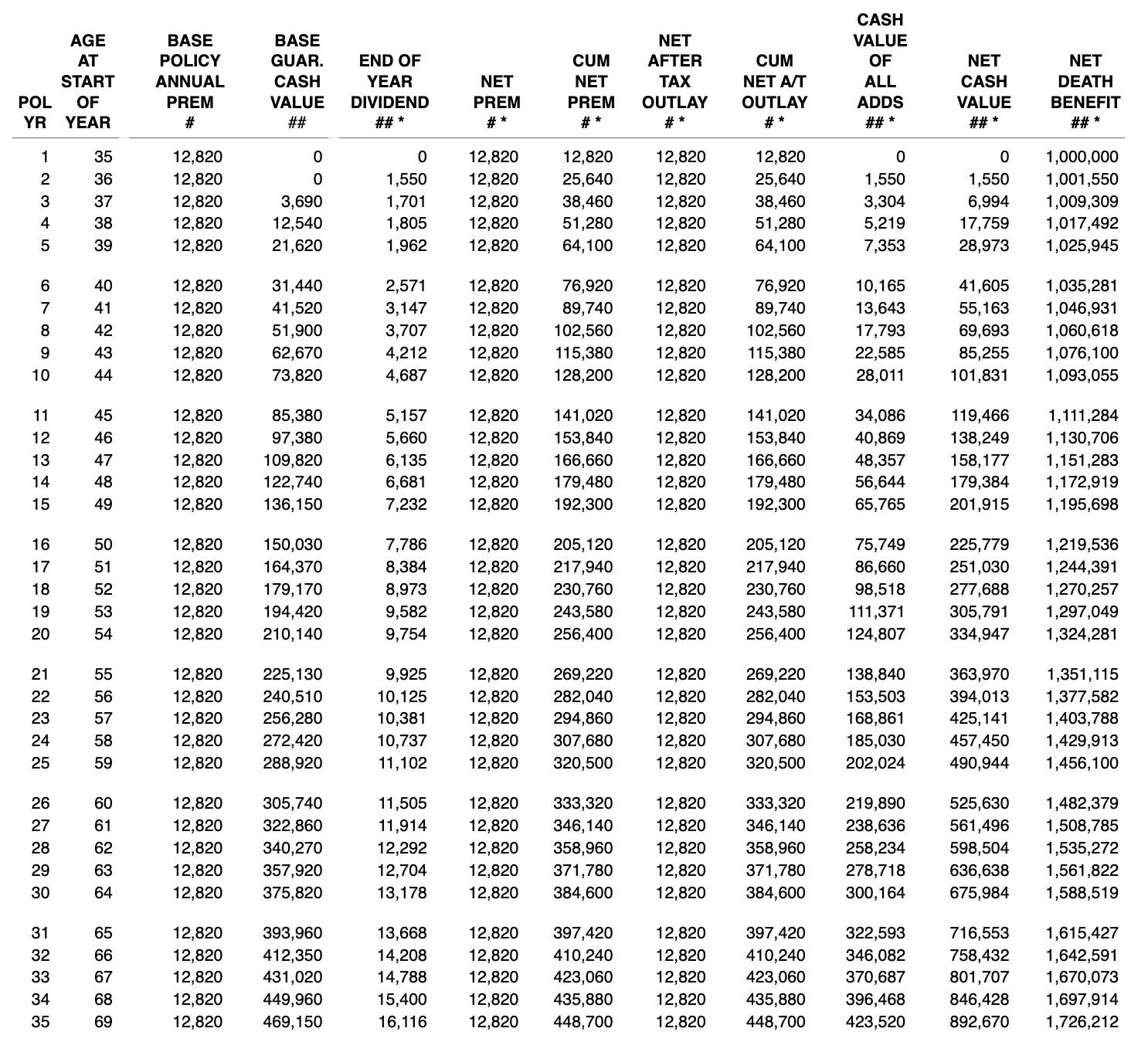

Because limited pay policies have fewer required premiums to reach paid-up status, they do require larger premiums each year versus regular whole life insurance policies. For example, a 35-year-old male looking to buy a $1 million traditional whole life policy (requiring premiums to his age 100) would need to pay $12,820 per year for such a policy.

A 10 Pay whole life policy issued by the exact same company for a $1 million death benefit requires the same 35-year-old to pay $28,600 per year. While the insured must pay more than double the premium for the 10 Pay policy, it does come with the guarantee that after 10 premium payments, the policy is forever guaranteed to remain in force with no future premiums required. With the traditional whole life policy, the insured will not achieve paid-up status until after he makes 65 payments to the policy.

Limited pay policies do tend to accumulate faster cash value than traditional whole life policies. This is due to the increased amount of premium the insurance company collects as part of the shorter payment guarantee.

Using the example above of the 35-year-old looking to purchase a $1 million whole life policy, it doesn't cost the insurance company anymore to insure this individual's life in any given year. So the excess premium that it collects produces additional investment income that the life insurer will typically share with the policyholder in the form of faster cash value build up in the policy.

This also traditionally means that the overall rate of return on premiums paid relative to cash value is higher on limited pay policies.

Are Dividends Still Paid on Limited Pay Whole Life?

Most limited pay life insurance policies are whole life insurance policies, and the vast majority of those policies are dividend-paying whole life policies. Given this, it's easy to understand that many people want to know what happens to the dividend on their whole life policy if it is a limited pay policy.

The answer is you will continue to receive a dividend on a limited pay whole life policy just like you would on a regular whole life policy. In fact, sometimes this dividend is higher than the dividend earned on a regular whole life policy due to the increased premium amount paid in the beginning for the same amount of death benefit.

Limited pay policies will often earn more dividends in earlier years than regular whole life policies. Limited pay policies will also continue to receive a dividend after the policyholder pays the required number of premiums to reach paid-up status. This statement, of course, assumes that the insurance company has profits to pay out to policyholders in dividends, which has been the case for many many years.

Additionally, you should know that all of the dividend options traditionally available on a whole life policy will also be available to you in a limited pay policy.

Can I still use the Cash Value on my Limited Pay Policy?

A limited pay whole life policy functions identically to regular whole life with respect to using cash value. The policyholder can withdraw cash value or take a loan against the cash value. The tax benefits life insurance enjoys are also extended to limited pay policies.

There is no change to this once the policy achieves paid-up status. The policyholder is still free to access cash value through either a withdrawal or loan. Withdrawals to the taxable basis and loans will continue to be income tax-free so long as the policy remains in force.

Example of a Limited Pay Policy's Cash Value Compared to Regular Whole Life Insurance

Here are a few ledgers (policy illustrations) to give you an idea of how limited pay policy values accumulate compared to regular whole life insurance.

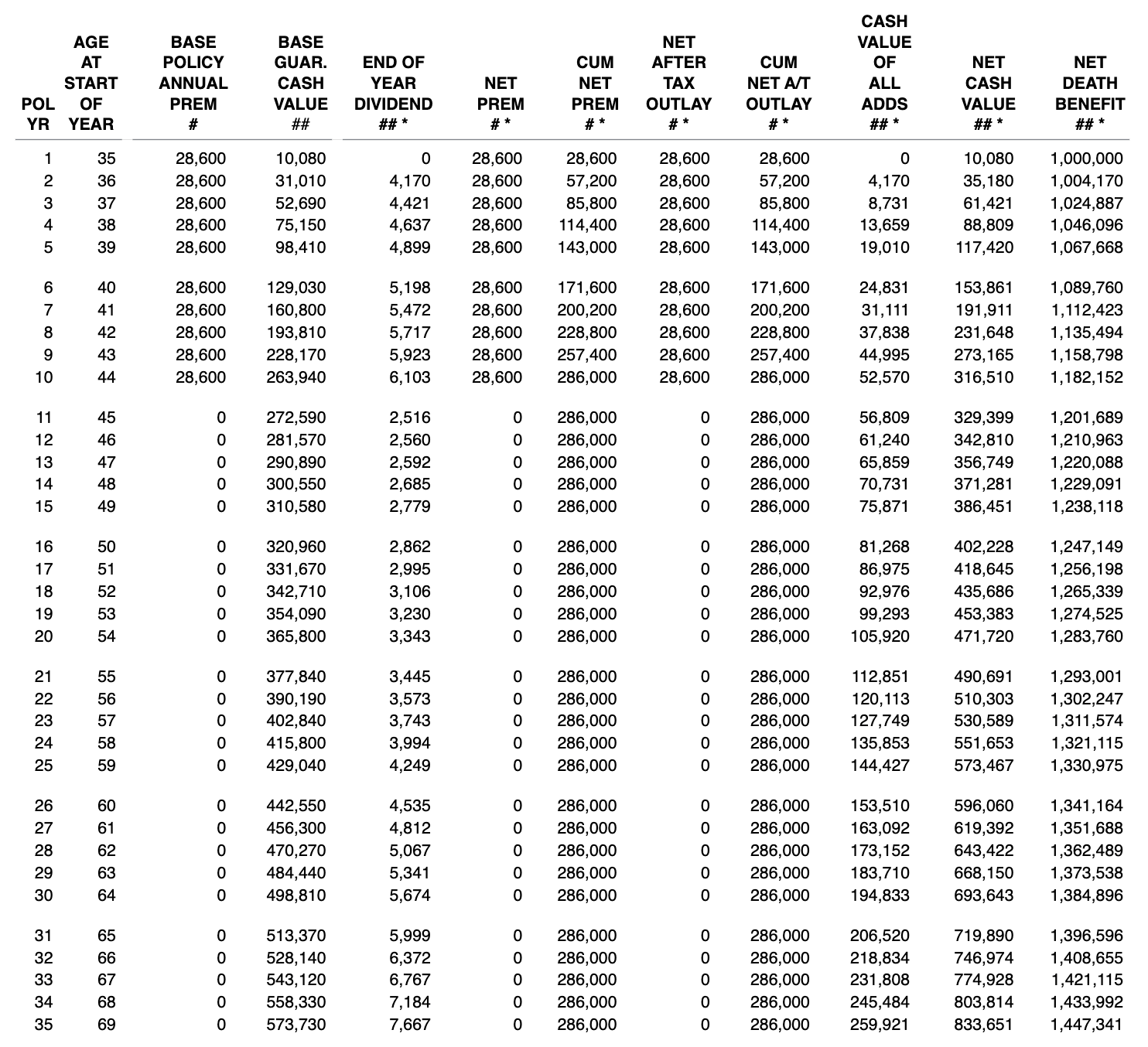

10 Pay

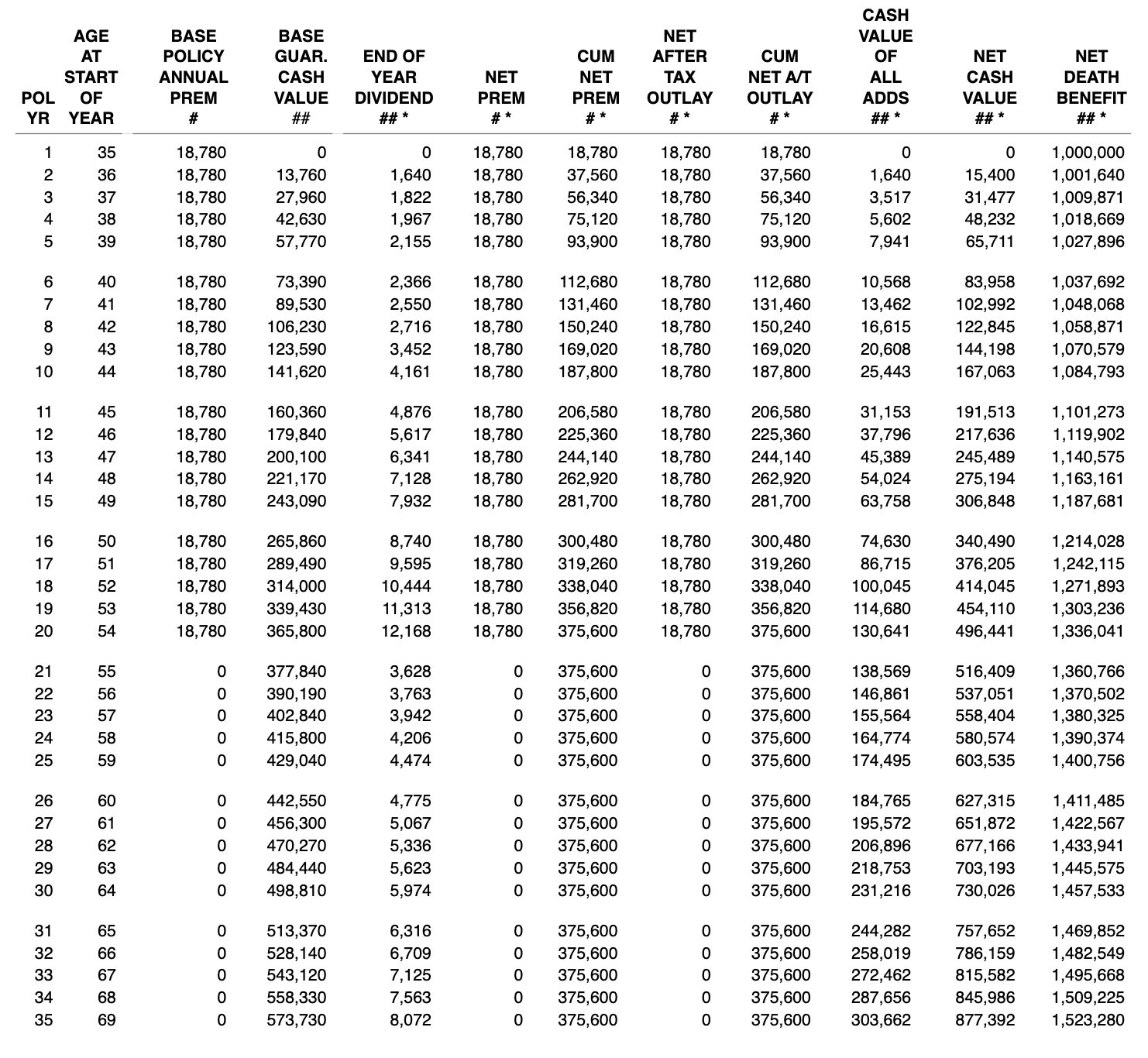

20 Pay

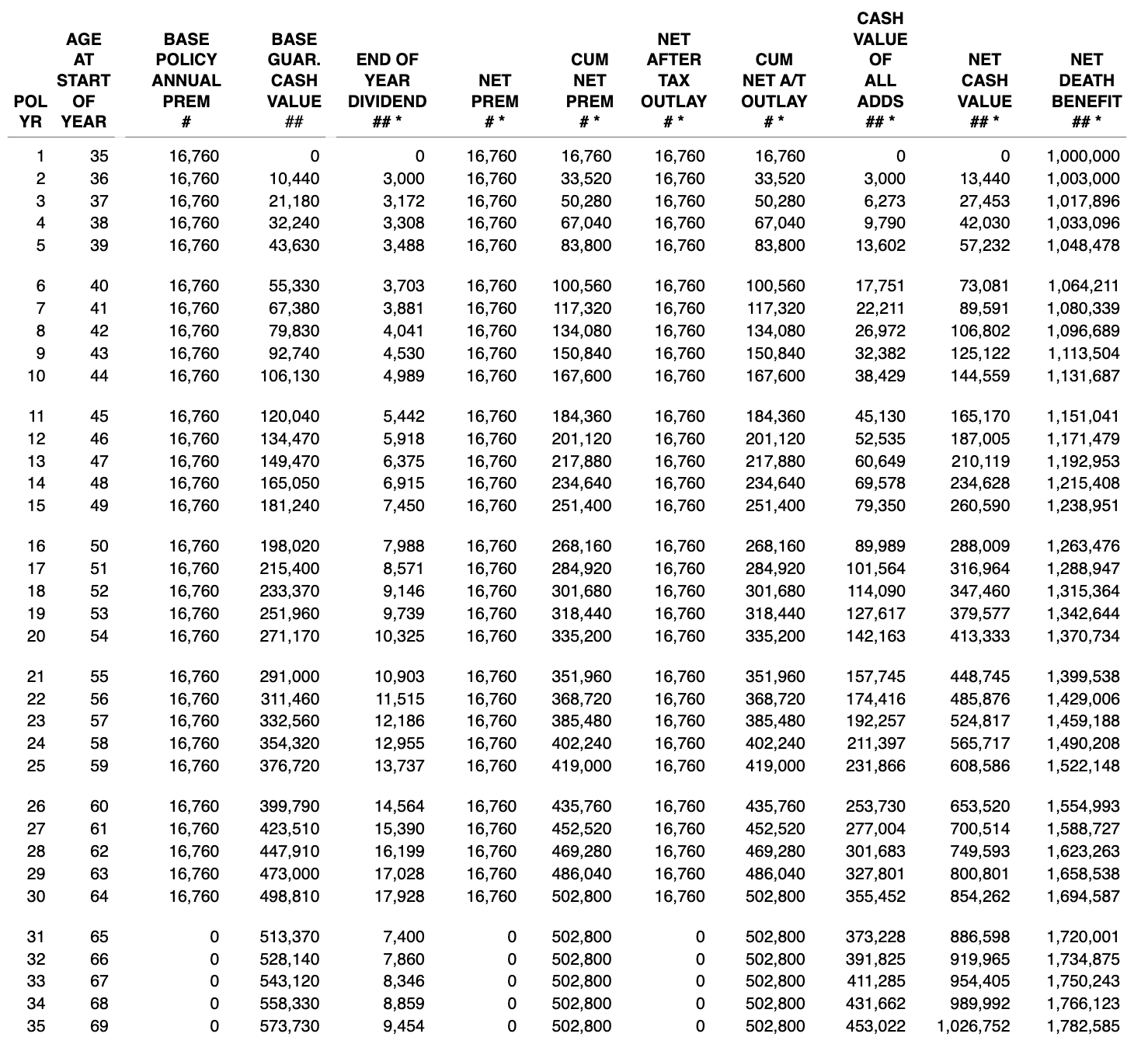

Paid to age 65

As you can see from these ledgers, the limited pay policies do produce more cash value and earn a higher dividend in earlier years. This is because of the higher premium the policyholder must pay for the limited pay benefit. You'll also notice that the shorter the limited payment period to achieve paid-up status, the higher the required premium paid per year.

Limited Pay Pros and Cons

There are both advantages and drawbacks to limited pay policies. While you likely noticed a few already, we'll cover them in more detail.

Limited Pay Pros

The first and most substantial pro to limited pay policies is the ability to more quickly achieve paid-up status. There's something calming about the fact that your policy is now guaranteed to be in force for the rest of your life without any more premiums paid. For some people, achieving this status in the shortest period possible is of the utmost importance.

Second, limited pay policies can produce more immediate cash value and more immediate dividends. In some cases, the net return on cash value is higher with limited pay policies. For people looking to achieve the highest return on their premium dollars in terms of the cash value in a policy, limited pay policies can be a great place to turn.

Lastly, limited pay policies may produce higher amounts of income for those looking to use life insurance as a retirement income source.

Because the policies can achieve paid-up status at or before the policyholder reaches retirement age, the policyholder will owe no more premiums when he/she uses the policy's cash value for retirement income. This will produce a net benefit that is higher than most traditional whole life policies.

Limited Pay Cons

First, the amount of premium required for a given level of death benefit is considerably more than a regular whole life policy. Someone with a desire to achieve paid-up status as quickly as possible may not have the funds necessary to do it with a limited pay policy.

Second limited pay policies are rather inflexible regarding changes to the premium in the future and will pale in comparison to a blended whole life policy both in terms of changing planned premiums and accumulating cash value.

Lastly, not all riders available to regular whole life policyholders are available to limited pay whole life policyholders. Some companies restrict the availability of certain riders due to the limited number of years the policyholder will pay premiums.

Should You Buy a Limited Pay Policy?

The decision to buy a limited pay policy is complex and requires careful consideration of someone's unique circumstances and desired outcomes. Hands down if achieving a guaranteed paid-up death benefit within a specific time period is the number one goal, limited pay policies are the top choice life insurance product.

If your goal happens to be something outside of paid-up status in a short timeline, you should proceed with caution when it comes to choosing limited pay life insurance. It might work for your needs, but there are could be more ideal options.

Thanks, this was a good explanation. If you do purchase a 10 year limited pay policy, can you continue to pay premiums after the 10 year pay period has expired?

Hi Chrisacs, in some cases yes. There are some policies that will allow this, but it involves a rather complex design for the life insurance policy.

Thanks for the answer. I have a rider ( for a child’s whole life policy) called a guaranteed purchase option (GPO). I think that’s a trade name for a set amount, paid up addition. Is that correct? I’m funding it at just under the MEC and the guaranteed assumption table has it “paid up” in eight years. I was just wondering if I can continue paying until the next GPO comes up in ten years. Thanks. I have learned so much from this blog.

The guaranteed purchase option is a rider that allows you to buy an additional policy without underwriting at certain intervals throughout the life of the policy. Paid-up additions are typically referred to as such or some companies call them: additional purchase/premium option, OPP, LSIR/ALIR, EPPUA/APPUA, and LPUA. I can’t tell you specifically what options you have with your policy, unfortunately, but you could reach out to the insurance company or agent of record and could ask.

Hello,

Can you tell me about this account, would it only pay out 1268.00 total, one time payment?

After my [someone’s] death her [someone] got this.

We don’t understand really

Thank you

Tanya

(edits by The Insurance Pro Blog to protect personal information)

Hi Tanya, I think you need to reach out to the insurance company for information on a specific policy.