Using life insurance to generate retirement income is a slightly advanced subject within the world of financial planning.

Stock jockeys hate it, and life insurance agents love it.

No surprise there.

So, is there something that life insurance brings to the table that is truly special, or are you better off betting your chips on the market for a prosperous retirement?

The market and other traditional investments are usually considered weapons of choice for generating retirement income, but maybe, just maybe, there is something your financial planner is missing that isn’t included in the “approved” brochure about retirement income planning.

Risk – We talk about it…a lot

Risk is a funny thing.

Most people have some inherent idea about what it entails, but few of us truly consider how much it affects our lives.

Perhaps this is because we want to be optimistic. Perhaps thinking about the number of risks we face for a task as simple as getting to work each day would make us all clinically depressed—good for Pfizer, bad for our pocket books.

Some risks are easily quantified, like the probability of losing a bet on a slot machine in Vegas.

Others, like the risk of having your house burn down tomorrow, are a tad more complicated to calculate.

For risks that are harder to forecast, we generally assign values in vague estimations (I can’t tell you precisely what the probability is that my house will burn down tomorrow, but I’m confident that it’s pretty low).

There are a number of hazards the future retiree faces in plotting a course to golden girl-hood. Anyone with a license to sell securities is likely to discuss market risk, interest rate risk, systemic risk, and liquidity risk.

But, there are a few factors, such as longevity and cash flow risk, that are often forgotten.

My goal today isn’t to add a bunch of new worries to your list of doom and gloom but to draw a few things to your attention that will help you plan smarter instead of working harder for your retirement.

Timing Risk – Negated by Averages or Serious Threat?

One form of risk that is up for debate within the financial planning establishment is all about timing.

As those of you who are well-read on the subject may already know, timing risk is the possibility you face of entering or being in the market at an inopportune time.

There are many in the bond and equity sales world—especially among the mutual fund crowd—who say that you can minimize timing risk with patience and a nifty strategy known as dollar cost averaging.

The thought is that time averages out returns, so worrying about the timing of your market entry is foolish because you’ll still be making money in the long run.

It’s a solid pitch if you’re selling investment products, and I’ll admit that there is sound logic behind the argument.

But, that logic makes less sense the closer you get to retirement.

Retirement Timing Risk

Despite what most in the investment sales world say, you don’t have forever to wait for the market to come back, even if you are only 22 years old.

Whether we like to admit it or not, there’s a finite number of years between our first and last days at the office. Those 40 to 50 years will define how we finish out our lives, and we only get one crack at it.

So, what’s the probability that your investments will go bust?

That’s actually somewhat simpler to calculate than you might imagine—at least, it’s easier than calculating the probability that I’ll be sifting through the ashes of my house tomorrow, assuming your investments are largely in stocks.

It turns out, retirement timing risk is less about the probability of a market contraction and much, much more about the timing of such an event.

When the Market Brings You a Bear for Your Retirement Party…

If the market brings you a bear for your retirement party, cry.

Bear markets that strike early in retirement can be disastrous. We’ve known this for a long time, but most of the investment world is pretty silent on the subject as it doesn’t have a great answer for avoiding the consequences.

Here’s an example that helps illustrate the point.

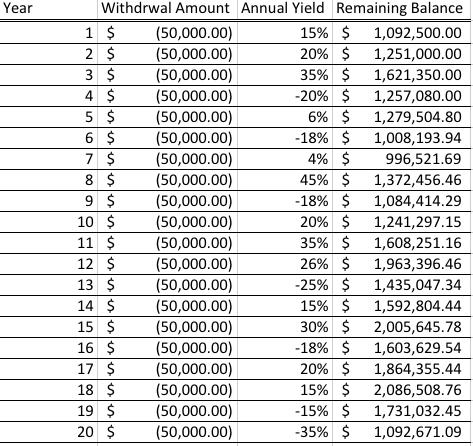

Let’s use a hypothetical $1 million portfolio used to generate retirement income at $50,000 per year in income. This assumes the 5% withdrawal rate that has been the industry standard for decades.

I’ve drawn up a random list of portfolio returns over a 20 year period.

The average return for all years is 6.85%, which is better than the last 10 years of the S&P 500 and a comfortable number according to what most major mutual fund companies tell me I can get with a well-diversified bond and equity portfolio in retirement.

Let’s start with the bull market scenario.

Our first 3 years are really great market years. We see then see a few bears along the way, and towards the end we see some strong bears, but that doesn’t bother us much.

We still wrap up the 20 year period with a million dollars still intact due to market appreciation. This is the sort of dream scenario found plastered on every sales brochure for every mutual fund company in existence.

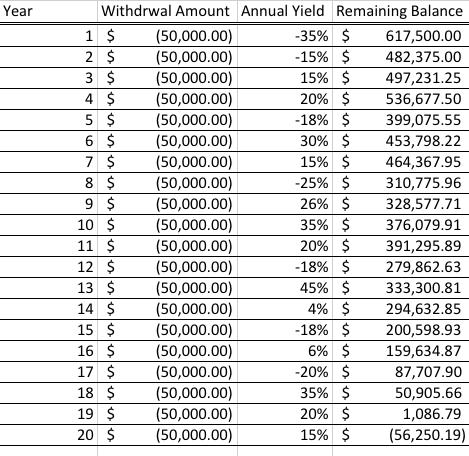

Now the bears come early.

I’ve done nothing but reverse the order of the returns, that’s it.

The average return is still the same, of course, but this time we ran out of money…a year early.

This is what I mean by retirement timing risk.

We can’t control when the market dips will take place, and as such we often can’t prevent a dramatically altered retirement if the market takes a bad turn around the time we’ve crossed out that last day on the calendar.

How Life Insurance Helps Negate this Problem

Life insurance is a low risk asset.

We’ve mentioned this oodles of times. And while most of you will accept that for what it is, reliable, the fact of the matter is this low risk profile makes it a star student when it comes to income generation.

Why?

Because it’s not affected by market dips.

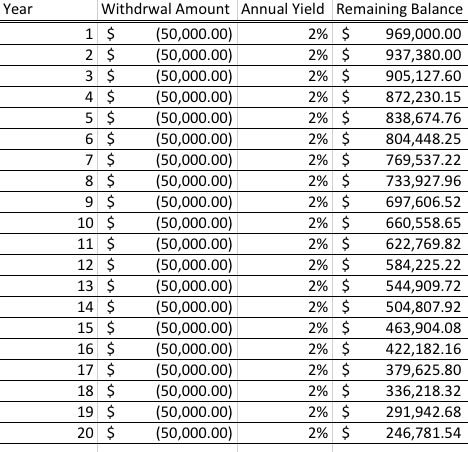

If we go back to our previous example and wipe out all of the hypothetical yearly market returns and replace them with a 2% static return each and every single year, our hypothetical retiree will have made it all 20 years with about a quarter of a million dollars to spare.

Here are the numbers:

If you give me a million dollars and a guaranteed 2% yield indefinitely I can guarantee that you won’t be broke after 20 years if you withdraw $50,000 per year from the account.

That’s mathematical fact.

The guaranteed rate on most whole life contracts is 100% better than our 2% return (and we haven’t even started talking about dividends).

Life insurance works so well for income purposes because it’s so incredibly stable. You won’t generally be excited about it, but you’ll be really happy it’s around when the rain comes pouring down.

Using life insurance to generate income works, and it works well because we can eliminate so many other risks you have staring you in the face that you probably haven’t even considered.

If you want to know more about the particulars and how it can work specifically, go over here and grab our free ebook, “How to Use Life Insurance to Create Tax Free Income.”