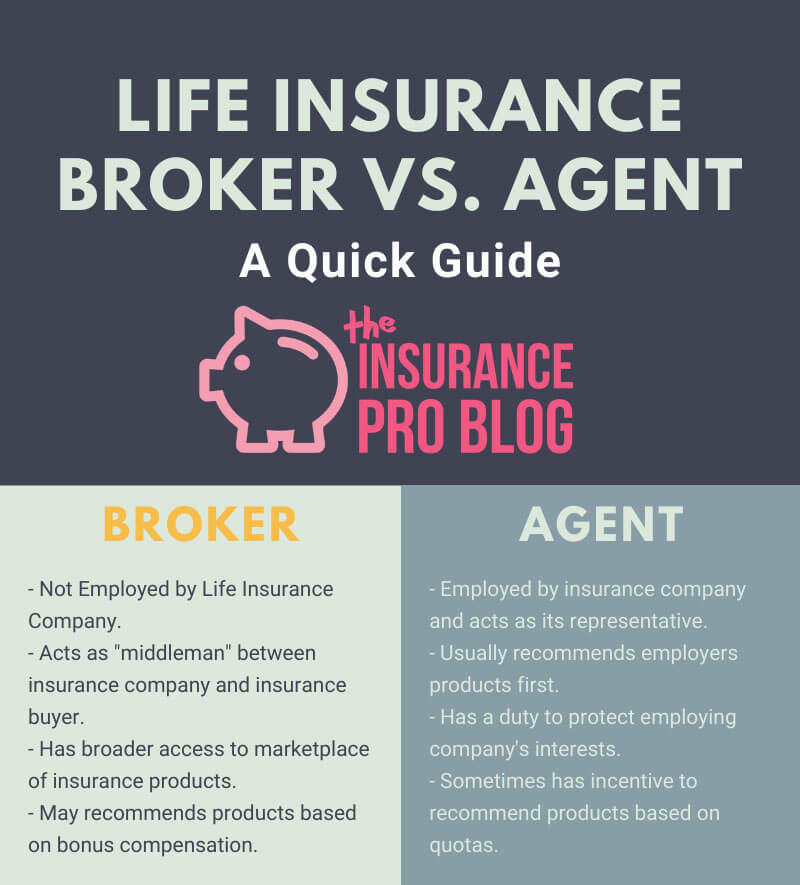

The key difference between a life insurance broker and a life insurance agent is the employment arrangement with an insurance company. Brokers do not have an employment arrangement with an insurance company and have no authority to act as a representative of the company. Brokers merely act as relationship middlemen matching prospective insurance buyers with insurance company products.

Life insurance agent, alternatively, have an employment relationship with an insurance company and act as a representative of that company. Agents have an obligation to serve the company's best interests and this can influence an agent's recommendations to a prospective buyer.

Are Life Insurance Brokers Really Independent?

Brokers have no employment agreement or official obligation to an insurance company. This usually infers that the broker is independent and capable of shopping the marketplace of insurance products for the best fit to a potential buyer's circumstances. While this sounds like a preferred option for life insurance shopping, the truth is brokers aren't always as objective and independently minded as they sometimes market themselves.

For many reasons that I'll get into today, brokers do have conflicts of interest that can cloud their judgment and lead to less objective recommendations.

Sometimes, the subjective recommendations brokers make comes more from ignorance than self-interest.

Still, brokers generally have more ready access to a broader marketplace of insurance products and can more readily access those products.

Are Life Insurance Agents always Biased?

Because life insurance agents represent a specific life insurance company and have certain obligations to that company, they often face criticism for assumed biases and conflicts of interest that influence their recommendations. This criticism comes mostly from the assumed standard operating procedure that agents will always seek to recommend their employer's insurance products over any other company's insurance products unless it is practically impossible for someone to buy the employer's products.

A very common example of this is the “right of first refusal” procedure employed by some life insurance companies. The gist of this system is that the agent must effectively give his/her employer first “dibs” at the prospective buyer. Should the employing insurance company decide the prospective buyer is a bad fit for the company, the agent is then allowed to seek alternative insurance products for the prospective buyer.

The criticism this system faces among some consumer groups is that while the employing insurance company may have products that are adequate for the potential buyer's needs, these products may not be the best product for these needs. In the eyes of this criticism, the agent should be able to tell the potential buyer about his/her other options outside of the agent's employer's list of products, but that is usually a violation of the agent's employment agreement.

While this example is mostly true for some career insurance agents, it's often taken way more literally than agents and their employing insurance companies actually practice it.

Do Brokers and Agents get Paid Differently?

Yes, it is often the case that brokers and agents get paid differently. Agents usually receive commissions for the sale of insurance products through their career agent contract. Agents also normally receive fringe benefits through their employer for reaching certain levels of insurance product sales volume. Examples of this include reduced cost or no-cost-to-the-agent insurance benefits, additional retirement benefits, and/or certain expense allowances for things like office space and other expenses associated with operating their insurance business.

Brokers also receive commissions for the insurance products they sell, but they rarely receive fringe benefits like agents as these benefits are more associated with employment relationships. Instead, brokers often receive additional compensation above standard commission rates paid to agents. These bonus rates seek to assist the broker in covering business operational expenses as well as recognize that the broker doesn't use company resources like the agent might (e.g. have an office paid for by the company, use company stationery, or use/benefit from company-sponsored regulatory training.

Because of this additional compensation available in some fashion to both agents and brokers, there is a potential for self-interested-influenced recommendations to potential insurance buyers.

Agents may recommend his/her employer's insurance products because he/she needs to meet a quota to maintain some benefits he/she currently enjoys.

Brokers might shop the bonus compensation they earn on insurance products and recommend the ones that pay the highest bonus to maximize their profits.

Should you Buy from a Broker or an Agent?

It's difficult to definitely recommend someone do business only with a broker or an agent. Brokers tend to have more experience. It's extremely rare for someone with little to no experience in the life insurance industry to start out as an independent broker. The experience and training necessary to be an effective insurance professional usually require someone to spend at least some time as an insurance agent.

But not all agents are necessarily inexperienced practitioners. Some people remain agents for their entire career and they are skilled at their job in recommending necessary insurance products to people.

Often times, the answer to the question of working with a broker or agent comes down to the specific insurance purchasing need. If you seek a simple term life policy to protect against lost income from early death, the agent or broker debate is arguable less significant. Term life insurance is inexpensive, even if you don't buy the absolute cheapest option on the market, so an agent's access to a broad marketplace is likely less significant.

If you are looking to purchase cash value life insurance and use it for a retirement plan or some other purpose that places a lot of significance on the accumulation of cash value, you are likely best served by a broker who understands this market place, has ready access to multiple products, and understands how each available product best meets various needs under this category of life insurance use.

If you're looking to purchase life insurance as part of estate or business planning recommendation, the agent/broker debate may come down to which person has access to an insurance company with resources to help you manage the life insurance plan. Often times, life insurance companies that focus on selling their products through agents have better resources in this regard. That doesn't necessarily mean you have to buy from one of their agents. Some of these companies also work with brokers.

How do you Know which one you are Working with?

The term “broker” and “agent” aren't always used in their technical sense. Few states recognize brokers officially through licensure–instead, they broadly issue “agent” licenses to both brokers and agents.

The best way to determine the relationship the person you are talking to has with an insurance company is simply asking him/her. Something as easy as, “do you have an employment relationship with this company?” will tell you what you need to know.

I wouldn't expect to determine if someone is an agent or broker simply by looking at his/her business card or whatever other contact material he/she has. Agents and brokers usually use other professional titles like “financial professional,” “advisor,” or “financial consultant” among many other possible titles.

It's also possible to see some insurance professionals use the term broker and agent interchangeably, so I wouldn't assume that if you one title or the other, that person necessarily operates in the technical capacity of the word.