Podcast: Play in new window | Download

If I had a dollar for every time someone asks me is whole life insurance a good investment, I'd have quite a few more dollars in my pocket. But this is a seriously good question, and I know many have talked at length about it–even us.

I believe that answering such a question comes down to two basic considerations.

On the one hand, we have a theoretical contemplation. This encompasses issues about whole life insurance like its tax free benefits, its versatility, and the security is provides.

Then we have the empirical review. This is the cold hard data that either accepts or rejects the notion that whole life insurance could be a good (or bad) investment.

There's a lot to peruse here on The Insurance Pro Blog that addresses the theoretical aspects of if whole life insurance is a good investment. So today, I want to shift focus instead to the empirical data.

But First a Disclaimer

I hold an insurance license. That makes me an insurance agent. This means I sell life insurance. So yes, I can't claim I'm completely an unbiased source of information. A disclaimer stating such was one of the first things I published on this blog way back in 2011 when it began. But this isn't really what I'm looking to disclaim. Instead I want to focus for just a couple of seconds on the word “investment.”

There are some prevailing theories that believe it's a no-no to refer to life insurance as an investment. Some even suggests there are regulations that explicitly prohibit it. I'm not here to explain my legal theory on if someone can or cannot refer to life insurance as an investment in varying contexts. I'm going to note that I'll be using the word “investment” today in a colloquial sense because that's the nomenclature most people assign to “thing-I-use-to-save-for-the-future” and as such it's much shorter and lot quicker than typing “thing-I-use-to-save-for-the-future” for the rest of this blog post.

Is Whole Life Insurance a Good Investment? Historical Data

Many years ago, I published a blog post highlighting the historical performance of a whole life policy. Policy details came from a voluntary disclosure found on an internet forum.

The data on the policy showed that it performed quite well from inception to the current time frame of the discussion. I reference this blog post often whenever asked is whole life insurance is a good investment, and I believe the numbers tell a compelling story about what can accomplish provided proper execution of a whole life policy for this purpose.

But, this data is getting a bit aged. I don't have contact with the individual who shared this data, so sadly I cannot update it. As the years go by, the weight of this data declines and I'm keenly aware of that.

So what to do.

Looking at New Historical Whole Life Data

My career as a life insurance agent spans over a decade, so I ought to have real historical data on whole life policies…and I do.

In fact, I have data on my own whole life policies.

A few weeks ago, I published a blog post that compared the accumulation of cash values in my own whole life policy, versus the results I would achieve if instead I invested the premiums over the same time period in an S&P 500 index ETF.

Here again, we see that a whole life policy designed to maximize efficiency performs very well relative to a broad stock market investment. Taking it a step further, we also see that future projections suggest the whole life policy grows wildly more efficient against the stock market investment.

But that's just one example. Do I have more examples? Sure do.

The Whole Life Policies We Actually Sell People

I could make the following point with my own policy, but to ensure that this works out for more people than just me, I wanted to share the figures from another whole life policy I sold to a client six years ago. This policy uses an identical design to the ones mentioned above.

This policy has performed very favorably. At just six years in, it has already achieved a positive rate of return on premiums paid. The policyholder is sitting on a nice six-figure balance. And this cash is completely unaffected by volatile markets brought on by major news headlines.

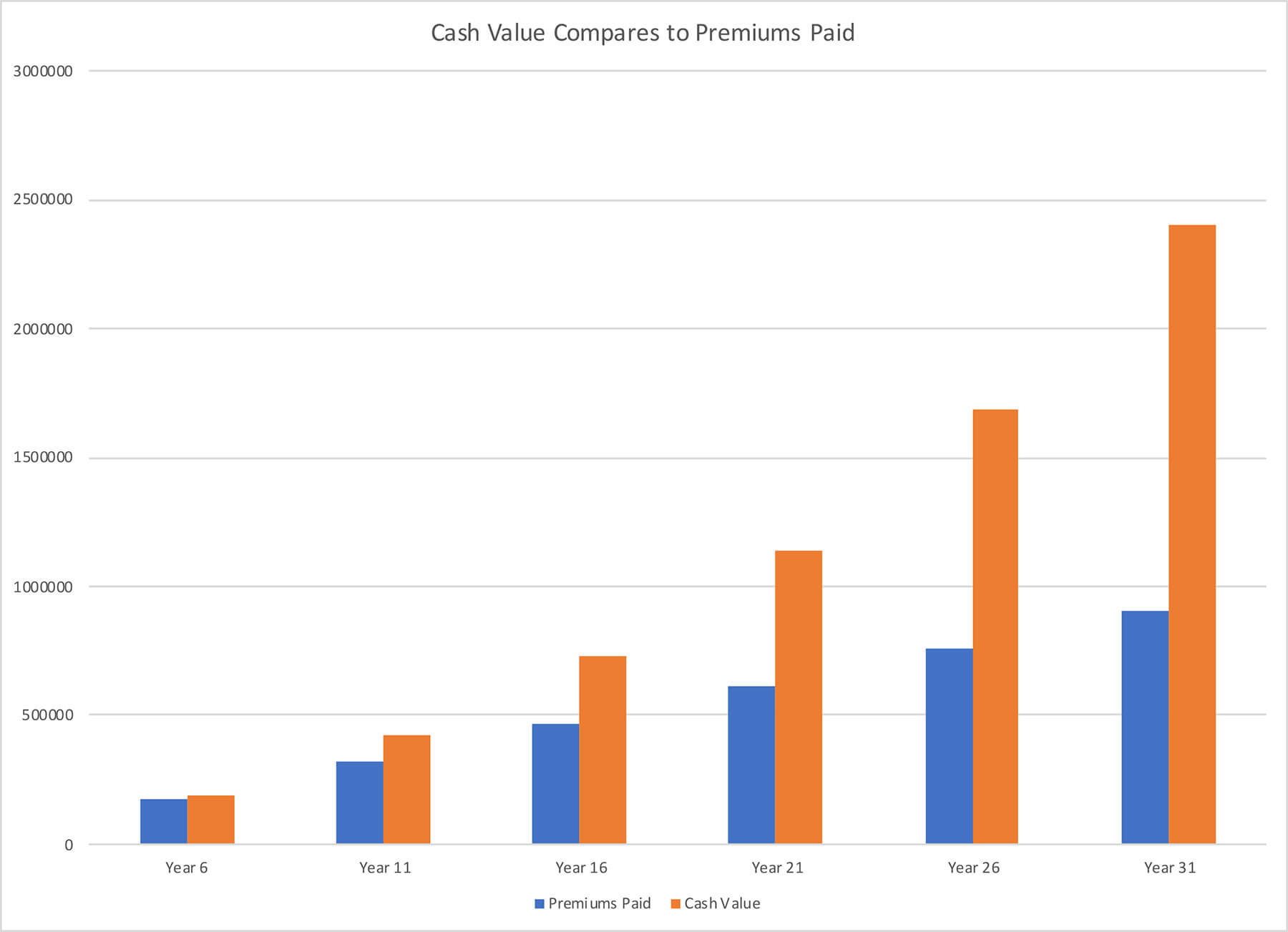

Here's a chart that compares the premium payments to cash value. This chart shows the current situation for the policy in it's most recent policy year as well as future projections:

As you can see, this policy is on a trajectory to produce significantly more cash value than the policyholder paid in premiums. When this policy is in force for 20 years, its cash value will be about double the premiums paid. The cash will continue to grow at a faster pace than the accumulated premiums paid after this point. In fact, by the time this policy reaches its 30th anniversary date, cash values will be closer to triple the sum of premiums paid. This year 30 results represents a more than 5.5% year over year compounding rate of return on the premiums the policyholder paid.

And when I say the premiums, I mean all the premiums. This isn't one of those insurance salesman slight of hands, where we back out some allowance for the death benefit cost to juice the calculated rate of return. Nor is this a tax equivalent calculation where we compare these results to what you'd need to achieve if the cash balance were income or capital gains taxable. If we made any of those adjustments, the effective compounding growth rate is considerably higher.

What about the Guarantee?

Many people take an interest in whole life insurance because they understand there are certain guarantees inherent in every whole life insurance contract. They also usually find out that these guarantees are quite a bit higher than the guarantees found in other insurance contracts, and a lot higher than most other savings/investment options.

Lots of time, the guaranteed column on a whole life ledger looks a tad blah because it makes the almost guaranteed to not be true assumption that the insurance company will never pay a dividend to the policyholder. I always found people who focused on this ledger to miss a much greater point about how compounding guarantees work, when we know some degree of non-guaranteed benefit was practically guaranteed to happen.

What I mean by this is, all the major insurance companies that actively sell manufacture and sell dividend paying whole life insurance plan to pay a dividend to policyholders this year. I'm also approximately 99% certain that they all plan to pay a dividend next year. Understanding this, we know that the fundamental assumption of the initial guaranteed ledger (no payment of dividends ever) is untrue. I've written about this subject in the past, but something interesting came up regarding this guaranteed assumption as I was looking over the above mentioned whole life policy.

I looked at a ledger assuming that moving forward, the policyholder never again receives a dividend payment. If that takes place, the returns are certainly lower. But they are still positive.

In fact, if the insurance company that issued this whole life policy ceased paying dividends from here on out, this policyholder has a guarantee that the policy cash value will achieve a slightly higher than 2.5% year over year rate of return 20 years from now. I want you to hold on to that fact for a point I intend to bring up later.

I am aware of no other financial vehicle that will guarantee a 2.5% compounding return over the next 20 years. And let's keep in perspective just how super unlikely that guaranteed scenario is.

So to recap, the policyholder currently owns a whole life policy that more than broke even within a six year period. That policy is on a growth trend to produce double or close to triple the premiums paid in the future, and this projects around a 5.5% rate of return on the premiums paid. At absolute world-falling-apart-worst-case-scenario this turns into a 2.5% return over the years. And let's not forget that here's also a chance that economic conditions improve to a point where the actual dividend paid is higher than currently assumed, which would result in even higher cash values.

On top of all this, the policyholder avoids complicated and annoying tax consequences associated with other investment options.

How Whole Life Insurance Compares to Other Investment and Saving Options

While the above information lays out a fairly compelling argument for why we say yes to the question is whole life insurance a good investment, I think we need to also spend some time looking at other data points regarding other investments to contemplate just how good whole life insurance is. The best way to arrive at a full understanding here, is to understand where whole life insurance falls in relationship to some of the alternatives.

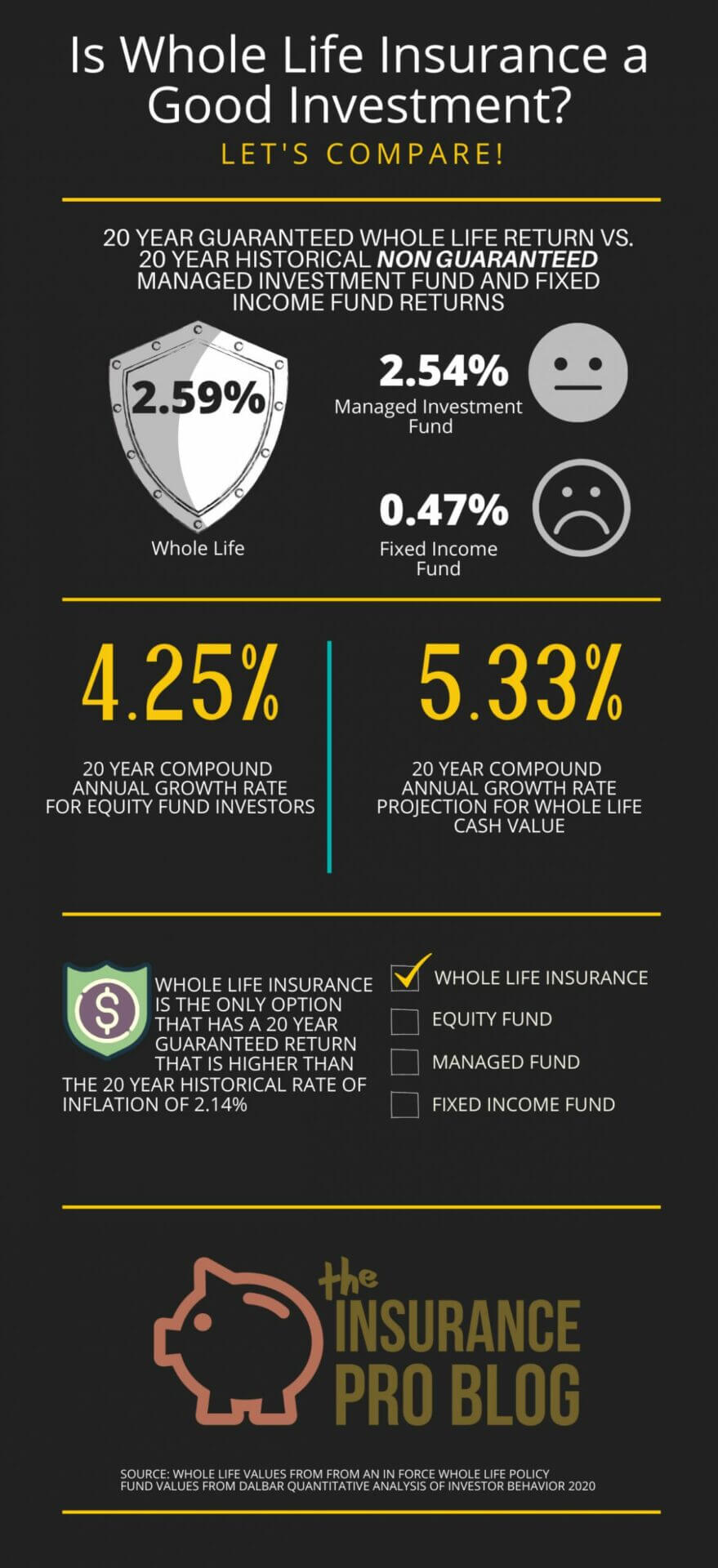

Every year, the Massachusetts based company DALBAR releases its Quantitative Analysis of Investor Behavior (QAIB) report. This analysis seeks to evaluate several aspects at the intersection of human thinking and investing outcomes. The DALBAR analysis shows year-after-year that human psychology is not well equipped to handle the mental toughness required for volatile investing–even when volatility is relative light.

One of the most fascinating data points from the QAIB is a multi-year rundown on investor performance for an array of investment allocations. These include: equity funds, fixed income, and tactical allocation funds. The most recent QAIB report shows us that investors faired better very recently, but long term performance falls well short of the targets most financial advisors and gurus setup for expectations.

Still, despite achieving decent results over the past three years, investors still lagged broader market indices, which eludes investors year after year. Looking at a much more extended time period, the data for investor achievement is much more sobering.

According to DALBAR, the top performing investment allocation for the past 20 year period is equity based funds. No real surprise there. What is surprising is that this top performing investment allocation achieved 4.25% year-over-year growth over the past 20 years. Fixed income fund investors showed the worst results over the past 20 years at just 0.47% year-over-year growth. That datapoint blows my mind knowing that most bond yields were significantly higher than this over the the same time period. The managed allocation fund investors (those who pay slightly more on average to have some extra degree of tactical management supposedly shepherding the fund's money) managed a 2.54% year-over-year rate of return.

Now, comparing these results to some benchmarks. The year-over-year growth for the last 20 years for the S&P 500 index was 6.06 according to DALBAR. The Bloomberg-Barclay's Aggregate Bond Index performed 5.03% year-over-year for the past 20 years. And inflation during these last 20 years wore away 2.14% of purchasing power each year.

So as you can see, all investment funds fell far short of their benchmark indices during the past 20 years. One of them even fell far short of the returns needed to surpass inflation. Those investors would have been better off spending the money on vacations and shinny toys.

But let's get back to that whole life policy I mentioned above…

In just six years, it's already achieved a year-over-year return above 2%. It's 20 year projections show results ahead of all the 20 year fund results from the DALBAR study. Even its future guaranteed values exceed the fixed income and tactical allocation fund results over the past 20 years. Here's a recap of everything:

So whole life insurance compares very favorably to other options one might chose as a “real” investment. Additionally, whole life insurance provides significantly higher guarantees than the other options.

But I don't want anyone to read this and walk away thinking that I'm telling you whole life insurance is the end-all-be-all investment option. Again, (one more time for the regulators) it's not an i-n-v-e-s-t-m-e-n-t. I do believe that there are plenty of option inside the world of equities that will most likely provide higher returns in a nominal sense than whole life insurance. I think you're very short-sighted if you overlook the benefits that equities can provide you.

Whole life insurance is an excellent complement to your portfolio in many circumstances. When designed to maximize efficiency, it can produce very solid returns. Its guarantees enhance at it ages when it earns dividends. And there is no other option available with more stability. That last point is hard to appreciate when you're young and lack the experience of living through turbulent times with lots of money on the line. But it's one of the most commonly mentioned benefits our clients note when we discuss their whole life policy.

How do you usually structure a policy for someone seeking maximum cash value accumulation, the ratio of how much should go towards base premium and paid up additions?

What would be the disadvantage?

Hi Rob, this is a question with no easy answer. There is no specific ratio as insurers differ in what they allow. They also differ in how expenses play a role in design. What might be a great ratio for one insurer will be sub-optimal for another for a few reasons. I don’t understand the disadvantage question.