Podcast: Play in new window | Download

Velocity banking is a strategy that uses a home equity line of credit (HELOC) to payoff debts instead of traditionally paying down debts simply with the money that you earn each month. Advocates for velocity banking claim that using it will help you reduce/payoff your debts much faster and greatly minimize the interest that you pay on said debts.

There is also a school of thought that seeks to use velocity banking to cover not just debts, but everyday living expenses as well through a HELOC. This group believes that home equity of mostly dead money and serves you little purpose, so it's best to put it to work wherever and whenever possible.

The idea actually has some solid math behind it, but not everyone will face circumstances that warrant the potential upside velocity banking potentially offers. Additionally, the actual implementation of such a strategy is much easier said than done. So we're going to walk you though the specific details of velocity banking, note the plus sides, point out the possible downsides, and elaborate on why this subject comes up on a blog dedicated to the subject of life insurance.

Traditional Velocity Banking Example

Suppose you own a house worth $250,000 and on said house you currently have a $150,000 mortgage balance. Suppose also that, like many Americans, you have several other debts you must service every month. These include: car loans, credit cards, personal loans, student loans, etc.

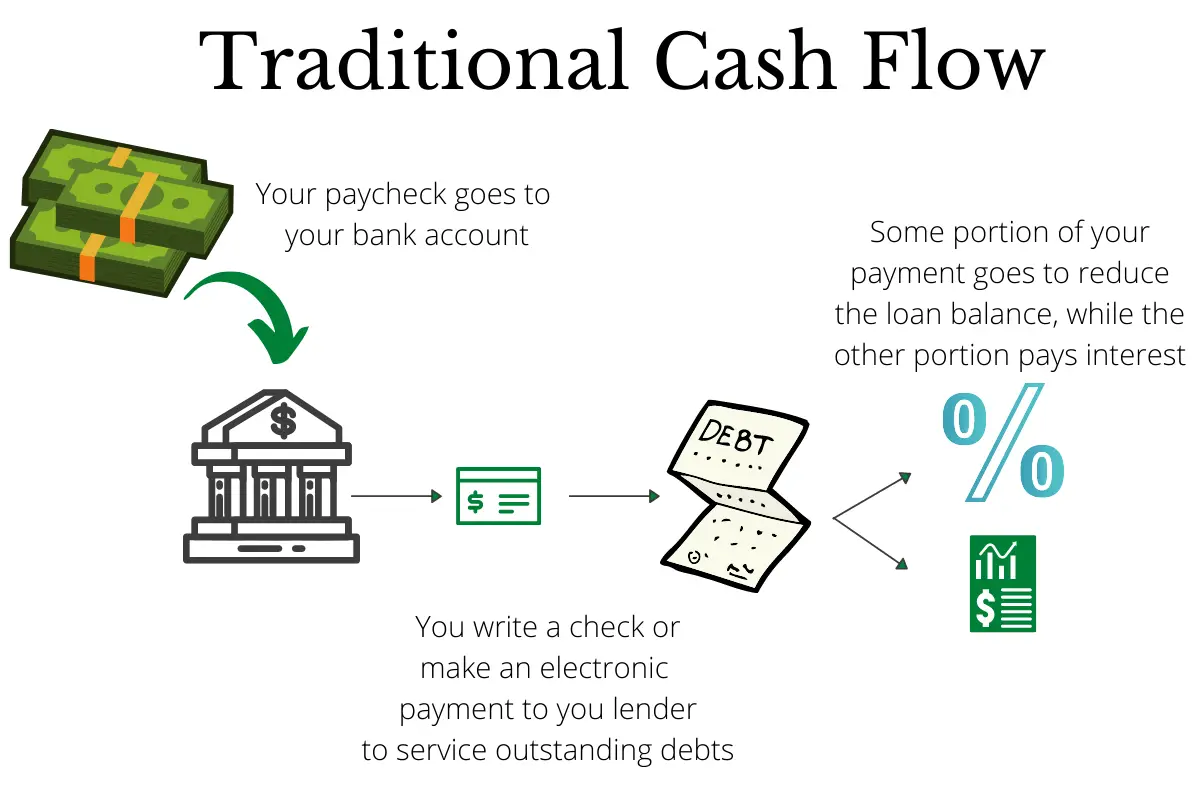

Normally, you would make monthly payments on the various debts you have by taking money in your checking account and writing checks or drafting electronic payments to the lender. A graphical depiction looks something like this:

When you tackle debt in this fashion, you often end up paying lots of interest up front as many debts are amortized (fancy finance term for spread out) in a fashion that ensures the bank receives the majority of its interest up front. This protects the bank's income from both default by the borrower and refinancing.

When you tackle debt in this fashion, you often end up paying lots of interest up front as many debts are amortized (fancy finance term for spread out) in a fashion that ensures the bank receives the majority of its interest up front. This protects the bank's income from both default by the borrower and refinancing.

Here's an example of how this breaks down graphically:

According to this graph, the very first payment made on this mortgage sends over 80% of the payment to interest and less than 20% to the paying down the principal balance. This remains the case for the first two to three years. After 18.5 years of payments, the monthly payment finally crosses over and the majority of each payment goes towards paying down the principle balance, with the remainder paying interest.

To quantify this, let's go back to the example I laid out where you have a $250,000 house with a current mortgage balance of $150,000. Let's assume that the original mortgage was $200,000. Your first mortgage payment would be somewhere around $952 per month with a 4% interest rate and a 30 year fixed mortgage. Using the above chart, this means your first mortgage payment is around $790 in interest and $162 in principal balance repayment.

This payment scheme ensures lenders earn most of their profits first, and it keeps borrowers indebted longer, which can make the cost of borrowing money more than many borrowers might assume.

There are other ways to approach and manage debt, we covered this a few times when discussing life insurance policy loans. The simply interest method that life insurance policies use can make an higher nominal interest rate actually cost less versus a bank loan that uses the above-outlined amortization method.

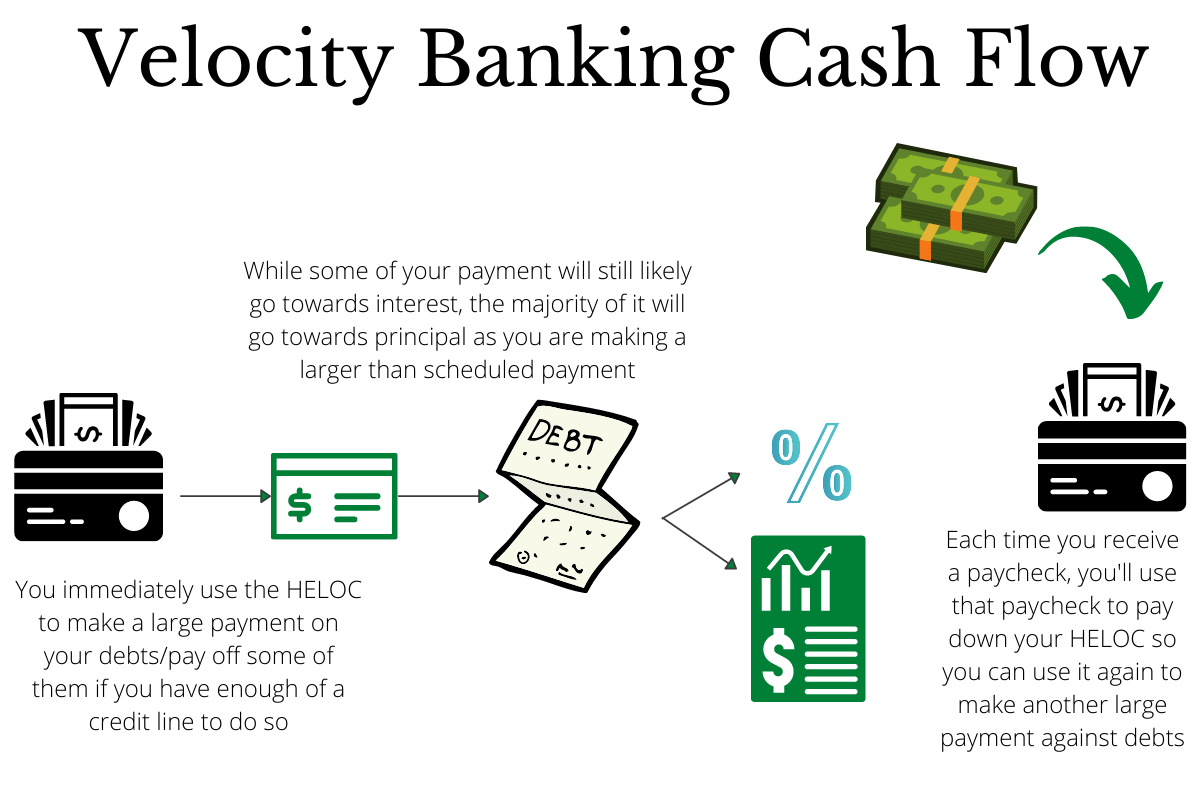

Velocity banking uses the exact same principles we outlined in previous blog posts to reduce your borrowing cost. Here's how it works, in theory:

You apply for a home equity line of credit (HELOC) or whatever other line of credit options you have available if the HELOC isn't an option for you. As soon as you receive approval and open up the HELOC, you draw down almost the entire line of credit (some advocates suggest that you should leave some untapped line of credit in case of emergencies) to pay off or down balances of your debts. When you receive your paycheck, you will use 100% of it to pay down your HELOC. In effect, you deposit your paycheck into your HELOC instead of into your checking account. For some people this will actually take the shape of depositing your paycheck into a checking account and then manually transferring all of it to your HELOC by making a principal payment to your HELOC.

Once you pay down the HELOC with your paycheck, you will again make a payment towards your debts with the new unencumbered credit line you freed up with your paycheck funds.

Velocity banking potentially saves you money because the HELOC charges interest based on the average daily balance of the HELOC throughout the month. The required payment you make to the HELOC is only the interest, and that interest calculation is simply the balance of the HELOC. The interest payment is not a combination of interest and principal reduction where the bank loads up the payment on the interest side.

Velocity banking potentially saves you money because the HELOC charges interest based on the average daily balance of the HELOC throughout the month. The required payment you make to the HELOC is only the interest, and that interest calculation is simply the balance of the HELOC. The interest payment is not a combination of interest and principal reduction where the bank loads up the payment on the interest side.

Additionally, if you carry unsecured debts (e.g. credit cards and personal loans) you likely pay significantly higher nominal interest rates on these debts than you would on a HELOC. This alone could save you a pretty significant sum.

Using the velocity banking concept in this context, primarily to pay down unsecured/high interest debts, is certainly a viable way to reduce and eliminate debts much faster than the traditional method of making payments on them.

Using Velocity Banking to Payoff your Mortgage

Once you eliminate other debts, Velocity banking advocates also suggest you can use this strategy to accelerated paying off your mortgage. You apply the same principals as before by using the HELOC to make a large principal repayment to your mortgage and then use your paycheck to pay down your credit line balance.

The key principle in play here is the idea that large principle repayments will significantly reduce the total amount of interest accumulated on your mortgage. What's more, the equity line of credit can acts as a safety relief valve should you run into a cash flow crunch and need some of the money back.

But here you have to spend some serious time doing some simple calculations to determine if you will truly save any money. The simply interest calculation the HELOC uses will not all on its own necessarily result in a lower overall borrowing cost versus your mortgage.

In the example I used above, the $200,000 initial mortgage has an estimated interest payment in year one month one of $790. If you had a HELOC for the entire $200,000 (tricky, but not impossible and we'll get into that in the next section) your very first payment required payment to the HELOC would be $667 assuming a 4% interest rate. BUT…HELOC's rarely have lower interest rates than 30 year fixed mortgages, so we have to take this into account. If the HELOC interest rate is 5%, the first interest payment is $834. That's $44 more than the 30 year fixed mortgage. Now, the HELOC method of calculation interest might reduce the interest payment more rapidly than the 30 year fixed mortgage would (especially if you are using your entire paycheck to pay down the balance), so there's still a chance velocity banking comes out ahead. You'll have to run the calculation for your specific situation to see if that's the case.

Usually, the velocity banking recommendation isn't to refinance your entire mortgage with a HELOC (but there are some, and that's what I'll cover in the next section). Instead, the recommendation is to use your current HELOC with a much smaller allowable credit limit than your mortgage balance, you make “chunk” payments towards your mortgage to reduce the balance. In other words, you are trading out mortgage debt for HELOC debt and potentially paying less interest because the of the simple interest calculation on the HELOC. Eventually, you'll payoff the mortgage and reduce the HELOC balance to zero. In some circumstances, this will happen more quickly than just making extra mortgage payments with the cash you have in the bank.

Using Velocity Banking Concept to Buy a House and Retain Equity as Buying Power

Taking things a step further, some people use this principle to purchase a house with a Home Equity Line of Credit. In this case, the HELOC is in the “first position” and no traditional mortgage exists. It's not an easy task, and will require some significant leg work on the buyers end to locate a bank willing to issue such a HELOC for such a purpose.

Once you purchase the home with the HELOC, you apply the same basic principles. Each time you receive a paycheck, you'll use 100% of it to pay down your HELOC. When expenses come due, you simple use the HELOC to pay them, which does increase your outstanding debt load, but you'll minimize it again when you receive your next paycheck.

This twist on velocity banking requires you to strongly hold the following beliefs and have the following non-negotiable circumstances:

- Home equity is dead money that serves you practically no purpose so long as you continue to live in the home.

- You must absolutely earn more money than you spend each month (otherwise you'll eventually run out of credit line to use for expenses).

- You have to understand that all HELOCs will eventually require refinancing or else you'll be required to repay the HELOC balance (often all at once as a balloon payment).

- Preferably you do not already carry lots of other debts and have a reasonably high credit score.

Velocity Banking and Life Insurance

If you happen to own cash value life insurance, you could apply the principles of velocity banking with it. You'd simple use a policy loan in the same fashion one uses a HELOC with velocity banking. This allows you to use the same simple interest calculation HELOC's use as life insurance policy loans are very similar.

The only exception to this would be the third strategy I outlined above. Since life insurance loans use cash value inside the policy as collateral, you won't be able to extract additional value by virtue of having untapped home equity. You could, potentially buy a home with a life insurance loan and apply for a HELOC to use in case of an emergency.

There are also some agents who advocate using HELOC's to purchase whole life or indexed universal life insurance as a means to build wealth through the cash accumulation feature of these policies or to leverage the death benefit of a life insurance policy for greater legacy value. I'm always cautious about this idea because I'm nervous about the risk it poses to ones home. If, however you have plenty of other assets to pull you out of a bad situation, it might be worth a look.

Does Velocity Banking Work?

The principles of velocity banking do have reasonably solid logic behind them. But you absolutely must spend some time working through the math to determine if it makes sense for you. This is not a silver bullet and it will not absolutely be your best option to pay down debt and/or payoff your home. The last strategy I outlined isn't so much worried about absolute interest savings as it is keeping an open line of money available through equity, so that one is harder to quantify what makes it a good idea or bad idea. It's much more a philosophical approach to money than an absolute mathematical solution to a problem.

This is also a strategy for the more hardcore DIYer. Those who aren't willing to actively manage such a strategy, or who feel a bit intimidated by intermediate financial concepts should steer clear of this. There are also a fair number of risks one takes on to employ this strategy, and I'd caution the risk averse to keep some distance from this.

Great piece! Also want to point out banks have a way of freezing HELOC’s when things aren’t going their way so always keep that in mind. I am also a registered rep and my BD does not allow us to use home equity to fund life insurance. Again as you point out the math could work, but not sure it is prudent.

Also, the banks can call those loans due.

Thank you Brandon,

Excellent Segment on Velocity Bank – please which lender can I speak to consider their HELOC offers?

Thanks for the feedback Pauline. We do not make recommendations on lenders.

I appreciate your review on the topic of velocity banking and infinite banking.