Podcast: Play in new window | Download

Universal life insurance is really not that interesting, but you'd never guess that by reading pretty much anything that gets published about it in the mainstream press. In fact, it has been featured in the WSJ more than a couple times in the last several years.

Each time, the story gets a little worse. I'll get to that a little bit later but first let's go over a small review of the basic mechanics of a universal life insurance policy. Take a couple of minutes to read through this as a refresher or quick start lesson depending on where you are with your knowledge of universal life insurance policies.

Universal Life Insurance Insurance Fundamentals

Fantastic flexibility is built into universal life insurance, you can loosely consider it a “pick a payment” type of life insurance policy. When it reached peak popularity in the 1980's, this idea was new and a wide departure from the rigidity of whole life insurance.

One of the nice things about universal life, there's no set premium associated with your particular death benefit. There are expenses associated with providing that death benefit but the amount of money you pay in premium to the policy is at your discretion.

You must cover the policy expenses to actually keep the policy, if you don't do that, the expenses will be deducted from the cash value of the policy. But effectively, every dollar you pay to a universal life insurance policy is credited to the cash value.

Remember, that we all have the luxury of hindsight today. Up to that point, the only options for life insurance were not flexible at all and had only a secondary focus on efficient cash value accumulation. Universal life disrupted quite a few things in the life insurance industry. Some good, some not so good.

Good: it's possible for the policy owner to load the policy with cash and to grow the cash value of the universal life policy very rapidly.

Bad: when a policy owner is told by someone, “you don't need to pay that $10,000 annual premium for a $1 million whole life policy, that's too expensive. You could by universal life insurance and pay $2,500 a year for the same $1 million coverage.”

Problems ensue when this happens. And unfortunately it would seem that it happened more than it should have back in the early proliferation of universal life insurance policies. We can all agree that selling these policies with a “race to the bottom” sort of price-positioning is rife with peril.

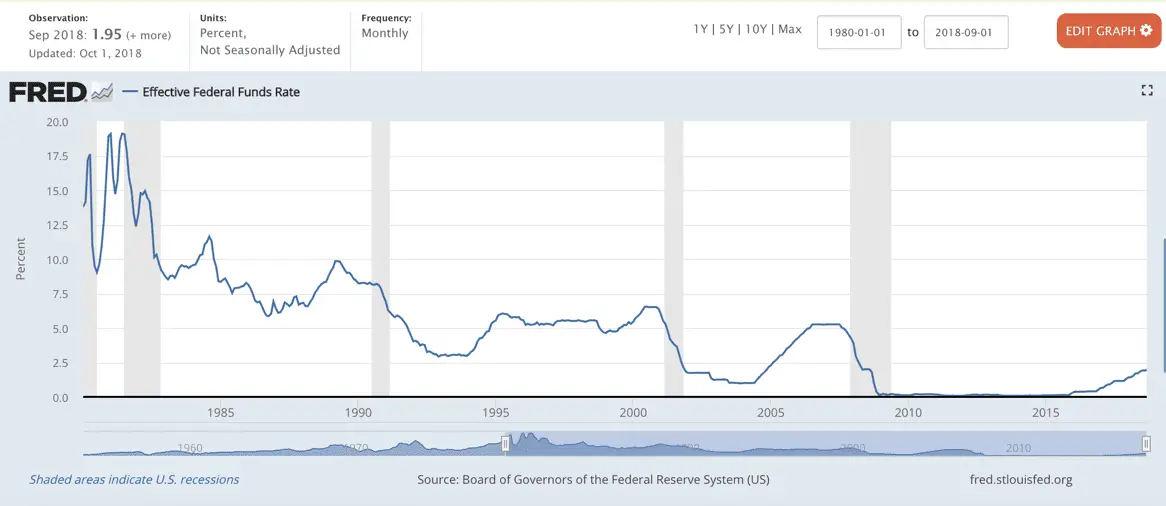

Remember, the underlying interest that's credited to the cash value in universal life insurance policy is the magic lever. If the interest rate that's illustrated is way higher than the actual interest that is credited over the life of the policy, bad things happen.

Interest Rate Highs = Race to the Bottom for Universal Life Insurance

Back in the 80s interest rates were sky high, probably hard for many folks to remember, we've not seen anything like it since. In fact, the general trend of interest rates has done nothing but fall over the last 35 years.

Unfortunately, there were quite a few policies sold back in the mid-80's that assumed a 10% interest rate would be paid for all years of the policy.

Going back to our fundamental understanding of universal life insurance for a second…illustrating a policy with a 10% rate would have made the premium necessary to sustain the policies artificially low.

Listen to here more.

A simple way for companies to check on underfunded policies is to flag ones where the policy value is projected to decrease over the coming year. This typically gives about a 10 year warning for a lapse. clear options need to be shown for how to increase the premium or decrease the benefit.