Podcast: Play in new window | Download

Indexed universal life insurance can be a good choice for retirement, but you should understand that it works as an option to complement your investments and other retirement planning tools. The top three things that make indexed universal life insurance a strong tool for retirement are:

- Its protection against losses

- Its ability to produce tax-free retirement income

- Its ability to pursue slightly more aggressive returns regardless of your age

Protection Against Losses

Indexed universal life insurance accumulates cash values based on premiums you pay and an interest paid on the cash value created by those premiums. The actual interest rate depends on the movement in an index (usually a stock index) over a certain period of time (most commonly one year).

But despite paying interest commensurate with movement in a stock index, indexed universal life insurance does not decline in value if the market is down. In fact, all indexed universal life insurance policies have a minimum accumulation guarantee. The unique functionality of indexed universal life insurance ensures against losses. This protects you from losing money when the economy takes a turn in an undesirable direction.

Tax-Free Income

Like all forms of cash value life insurance, indexed universal life insurance enjoys several tax benefits. One critical benefit for those seeking to use life insurance to create retirement income is the ability to keep all income created by an indexed universal life insurance policy tax-free.

Tax-free income from life insurance has more implications than just not having to send a check to Uncle Sam on the money you take out of the life insurance policy. The income you create from a life insurance policy does not count towards provision income. This means it will not affect the taxability of your Social Security earnings.

More Aggressive Returns at Advanced Age

The indexing feature mentioned above can produce a very high rate of return for a fixed interest savings plan. Many indexed universal life insurance policies available today have the potential to produce a low double-digit interest payment on the policy-owners cash value. Indexed universal life policies can do this and still protect your cash value from losses if the market declines.

Imagine for a moment that you own an indexed universal life insurance policy with $500,000 in cash value. The market is up for the year and you earn 10% on this cash value. That means you'll earn $50,000 in interest that will add to your cash value.

Investments or other savings plans that have the potential to achieve this sort of return also require you to accept the risk of losing some or all of the money you have saved in the plan. This is not the case with indexed universal life insurance. You can remain in pursuit of a low double-digit return on your money all the while knowing that the worst-case scenario if you earn no interest in a given year (this might result in a small net loss for the year as a result of insurance expenses being covered by your cash value, but you can always find out what this amount is and it will never be anywhere close to all of your cash value in the policy).

Will Indexed Universal Life Insurance Produce Guaranteed Income?

No, indexed universal life insurance does not produce guaranteed income per se. It does, however, produce an extremely stable income because it lacks the downside exposure to the loss mentioned above.

This being said, if you absolutely require guaranteed income from savings or an investment, you are most likely best served by an annuity. You will find that the non-guaranteed but still very stable income you can create with an indexed universal life insurance policy is higher than the guaranteed income created by an annuity.

Should you use Loans or Take Withdrawals to get Income from the Indexed Life Insurance Policy?

For indexed universal life insurance, you will almost always use loans for income creation. Indexed life policies with an “indexed loan” feature will certainly offer an attractive way to create income through a policy loan. These types of loans allow you to remain in the index while you take a loan against the policy. This creates the potential to earn more on the money you pledged for the loan than the loan interest rate that accumulates on this money.

Withdrawals are rarely used for income creation with universal life insurance policies because of the indexed loan feature. Also, many universal life insurance policies offer other loan features that offer more benefits to the policy-owner than simply withdrawing the cash from the policy.

To be clear, you can withdraw money from a universal life insurance policy if you want it. But doing this is likely less optimal than using the loan features you have available.

Do you Have to Payback the Loans you Take to Create Income?

No, you do not need to repay the loans taken out to create a retirement income from a life insurance policy. So long as the policy-owner dies while the policy is still in force, the death benefit of the policy will pay off the loans and the remainder will go to beneficiaries.

This planned outcome will also ensure that all income created by the life insurance policy remains tax-free.

What's the Best Way to Design an Indexed Universal Life Insurance Policy to Produce Good Results for Retirement?

While indexed universal life insurance can be a great option for retirement planning, you must ensure that you have the appropriate type of policy and correct implementation of that policy for the correct results. If you do not buy the right policy type, or if your agent designs the policy incorrectly, it will not work well, and you might end up costing yourself thousands in a poorly executed policy.

The correct design seeks to optimize the cash value accumulation feature of the policy and suppress the death benefit as much as possible. The correct circumstances to take advantage of indexed universal life insurance as a retirement vehicle are those with above-average incomes, who have the disposable income that allows them to place $10,000 into the policy annually (at the very least), and who has either fully used or at least fully understands the other options that exist for retirement planning.

How Much Income Can I Create with an IUL Policy?

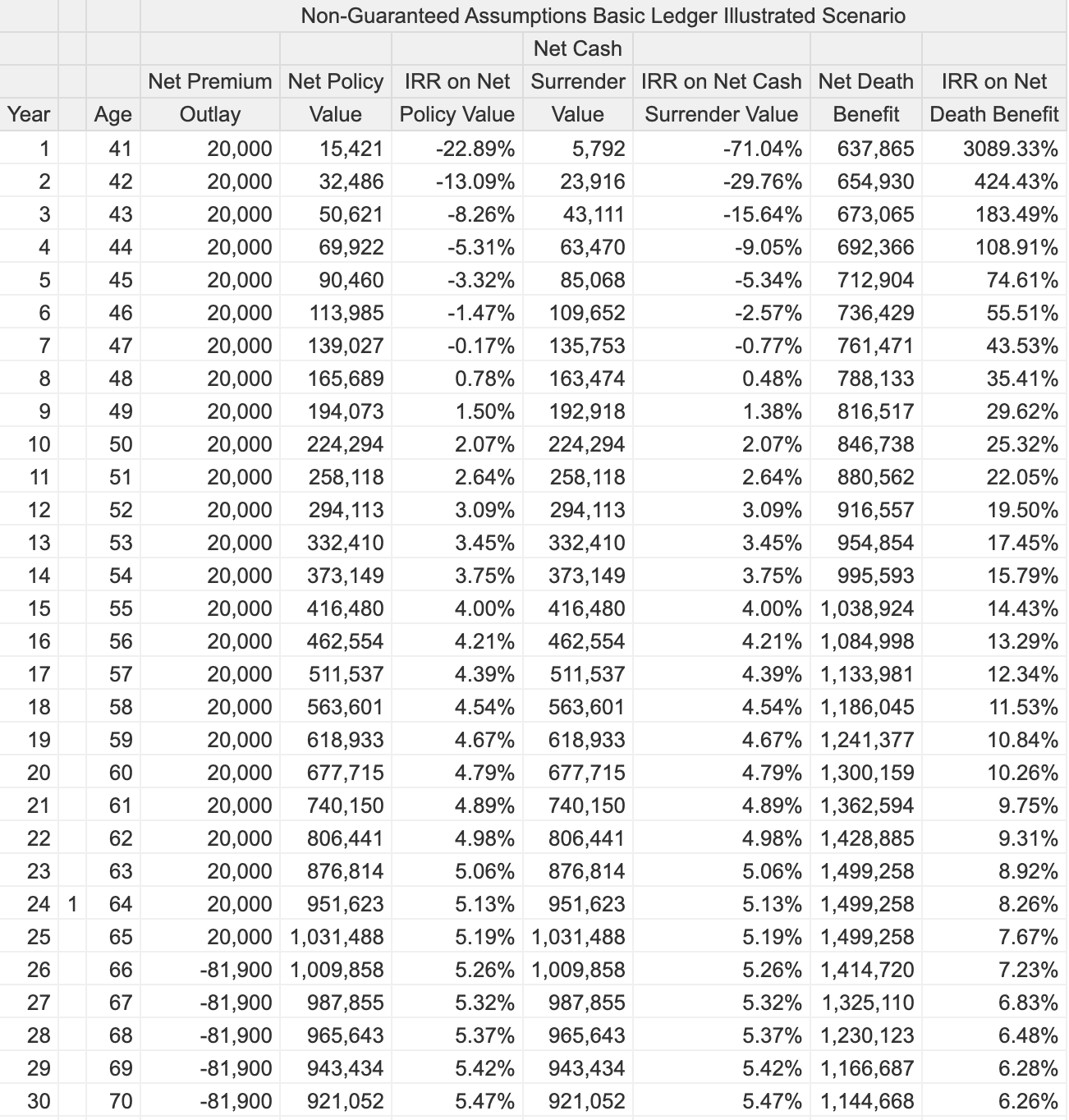

Here's an example of an indexed universal life insurance policy for a 40-year-old male who puts $20,000 per year into the policy until he retires at age 65. He then begins to use the policy to create income in retirement:

This ledger shows us that he can begin generating income in the amount of $81,900 at age 66. This income amount projects to his age 100 (not shown in the ledger).

The reported income is free of income tax liability and regardless of economic conditions, this policy-owner knows that he'll never have a year that the policy drops in value by some crazy amount like 20%. The worst he can do is actually 1% interest earned on his cash value (that's the minimum on this particular indexed universal life insurance policy).

As you can see from all of this, indexed universal life insurance is a pretty good tool for retirement planning. It complements other options (such as your 401k, IRA's, etc) very well. It provides an incredible degree of stability because it limits losses when markets turn negative. Lastly, it benefits from special tax treatment that significantly augments what you can ultimately achieve in terms of real buying power from the policy's cash value and/or death benefit.

any chance you can show the Guaranteed side of this ledger?

Hi Jerry,

I’m not sure I see the point in it. I think the blog post explicitly mentions that if you are looking for some sort of contractually guaranteed result, IUL is not the right fit.

Hey guys thanks as always for the balanced perspective. Is your 40 y/o male in above example “standard”?

Hey Thomas, thanks for the feedback.

The example here assumes preferred risk classification.

Brandon,

I see a lot of videos talk about how mortality cost will cause the IULs to lag severely in later years as one gets older. This is because IUL has an annual renewable term like chassis causing the cost of insurance to go up each year. Can you clarify this by illustrations? Everyone talks about this, but nobody seems to show any data behind this. In a whole life we do something similar by adding a term rider to enhance cash value, but the term rider portion goes down eventually as future dividends end up buying paid up additions. I assume this is not the case with IUL? Is there anything like a paid up portion in IUL?

I assume that the illustration shown has a certain average return assumption each year. As we all know average return is not the same as real returns as the sequence of returns can have an impact on what is being taken out as cost from cash value. Would appreciate if you can clarify the above points.

Hi Jay,

Here’s a blog post about IUL costs from a few years ago where we did pretty much what you are asking. You’ll see that long term the expenses of the policy comprise a small percentage of overall cash value, which is a very low hurdle to cross with the accumulation feature of the policy. For a lot of IUL policies, simply moving cash to the fixed account can remove the fear of losing money due to zero crediting years. We should perhaps update this discussion with a podcast episode.

This is the ultimate retirement vehicle because you can take advantage of Compound Interest and you have access to your money at anytime, tax free withdrawals, 0 floor which means Uninterrupted Compound interest, death benefit paid to your beneficiary and cash value too to pass on generational weath to your family, plus you can use the death benefit if you get cancer or other terminal illness. (Promotional content deleted). Best decision I have ever made!!!

My Universal Life policy of 20 years has just doubled my premiums numerous lawsuits starting all over US

Hi Louisa,

Sorry to hear that you are in this situation. Do you mind sharing with us what death benefit amount you have, how much you were paying in premiums up until the increase, and what age you were when you bought the policy?