Podcast: Play in new window | Download

Following up on my long established position that indexed universal life insurance is not market correlated, I want to share a story about a recent client situation involving IUL. As you all well know, the market experienced incredible volatility recently due to major attempts to mitigate the spread of Covid-19. This resulted in a massive contraction in market values back in March followed by an incredible resurgence in values through April and now into June.

For those who remained calm and didn't shift assets, the experience was one of reduced account values, followed by balances nearing their positions at the start of the pandemic. In other words, not much of a change. That's a great story for those fortunate enough no to move assets in the wake of all the CNBC Market in Crisis specials. But what about those who did worry and did sell to mitigate losses? I'm sure they are kicking themselves at the moment.

What also about those who face furloughs or outright job loss in the face of all this? What about the business owners who remain closed or effectively closed due to state regulations that significantly prohibit business as usual? What about those who had to dip into their savings to cover obligations?

The Double Whammy of a Market Retraction

The stock market is a leading indicator. It usually declines before we find ourselves smack dab in the middle of a recession. The insidiousness of this is the fact the people watch their account balances shrink and then receive their pink slip. This often forces people to take money from their already depressed investments–a forced sell off at the worst possible time.

We hear financial pontificators chide us all the time in market corrections. “Don't sell!” “This is the worst possible time to sell!” Stay invested!”

Great advice when you have the luxury of making that decision on your own. But if life makes that decision for you, you can't tell your boss that you're going to need him to delay your termination because you need the income for a while at least until your 401(k) rebounds.

So despite the well intentioned advice, withdrawing funds from an investment account may have little to do with fear of the market and everything to do with an emergency necessitating a cash infusion. The unfortunate consequences of such a reality is the sale of an asset while it's seriously depressed and this usually leads to forfeiting gain from the rebound in asset price once the panic subsides.

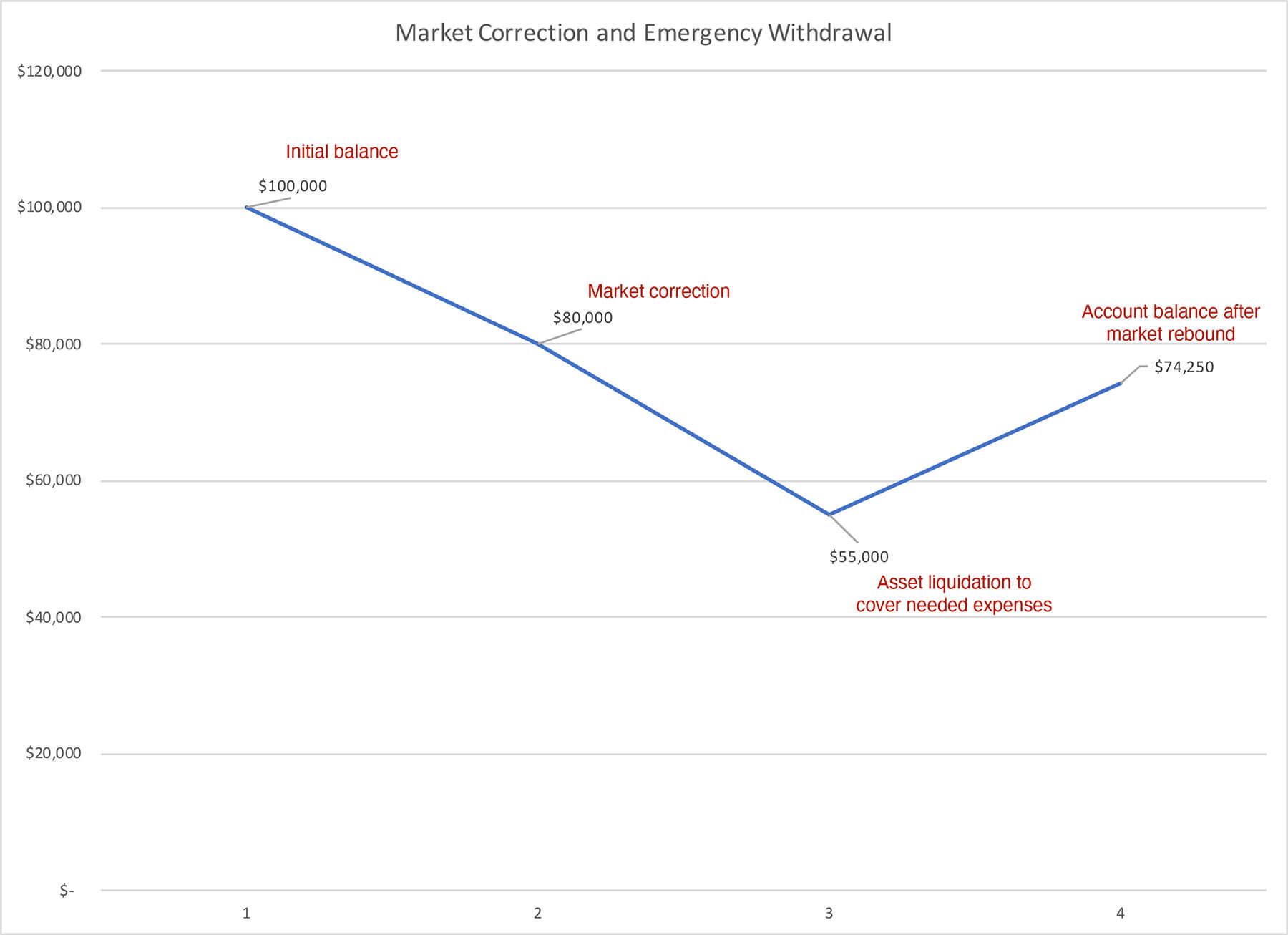

Here's a graphical depiction to help illustrate the impact:

In this scenario a 20% market correction draws down the initial investment account by $20,000. The investor then needs $25,000 in cash so he decides to liquidate a part of the account and sell $25,000 worth of stocks. The market then rebounds 35% and this leaves the investor with $74,250.

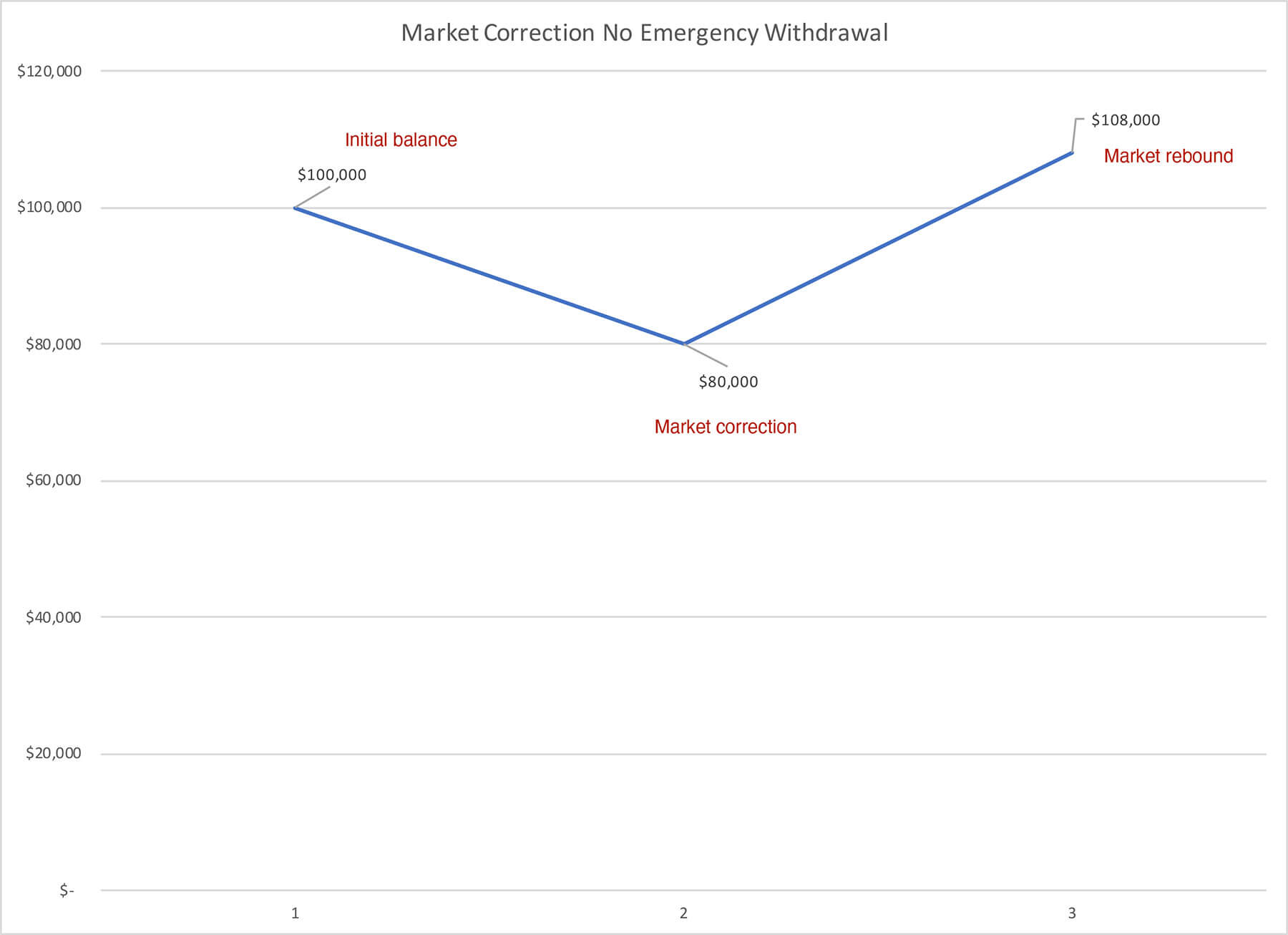

This isn't a terrible account balance after the correction, but let's see what happens if the liquidation wasn't required:

Here the market experiences the same 20% correction, which results in a $20,000 reduction in the account balance. But here the investor doesn't need to sell off $25,000 worth of stock and rides the 35% rebound with all stocks still intact. This results in a $108,000 balance after the rebound. So not taking the $25,000 out of the account increases the investor's account by $33,750.

It's easy to see from this why financial gurus are so adamant about staying the course and not selling in a correction. But as we already covered, sometimes that sale is forced by other necessities we don't control. If the mortgage is due, the bank isn't going to say, “don't worry about it, we want you to make sure you recover your losses first.”

Indexed Universal Life Insurance in a Market Correction

We recently had a client take a loan from an indexed universal life insurance policy that was necessitated by the market correction. I sensed a good amount of resistance. It felt as though he felt taking a loan at this time was wrong for some reason. I didn't believe that and was quite vocal about my thoughts, which were this is exactly why he owns life insurance.

I mentioned that taking the loan wasn't going to impact the index earnings, which given the market conditions were likely to be the guaranteed interest of 1%. Little did I know, things were going to recover rather quickly before his early June anniversary date. By the time his anniversary date came, and his one year S&P 500 index segment closed, his actual index earnings were capped out at a low double digit interest payment on his cash value.

So this means he took a $25,000 loan from his policy, this had zero impact on his cash value balance, and he then earned 10.5% on his entire cash value balance. The original Covid correction had no impact on his account balance because this is a fixed insurance product that is not invested in the market. There was no scary moment of sudden losses over the course of a few weeks and the recovery left him in a place better than he was a year ago.

He also opted to reduce his normally scheduled premium payment–completely permissible with indexed universal life insurance–by 75% due a cash flow problem that necessitated the loan. Truthfully, the premium payment was entirely unnecessary, but he wanted to make it.

He hasn't begun making any repayments to the life insurance policy loan and that's totally okay. The index earnings he just received far exceed the loan interest that will accumulate (it hasn't yet accumulated, so it might not if he chooses to pay down the balance) over the next 12 months.

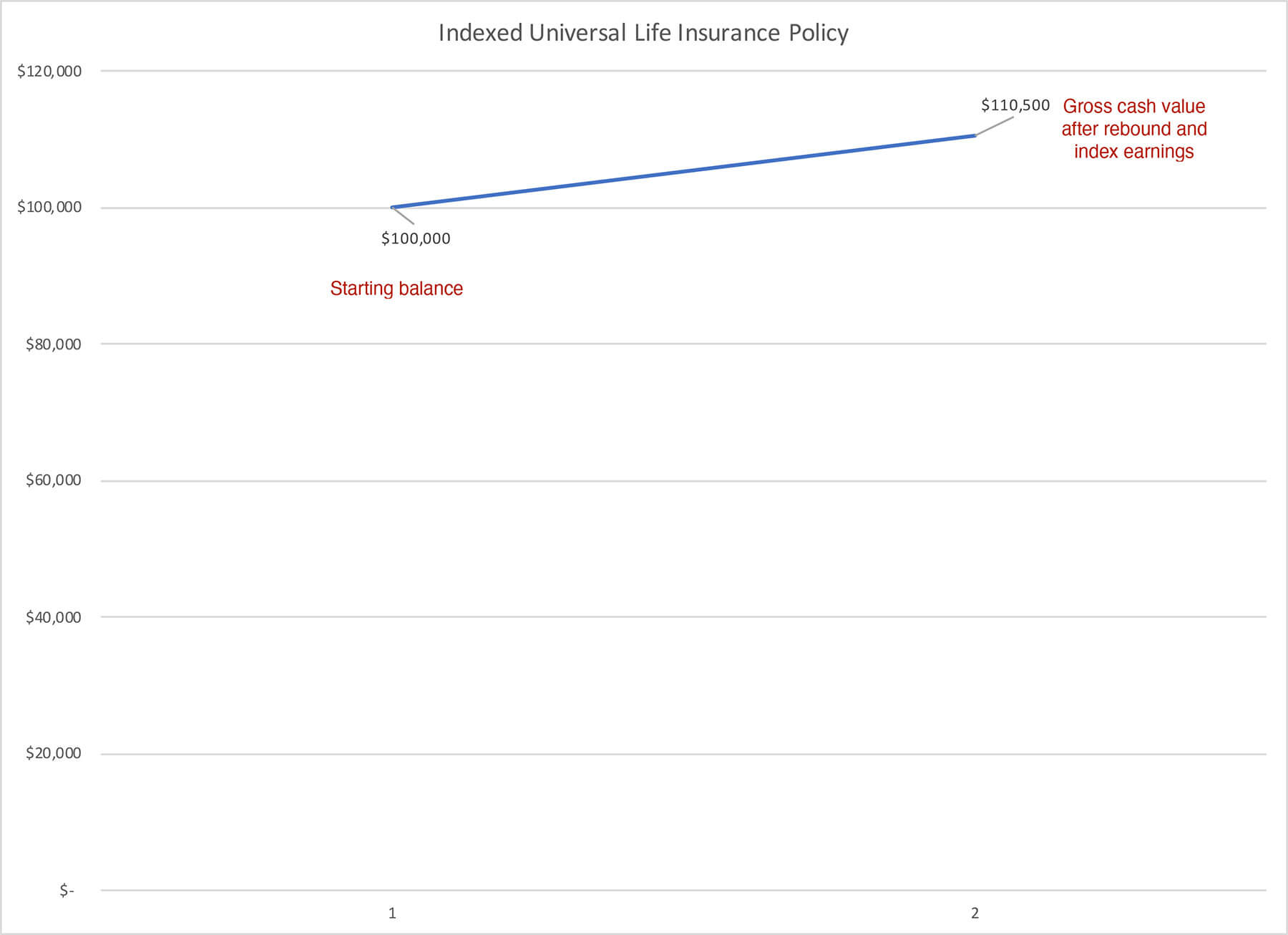

Using the above market investment examples, here's how indexed universal life insurance under similar circumstances behaves despite a loan of $25,000 being taken during the correction:

The result is a straight line because the market correction has no affect on the cash value. Even with the loan being taken, that too has no affect on the gross cash value balance. Only the index earnings cause a change in the cash value and that is a positive change.

Index Universal Life Insurance is Market Neutral

Years ago I original mentioned that IUL is market neutral. This means it is not correlated with the stock market. When we speak in terms of market correction, we mean that an asset moves to some degree with the moves in the overall stock market. Investors seek other investments that have low or no correlation with the stock market as a means to avoid losses when the stock market corrects.

I should take a brief pause and note that there is a distinct difference between assets that are not correlated and assets that are inversely correlated with the market.

An inverse correlation means that that asset moves in the opposite direction of the stock market. A short position is one of the best examples. Here the asset rises in value when the market falls in value. This is one way to mitigate losses (or even create gains) when the overall stock market declines in value. It is, however, very timing dependent and can result in significant losses if held too long. This is the case because the market does tend to increase over the long term.

A non correlated asset on the other hand is unaffected by movements in the stock market. The price of timber, for example, is usually unaffected by a rapid rise or fall in the stock market; therefore it is a non-correlated asset.

Whole life insurance enjoys a well established position as a non-correlated assets with the stock market. It has very stable cash value that increases by a guaranteed interest rate and dividends when applicable.

I contend that indexed universal life insurance enjoys the same benefits–though I realize others have disagreed at times. The contention is the market linked aspect of the indexing feature of IUL. Because the index account uses a market index of some sort, and because those indices are traditionally stock-based, many suggest that indexed universal life insurance is too much like the stock market to remove the risk of the market. I think the above example does a good job in pointing out the major flaw in that logic.

Bottom Line on IUL and Market Correlation

Indexed universal life insurance enjoys stable cash value with an interest rate based off the movement in an index. Often times this index is partly or entirely tracking a stock index, but the segmentation of indexed universal life insurance removes most if not all of the correlation the asset has with the overall stock market.

Indexed universal life has zero correlation to the stock market. The policies are fixed rate instruments. Interest is calculated through movements of indices but the caps are entirely controlled by the insurance company. With unilateral ability to control the caps the insurance company controls the cash values and the guarantees of the death benefit. Agents entirely misunderstand these policies and the impact the low interest rate environment will have on the caps. These policies and their risks have been oversold, and many policies will be underfunded and will lapse once the caps are reduced.