Podcast: Play in new window | Download

Industry chatter about indexed universal life insurance spans a wide spectrum of woohoo! and boohoo! Regardless of your position on the product, the one apparent consensus is: the product is on fire! Sales for indexed universal life insurance are up up UP! And if I end one more sentence with an exclamation, you'll probably want to murder me.

For years, we've seen industry reports and news coverage extolling the meteoric rise of indexed universal life insurance. The product appears to be the one bright spot in a sea of otherwise boring sales data stubbornly stuck on a flat growth curve. Don't believe me, check out these reports here, here, and here.

This, of course, makes for great marketing fluff when it comes to all the shiny brochures life insurers waste policyholder money on. It's an obviously glorious narrative. Come buy indexed universal life insurance! Why? Because everyone else appears to be doing it!

It's the one product that continues to impress with double digit growth in sales. With achievements such as this, it looks like the life insurance industry is booming into new markets and snapping up ever more customers. If only that were true…

Historical Growth Data: Indexed Universal Life Insurance

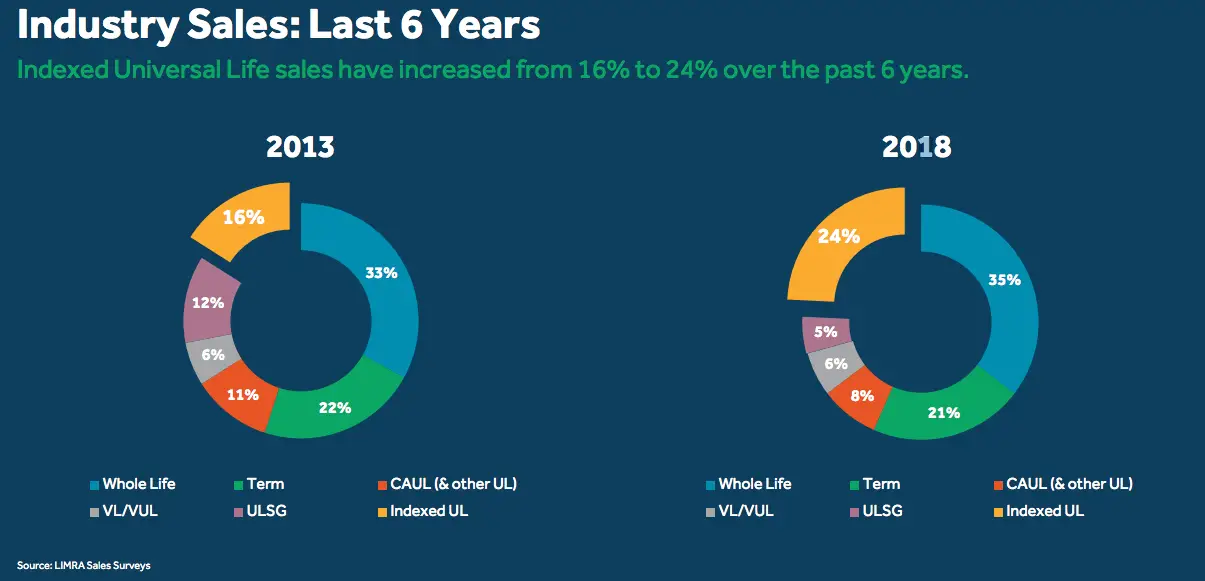

Here's an info graphic the Guardian put together with LIMRA data for a brochure it created about indexed universal life insurance:

The specific brochure I pulled this from wasn't seeking to promote indexed universal life insurance, quite the contrary. But here, Guardian wanted to note what others reported for the past several years. Sales of indexed universal life insurance are on the rise.

In 2013 IUL sales comprised only 16% of the overall individual life insurance marketplace. In 2018 that number grew to 24%. Impressive!

But pump the breaks for a second and take a second look at that infographic and tell me if you see what I see. Add up the all the number that represent universal life insurance sales for 2013 and then for 2018…I'll wait while you open your calculator app.

They are almost the same. In fact, they are slightly lower in 2018 than they were in 2013–43% versus 45%.

From 2013 to 2018 Variable Universal Life Insurance sales remained mostly the same. Notice, however, the drop in sales for ULSG (aka secondary guaranteed or simply guaranteed universal life insurance) and CAUL & Others (what we used to call “current assumption” universal life insurance).

Since the introduction and widespread adoption of indexed universal life insurance, many companies ditched current assumption universal life insurance. In addition, following the adoption of Actuarial Guideline 38, several companies scaled back their secondary guarantee universal life insurance, many in favor of indexed universal life insurance policies that incorporated a secondary guarantee of some sort.

When we back out a bit and view the data through a larger viewfinder, we see a story more about swapping one product for another than about gangbusters sales results of a hip new product offering.

The Universal Life Insurance Sales Trend Down Overall

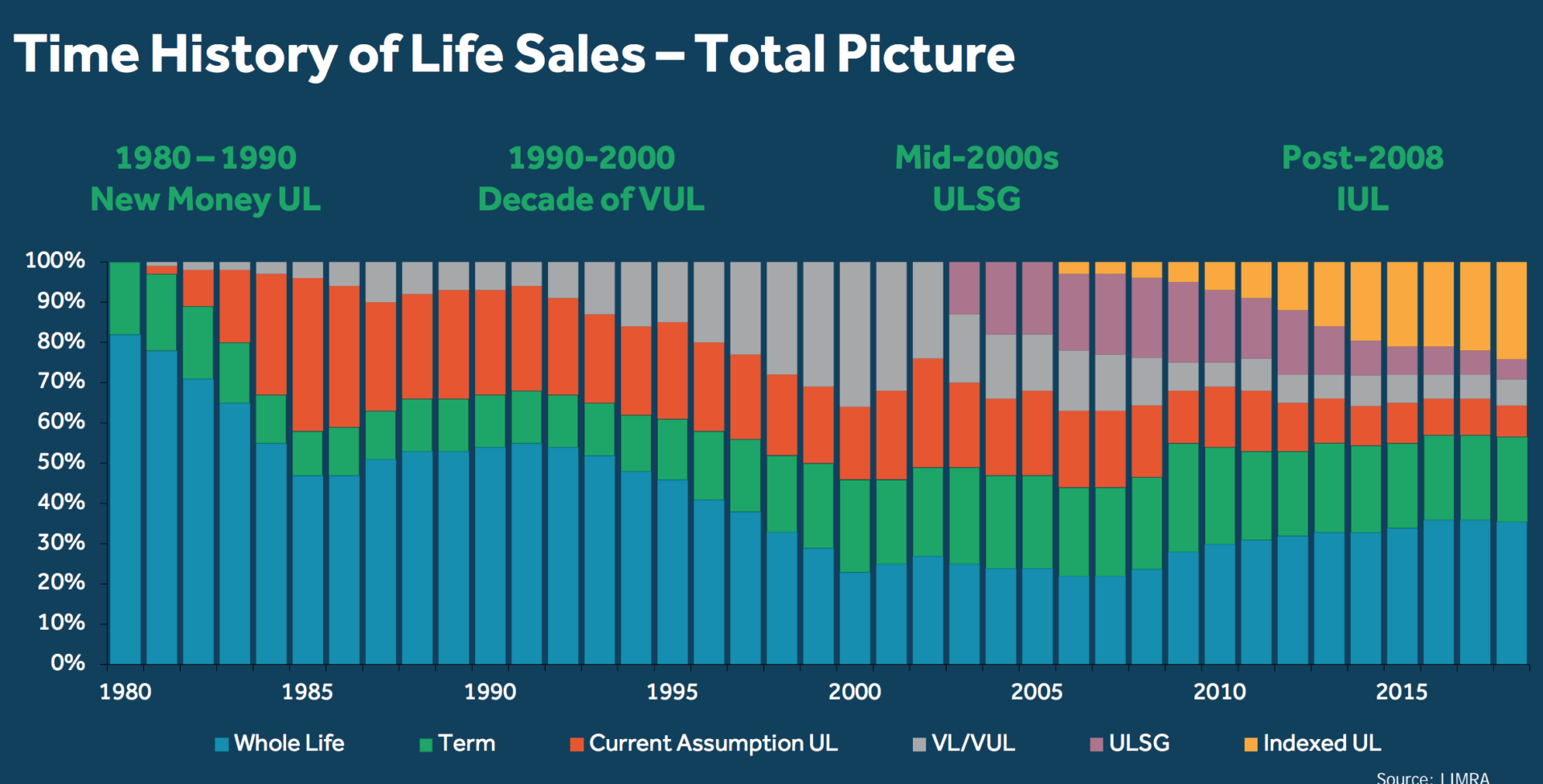

Here's another chart thanks to Guardian, again sourced from LIMRA data:

Here we see that, since inception, universal life insurance sales overall hit a peak around the early and again in the mid 2000's. But since then, the sales declined. We start to see indexed universal life insurance register in the mid 2000's and sure enough sales do rise rapidly. But with the growth of IUL sales comes a sharp fall in all other universal life insurance sales.

So Should you Buy Indexed Universal Life Insurance?

Potentially, but not because someone told you it's the fastest growing product in the life insurance industry right now. While that statement is technically correct, it's misleadingly applied to suggest people are pouring into the product.

Indexed universal life insurance has many virtues. It's taken a bit of a beating over the past few years do to rising options prices and lower interest rates, both of which place downward pressure on the indexing feature of the product.

But policy owners of indexed insurance products continue to benefit from the bull market and achieved interest payments in the past year that are the envy of any conservative investor.

Bottom Line

Yes indexed universal life insurance sales grew at a double digit pace over the the past 10 years, but there are two important factors that led to this.

First the product first appeared on scene not much more than 10 years ago, so growth from virtually nothing makes double digit year-over-year growth and easier accomplishment.

Second many life insurers discontinued other forms of universal life insurance and many insurance marketers shifted focus away from other forms of universal life insurance. The market place simply took its universal life insurance dollars and put them with indexed universal life insurance. In other words, universal life insurance sales were going to happen, and as other forms of universal life insurance disappeared, indexed universal life insurance captured those sales.

Indexed universal life insurance can stand on its own intrinsic merits. We shouldn't overlook them. Sales data on its own is a shaky reason anyone should buy a life insurance product. And this particular sales datapoint bends reality.

If there is a significant market correction and the downturn lasts for a decade (or more) without recovering to the previous high, why would I want to have purchased one or more IUL products before the crash? It’s all roses and sunshine during this bull market that started in 2009 but if things go the other way, what contractual guarantees in the IUL provide some ray of hope during a prolonged bear market? I cannot see how an IUL chassis will work out, when the markets are going down or sideways, as any growth will be absent or the bare minimum AND you still have the insurance costs to address. Interested in your thoughts.

Hi Todd,

In a scenario where we have prolonged market decline, the effect on IUL depends on the how the “function” of the decline. If we have an up and down market that averages more losses than gains the impact on IUL might not be as bad as we’d first assume. Up and down with an overall average of loss would be frustrating for an in the market investor, but IUL could benefit from the point-to-point aspect.

If, however, the movement is constantly down year-over-year this will certainly negatively impact IUL and frustrate most if not all IUL policyholders with a few possible exceptions.

1. The policyholder might opt to move to the fixed account. Some older fixed account IUL policies have pretty decent guaranteed minimum fixed account interest rates. If reality is a stock market that losses value every year, the 3-4% fixed interest might appear attractive.

2. Some indexed annuities introduced inverse market index options years ago, so we’d probably see insurance companies bring these options to life insurance policies as quickly as possible.

This all being said, a prolonged declining market, where each year is down from the last is not good for IUL. If you truly believed that is the direction of the stock market, IUL would be a bad choice for you.

I’m so glad you guys are back. I really missed your podcast!!!

Thanks Jamie, we’re glad to be back and thanks for sticking around in our absence!

Should I choose VUL over IUL since I’m 52 years old?

Hi Marissa, I wouldn’t say your age guides the decision between VUL and IUL.