Most of our readers and clients are familiar with the White Coat Investor—a web site started a few years ago by Jim Dahle, a physician who practices Emergency Medicine. I’ve talked about Jim’s work before, once quite a while ago when he attempted to malign whole life insurance and again about a year ago when readers wanted me to take on his suggestion that whole life insurance is not like a Roth IRA.

The second time I disappointed some people when I did the exact opposite of what they wanted by pointing out that he wasn’t wrong on that subject.

For the most part, we like to leave him alone in his pursuits. This is due in part to the fact that, believe it or not, we’re not all that different in our main goal—to identify and bring attention to the really dumb things financial professionals of all types do to people (for the White Coat Investor it’s specifically doctors) that leave them in a less than optimal position.

We differ, obviously, on our feelings about life insurance and that’s mostly fine. But Jim’s been on a bit of an indexed universal life insurance rant lately thus we’ve decided to weigh in on his recent work reviewing an indexed universal life insurance illustration that someone sent him.

How Indexed Universal Life Insurance Works

The first section of Jim’s review “explains” how indexed universal life insurance works. A lot of the mechanics are mostly correct but then immediately dives into a list of “problems” with these contracts.

None of which are real problems.

The product isn’t designed to yield as high as directly investing in the stock market largely because it doesn’t have nearly the risk profile that investing directly in stocks does. This doesn’t make one better than the other, it just makes them different.

Then there’s this statement, which cannot be paraphrased, read it start to finish and you’ll see why:

“Add in the cost of the insurance (not insubstantial if you’re older, sicker, or have dangerous habits like I do), the fess, and the commissions, and you’re looking at returns that are likely to be similar to a whole life policy, but could either outperform it or underperform it. That means, if you’re one of the 20% of people who actually hold on to the policy for the rest of your life, that you’re returns will be somewhere between the 2% guaranteed and the 5% projected returns.”

Did he just number dump us?

Well luckily we know enough not to be confused by the random throwing around of numbers..

Then Jim finishes off the section by noting that ”The big selling point of these policies is stock-market like returns without any downside risk.”

Wouldn’t there reasonably be some sort of tradeoff on return if we gave up the fact that we could also lose money?

Hold onto that though, we’ll come back to it.

Reviewing an Actual Illustration

Jim received an illustration for Midland National’s CV4 indexed universal life product. The policy assumes a very healthy male age 30 placing $5,500 into the policy each year. He notes that the guaranteed interest rate (on the fixed account, which he confuses) is 3%.

He then goes on to make this comment:

“note this guaranteed rate is much lower than the typical non-guaranteed 6-8% crediting rate on whole life policy.”

Did you just say Eleventy-five?

I’m not sure what the guaranteed rate on the fixed account of an indexed universal life insurance contract has to do with the non-guaranteed rate of a whole life insurance contract, but apparently it means life insurance is bad? Or something like that.

The Guaranteed Ledger

The discussion on the guaranteed numbers starts by noting that: ”People buy IUL’s for the guarantees.”

Really?

I’ve been in the insurance and financial services industry quite a bit longer than Dr. Dahle has been blogging about it and I’ve also written a lot more indexed universal life insurance contracts than he has (see what I did there?) and no one who has bought one gushed about the guarantees.

Not surprisingly, the guarantees aren’t awe-inspiring. Now, they are infinitely better than the guarantees on an equity mutual fund with…well…anyone but let’s not get details like that get in our way.

There’s a comment about the whole “you can’t lose money” claim that some agents make regarding indexed products that is taken very much out of context. Since the products starts out with a pretty low amount of cash surrender value (not cash value, but cash surrender value, there’s an important difference there) there’s an obvious loss that could be recognized if one were to cash out of the policy.

Similar to the loss one could realize if they bought into practically any S&P 500 indexed fund in early 2008 and then sold. What’s the actual loss in terms of cash value? About 12.73% according to the Midland proposal.

The Assumed Ledger

The assumed ledger takes one two forms. A 4% assumed crediting rate and an 8.6% (the default rate) assumed crediting rate. The 4% midpoint scenario offers an interesting insight, but before we go there, lets first jump to the ledger everyone is really interested in, the defaulted assumed rate.

At 8.6% assumed index crediting the internal rate of return on the policy (that’s the annual interest rate equivalent you’d have to earn on the premiums paid to achieve the same cash surrender value) is 7.98%. Not too bad, even Jim agrees.

But he does present this information with the caveat that this is highly dependent on what the crediting rate ends up being. Which means the overall return is entirely dependent on how things work out. Making it different from all other savings or investment plans how? I’m not entirely sure.

But there’s a problem, you see.

This 7.98% internal rate of return is still under 8%. Most of the intelligent crowd will ask ”so what?” and I’m very much with you, but apparently this is a problem. Dr. Dahle then points out that this is way behind the ”long-term” internal rate of return of the Vanguard 500 Index Fund, which comes out to 11.05%!

He even was nice enough to calculate the difference in total money we’d have between that 7.98% and 11.05% return. IF you invested $100,000 over the course of 25 years it’s $682,000 vs. $1.37 million.

That’s like, twice as much. Amazing! Lets everyone stop what you’re doing and start filling out Vanguard paperwork.

Not so Fast

If all of that information caused you to raise a suspicious eyebrow, congratulations you’ve obtained the skill of detecting BS.

11.05% is, I assure you, the “since inception” internal rate of return for the Vanguard 500 Index Fund—it says so right on their website.

But that time frame spans from the mid 1970’s to present. That’s a tad longer than the 25-year period we were talking about earlier. But what’s 12 years give or take among friends?

Also, that’s the internal rate of return assuming you were all in at year one. Remember that time we wrote that piece that explained how there’s a difference between lump sum investing and systematic investing?

So what happens if we take the annualized returns from a 25-year period (1989 to 2013) and calculate the internal rate of return on a $5,500 per year investment in the Vanguard 500 Index Fund? We end up with $317,249.39. That’s an internal rate of return of 5.95%

Wait a minute. That’s less than the indexed universal life insurance policy, and just like the late Billy Mays used to say, “But wait…there’s more!”

That 5.95% return over that time period ignores the fees you would have paid Vanguard. And since, contrary to the belief held by some, they don’t invest your money for free we have to internalize the fees Vanguard would have collected.

So if we go back and add the quite impressive 0.17% management fee they currently assess in all years, our net cash comes out to $308,543.50 or 5.76% per year rate of return. And since we always look at insurance contracts fees included, it’s only fair to include them for the mutual fund in this case as well.

So a real apples-to-apples comparison over the same time period tells us quite a different story.

Hey, remember that 4% midpoint?

The Midpoint

The 25-year internal rate of return for the 4% midpoint comes out to 3.41%.

But these things don’t work in a vacuum. If the average credited interest rate were cut down 54% than we’d have to also assume that our return on the market was going to decrease by a similar amount.

The insurance industry isn't blind to competitiveness. In fact, it's fierce interest in competitiveness is a major reason universal life insurance exists in the first place–those old whole life products were oh so profitable and oh so lagging behind in terms of performance.

If we took market performance and cut it in half, it too would be in the same territory.

What can I expect my Yield to be?

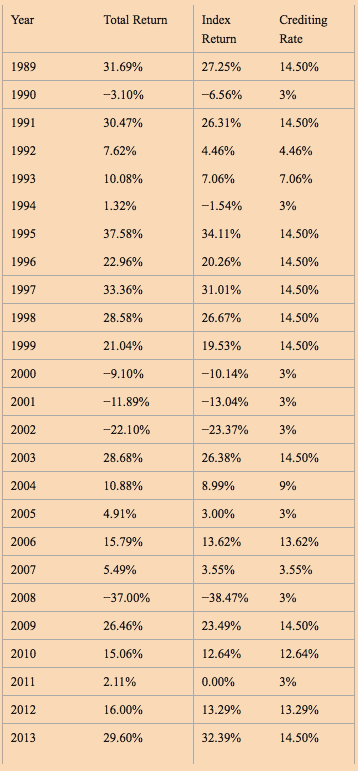

Jim attempts to answer this question with a historical table that compares Midland’s index crediting strategy for its one year point-to-point on the S&P 500 index to the S&P 500 itself and a Total Return Fund.

He makes a mistake concerning Midland by stating that the product has a 3% annual floor to the indexing strategy. This is not correct.

The floor is zero. This brings him to an incorrect conclusion about the average credited interest rate that would have happened for the past 25 years. He calculates it at 9.17%, but once we correct his mistake the correct average would be 8.46%. If we rerun the Midland illustration assuming this 8.46%, the 25 year compound annual growth rate on cash is 7.84%–for those keeping score.

Here’s a copy of the table:

That point aside, Jim points out to his readers that the average return that can be calculated from these tables for the indexed universal life insurance isn’t the same as the internal rate of return or compound annual growth rate (they are the same thing) as the average rate of return calculated from these tables.

Normally, I wouldn’t really care about this comment, but there’s a sort of suggestion that this is a unique draw back to indexed universal life insurance, which isn’t true.

If we calculated the average return from the other two options—a total return fund, and the index itself—we find that their average returns are substantially higher than the true compound annual growth rate that would be achieved if someone actually invested in the market.

So again, the suggested draw back to life insurance is exactly the same with all other options we have available for saving our money somewhere.

The index itself has a 17.58% average return but the compound annual growth rate on the same $5,500 per year comes out to 6.82% while the average return on the total return fund is 18.98% with a compound annual growth rate on the same $5,500 of 8.60%. These numbers completely ignore fees (see above on why this might be important).

The reason for the spread between the arithmetic and geometric means is due to variation. Indexed universal life insurance is way less volatile, and if this alone doesn't satisfy your need for proof in the difference in volatility, I’ll give you the calculated standard deviation for each data set:

- Total Return Fund: 11.49%

- S&P 500 Index: 11%

- Indexed Universal Life Insurance Policy: 6.47%

Let me quantify something for everyone. The indexed universal life insurance yielded nearly 15% better than the S&P 500 index itself for the past 25 years in our hypothetical example with 41% less variation.

The total return fund does bring more money to the table over the last 25 years in our hypothetical example. About 9% more money, meaning if the indexed universal life policy generated $100,000 the total return fund would bring $109,000 to the table.

But does it with 78% more volatility than the indexed universal life policy.

So using capital letters to point out that the average credited interest rate (which is nothing more than the average interest rate) isn’t the same as your return doesn’t make indexed universal life insurance any different from any other place you could store your money where the yield can change each year. But the actual return does tend to be way closer to the average return with indexed universal life insurance than is the case with typical stock market savings.

Yield isn’t the Only Consideration

There’s something more relevant to this discussion than merely yield. There are a multitude of benefits to life insurance when leveraged as an asset class, like the tax free status of growth and potential tax free distribution, the death benefit, the liquidity that comes along with being able to access cash at any time for any reason, and the risk adjusted rate of return that is far superior to any other option I’m aware of—to name a few of those benefits.

Let’s talk about income for a minute–since saving for the future is more about what you can do with your money than simply how much of it you happen to have.

If I go back and solve for max income on this proposal using the fixed loan option on this policy (fixed meaning the loan interest rate and the credited interest rate on the cash that backs the loan used to generate income is guaranteed to be the same, this is a contractual benefit to Midland) from age 55 to 100, the result is just under $35,827 (I’m rounding the cents up to the nearest dollar).

Remember that total return fund that outperformed the indexed universal life policy? This income stream represents 7.5% of the balance of that option from the income commencement date. Far, far higher than would be reasonable for most equity backed investment options—unless you are Dave Ramsey–and given the young age at which income begins, the probability of a more volatile savings plan's failure is increased significantly.

This happens because, again, the indexed universal life policy is far less volatile.

It’s going to continue to earn the indexed return and there is significant safety of principal. This is what agents and brokers are mostly concerned with when we talk about not being able to lose money. The policy doesn’t roll backwards when the market drops 25%. And as longer time readers know, declines in the market early on in one’s retirement years can have substantially negative impacts on your longevity risk—not something indexed universal life insurance policy holders worry about.

So what if we took that higher yield from the total return fund and placed it into something like an annuity in an attempt to augment income?

Best case scenario is a single life calculation (meaning if you die a year later the insurance company keeps your money) comes out to $26,952 or about $9,000 less. If one wanted to ensure that an early death at least kept their money in the hand of their loved ones the income comes out to $25,584, or a little over $10,000 less per year—if you made it to age 100, that’s $450,000 you gave up.

And what if we wanted to save more than $5,500 per year? That's a convenient number since it's within IRA limits.

But for those with more money on hand, and a five or six figure savings rate, life insurance becomes a lot more useful and helpful when it comes to deferring taxes on savings.

But what about the Fees?

Jim’s review doesn’t shy away from an old anti-insurance argument, fees. He takes numerous shots at insurance contracts regarding fees and commissions paid to agents and brokers.

I'm not really sure why making money is evil, since the profit motive is a key force behind market economics–a system that has put a lot of money in his pocket–but those silly details are inconvenient when you're trying to make a point I guess.

While commenting on the lack of cash surrender value in the first year of the policy he states:

“That’s pretty typical of life insurance. That money is paying for insurance but mostly going to the agent who sold it you as the commission.”

At the highest regular payout Midland National offers to an agent, they would pay $1414.49 for selling this policy or 25.72% of the initial premium. His suggestion that the 75.6% loss in year one comes mostly from commissions is simply false, and further, that loss didn't actually take place.

What Dr. Dahle failed to disclose was that the policy actually had between nearly $4,800 and $5,100 (depending on if we’re looking at guaranteed or projected values respectively) in gross cash value. This is the total amount of cash in the policy—the amount of which the credited interest rate is based—and is your money, but subject to a surrender charge if you cancel the policy within a certain period of time.

Life insurance isn’t a product that can be applied universally (just like all other financial vehicles) so we can’t look at one and declare it bad just because it doesn’t fit someone's circumstance.

If someone wanted immediate liquidity, I can design an indexed universal life insurance policy that has an immediate gain. Assuming the same parameters in Jim’s example, I can design a policy that has $5,600 after year one. It comes with a decrease in longer term performance (i.e. the Midland policy Jim used would have a higher compound annual growth rate by year 25 and on) but if first year liquidity is super important, then this can be done—oh and I still make a commission, a very comparable one to the Midland policy in this example).

But I have one more thing to point out as it relates to fees.

There are those who like to suggest that universal life insurance expenses (cost of insurance) rise dramatically as the insured ages.

Looking at this policy and assuming the income scenario, the fees in the policy remain pretty consistently at 0.4% of the cash value in the policy. That’s about double the 0.17% asset management fee that Vanguard assesses, but Vanguard doesn’t pay a death benefit when the policy owner dies, nor does Vanguard allow the policy-owner to maintain a pretty decent likelihood of a double digit return in any given year while providing significant safety of principal.

0.4% of assets is far better than the averaged managed mutual fund and even rivals some passive/indexed funds. The additional benefits that are available with the life insurance contract make that 0.4% seem pretty competitive.

Mistake or Misleading?

I don’t really think that Jim Dahle is intentionally trying to mislead his readers, largely because I'm not aware of any reason for him to do such a thing. His conclusions are wonky because he did the analysis wrong. He's a full time physician and a part time financial hobbyist. And that's okay.

In truth, I applaud him for trying to take an active role in helping people, but I do wish he’d tone down the absolutism regarding various financial products.

The insurance industry isn’t evil, and it’s not trying to swindle you of your hard earned money. We work with a lot of people all across the country and a number of them are physicians and other sophisticated, well-educated, and successful individuals.

We have an unheard of 0% five year lapse rate, meaning no one cancels the contracts they buy from us. We can’t pull the wool over that many people’s eyes for that long so the merits of the products speak for themselves.

People who understand what these products bring to the table, love what they accomplish. But just like any product, life insurance can be used for good or evil. Bad people do bad things in every industry–life insurance, investments and medicine included.

I’m going to pat myself on the back as I too thought the historical yield comparison was wrong mostly because of what you detailed here.

Thank you for being a source of knowledge to novices like myself!

You’re welcome, thanks for reading.

I bought one of these Midland products about eight years ago. I’ve averaged almost 9.2% credited per year. And I place A LOT more than $5500 into it.

Awesome how that works, isn’t it?

Brandon,

This is one of your best posts!

As a consumer, I am constantly amazed at the main stream media and internet bloggers outright “hate” for insurance products, or at minimum, grudging acknowledgement that it works for a small number of specific circumstances.

I wonder if they heard some horror stories of how some people were sold the products, then extrapolated that to everyone. It’s as if you heard stories of brokers and advisers who steered people into various mutual funds or non-traded REITs which blew up, and then passed judgment on all brokers and advisers based on those incidents.

But I think the issue is probably in the lack of education regarding the role(s) that life insurance (in all its form – term, permanent) plays in the context of a person’s financial plans.

It takes more specialized knowledge that you and Brantly have on this blog to educate people that buying a 20-25 year term policy when you’re 30, and not ever needing any other insurance products ever…assumes the optimistic scenarios come to pass: kids are out of college and got jobs, your external savings and investment plan worked, you got a nice series of good returns at critical times (right before/after you retire), you didn’t have financial setbacks or loss of a job, you paid off your mortgage and you didn’t suffer any degradation in your health.

At its most basic, insurance products are a transfer of risks: mortality, longevity, volatility, sequence of returns, interest rate, inflation, disability, etc.

Since I don’t know the future and also since I know myself (a big scaredy cat whether the stock market has gone up 100% or when it has gone down 25%), I will gladly give the insurers more money and trade some upside to get low volatility tax free compounded growth that just happens to pay my beneficiaries a large sum of money when I expire.

Thanks!

Thanks! I’ve commented before that it takes a little effort to understand this stuff, but it’s worth the effort. Because there is a benefit there for sure.

My daughter, a gastroenterologist, pointed this site out to me a year ago (I’ve been in private practice as a dermatologist for 20 years).

She knows that I’ve owned several life insurance policies and was contemplating another (an indexed equity universal life insurance policy from a different company than the one mentioned here).

I’m pretty new to these indexed products, but I’ve owned whole life insurance for a long time, and I’ve been pretty happy with the results.

She likes to think that maybe she can do better than dear old dad with the stock market, and I keep reminding her that slow and steady wins the race. My investments (and I own quite a bit of them) have certainly been up and down over the years, but my life insurance has always brought a lot of peace of mind.

Listen to dear old dad 😉

Glad to hear the whole life policies have worked out well.