Podcast: Play in new window | Download

We like life insurance because it marches to its own beat. In other words, when CNBC is reporting panic over Facebook, life insurance carries on almost as if its never even heard of Mark Zuckerberg. A majority of our clients adopt a similar view on life insurance.

Life insurance serves as a wonderful complement to a portfolio of stocks and various other securities largely because it's not inextricably tied to performance underpinning those other assets.

It might make sense to assume, therefore, that indexed universal life insurance plays a different role. It is, after all, tied to the stock market so it should follow that such a life insurance product is too tightly associated with stock market movements to serve any useful purpose of diversifying economic exposures. This sounds plausible in the most elementary sense of the understanding. It is, I'm afraid, however, dreadfully wrong.

Market Neutral and Non-Correlated Assets

While some of the more technical among us might argue my casual association between market neutrality and “non-correlated assets” is a confusion of two unique concepts, I beg that you allow me the leeway to group them together for the time being. I promise there's a point to doing this and that we will arrive at this point by the time I'm done today.

Lets first ensure that everyone is working with the same definitions moving forward as I use these terms.

Market Neutral

Market neutral generally concerns an investment strategy that seeks to lessen the extremes of owning any asset where the risk of loss presents itself. Think of it in terms of giving up a certain amount of likely gain in order to shield yourself from a certain amount of potential damage. If you are comfortable with some more technical investment jargon, it's commonly a practice of taking a long and short position on an asset. If you don't know what that means, just understand that you stand to gain from both appreciation and decline of the asset's value.

For an investment strategy to be neutral, it must satisfy two requirements.

- It must benefit from both an increase and decrease in the asset value

- It must (at least theoretically) remove (or reduce) the risk of loss from owning the position in the asset

Non-Correlated Asset

A non-correlated asset is merely an asset that is not correlated to the stock market. In other words, an asset that does not move with the movement of the overall stock market.

Indexed Universal Life Insurance Market Neutral and Non-Correlated

Indexed universal life insurance is a form of cash value life insurance that earns an interest rate on cash values derived by the movement in an index over a specified period of time. Usually, the index is a stock index. I don't have exact data on how often a stock index is chosen over other indices, but I would estimate well over 95% of the time.

Given the ubiquity of stock market indices chosen for indexed universal life insurance, it makes sense to assume that this product would closely mimic overall stock market results. But a closer review of the precise functionality of this product tells a different story.

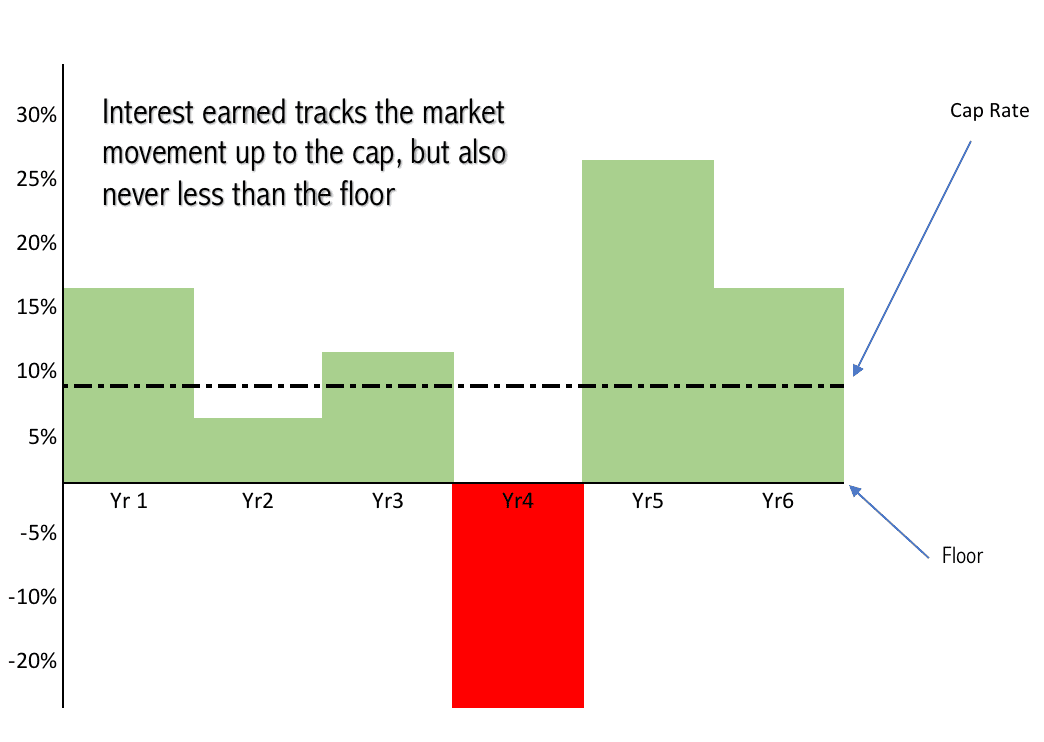

Caps and Floors

The most common index chosen for indexed universal life insurance is the S&P 500 and the most common time frame is one year. This means the interest rate paid on cash values will be the calculated percentage change of the index over a one year period. These products use a cap or an absolute maximum interest rate and a floor or an absolute minimum interest rate. Caps and floors vary, but on average caps are around 10% and floors 0%. This means the interest rate will not exceed 10% but will also never be negative.

Some index universal life insurance products also make an additional adjustment to the interest rate. We refer to this feature as a participation rate. This feature of indexed universal life insurance is more specialized and typically not a factor in the average policy that chooses a one-year S&P 500 indexing option.

Some index universal life insurance products also make an additional adjustment to the interest rate. We refer to this feature as a participation rate. This feature of indexed universal life insurance is more specialized and typically not a factor in the average policy that chooses a one-year S&P 500 indexing option.

The caps, floors, and periodization of indexed universal life insurance introduce very unique–and important–attributes to this product. And I'll argue that these features are the very reason why this product is both market neutral and non-correlated to the stock market.

Stacking the Gains on Top of the Losses

The fact that indexed universal life insurance benefits from upward movement in the stock market to lead some to assume a correlation between the product and overall market. But this relationship ends at this point (i.e., is moves upward when the market “moves” upward).

When the market declines, indexed universal life insurance stays put. The interest rate is zero or a minimal amount, but never a corresponding reduction of cash values that mimics the losses a true investor might realize in a declining market. And then, like the end of a bad day, the end of a bad year comes and goes beginning a new year where the prospects for gains start from a vantage point far higher than a true investor who road the market down in the prior year. This places the indexed universal life holder in an advantageous position to ring in new gains for the year, unlike the true investor who might spend the next 12 months merely regaining lost ground.

The Gravity of Averages

Most of us are pretty comfortable with the concept of an average. It's a central value of multiple results seeking to answer what usually happens with a set of data. But have you ever given any thought to what exactly the average means (slight pun intended)? Or what its implication is concerning anticipated results from subsequent events in our life?

If it's usually rainy in April, does that mean it will definitely be rainy in April? No. If this April is unusually dry, does that mean next April will be unusually wet? Probably not. But if this April does happen to be unusually dry, I'll bet next April will appear obnoxiously rainy if only next April is simply average concerning rainfall. The inverse of this is also true. It would also be exceptionally rare if we had two extremely dry Aprils in a row, again the inverse is also true.

What the hell does any of this have to do with the stock market or indexed universal life insurance? Averages matter. They matter because data points (in this case sequential events) tend to localize around a calculated mean. This is why we don't generally see years where the market is up 62% nor do we tend to see years where the market is down 30%. Instead, we see something more closely to the market is up 12% or down 5%. We also don't often see market returns or losses in a given year being exceedingly high or exceedingly negative for a period longer than one year.

When losses (especially big losses) do occur, they tend to precede big annual gains. These gains rarely recover all of the loss in a single year, but they can be quite substantial.

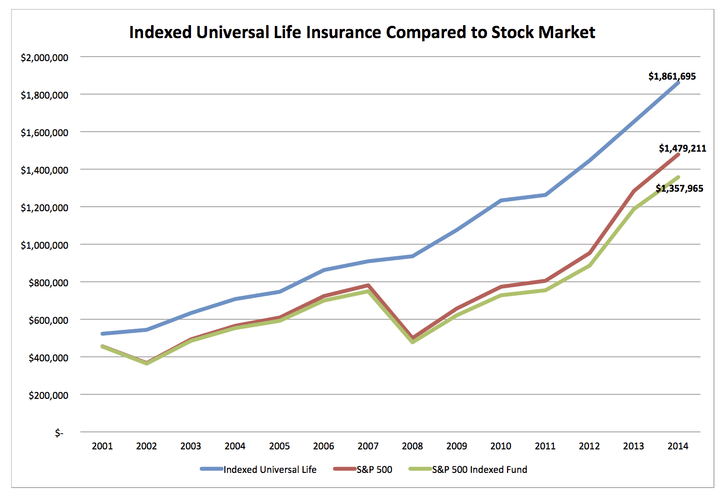

Indexed universal life insurance doesn't participate in the loss, but it does benefit from the gain. This allows indexed universal life insurance policyholders to pause in the bad years, and then pick right back up where they left off beginning the following year. This segmentation of how indexed universal life insurance policyholders realize gains make for a very special opportunity to stack gains on top of losses. This ultimately makes the product behave wildly different than a direct investment in the stock market.

Multi-Year Strategy Removing some Sequence of Returns Associated Risk

We've discussed the sequence of returns risk before. Put simply, is the notion that you cannot control the timing of a market decline and there are times when a decline is more or less favorable to you. The timing of declines can have a greater impact on your financial health and overall ability to accomplish various goals.

Index universal life insurance does not eliminate, but it significantly reduces the impact of the sequence of returns risk because it is less affected by years of market declines. This places it in a very special class of assets that one can use to accumulate wealth while being less concerned about how to preserve an asset base. And this, I present to you, is the key functionality that makes indexed universal life insurance market neutral and non-correlated.

Yes, I realize we're stepping outside of the boundaries of traditional consideration for market neutral assets. But it's this line of thinking we need to look beyond what everyone else stares at and gets wrong. This level of understanding unleashes options because it strategizes based on multi-decade planning rather than short-term worries over how you fared relative to the stock market in a given year.

Indexed universal life insurance can benefit from both market gains and market declines. It can remove a significant degree of ordinary market risk. AND it can greatly diminish probably the greatest risk we all face when it comes to wealth accumulation and retirement planning. It affords the luxury of allowing policyholders access to a degree of potential returns reserved only to the exceptionally wealthy or extremely insane. As a result, indexed universal life insurance is not at all like owning stocks in the actual stock market and can serve as a wonderful complement to anyone who does own such securities.

Unfortunately this misses the biggest point. What is actually being done behind the curtain? What are the hedging strategies and how transparent are they? If this could be accomplished with even relative certainty why would every hedge fund be incorporating this strategy and be wildly successful? Why did so many annuity companies with similar type guarantees go out of business or stop selling the products are 2008? What is the track record other than linear mathematical back testing?

Hi Bob,

Feel free to edit and resubmit this comment in a more coherent manner, and we’d be happy to discuss with you.

Hi Brandon,

I love the articles, podcasts, and site overall. I have a more specific question about IUL. I was told by my friend who’s an agent, and given an illustration, about a Voya Global Choice IUL with a index option that’s uncapped, 2yr, and takes 75%/25%/0% of the best two of the three indices of S&P500, Hang Seng, and Euro Stoxx. It’s at 65% of that weighted value, if I got the details right based on the illustration. Looks like this can potentially deliver some amazing returns when the markets are up, but I looked into Voya’s ratings and company and they don’t look as strong as other companies. What are your thoughts on this IUL with their unique 2yr index option, as well as the longevity of this product/company and the likelihood that this account won’t get “nerf’ed” down the line?

Thanks!

Endless Summer

Hi Endless Summer,

Sorry for the delay on this comment. It ended up in a weird place in our comment manager.

I understand the hesitation over Voya’s financials and we certainly don’t love this fact. I will say that they still maintain a reasonable and acceptable result at the company year over year.

I don’t personally like multi-year index options because I believe they are designed to look really appealing while insurers have crunched ample data to know that they rarely produce the results they purport.

I can’t speak personally to Voya’s management of policies and commitment to non-guaranteed aspects of the policy as we’ve never written business with them and do not presently manage any policies issued by them.

I’ve looked at Voya’s products in the past and I don’t find this one to be particularly better than past iterations. I also don’t find it to be superior to several other options available from other companies with strong balance sheets.