Podcast: Play in new window | Download

Whole life insurance can come across a little intimidating at first. The insurance industry has a bunch of specialized lingo and this isn't always super clear to normal people who don't work with life insurance every day. That said, with a little patience, and this article, you will be capable of reading and understanding your whole life insurance statement.

Per insurance law, life insurers must provide policyholders with an annual accounting of their policy once per year. This must arrive in the policy owner's hands within a certain timeframe around the policy anniversary date (normally 30 days before or after).

Whole life statements normally include information about the following five items:

- Death Benefit

- Cash Value

- Premiums

- Loans

- Dividends (if the policy is dividend-paying)

Whole Life Death Benefit

Death benefit information in a whole life insurance statement often includes several values. These can include:

- The base whole life death benefit

- Any death benefit provided by a term rider

- The death benefit from paid-up additions

The base whole life death benefit is the original death benefit from the whole life policy. It excludes any riders and death benefit from paid-up additions. This death benefit amount will not change over time; it is the original guaranteed death benefit of the policy.

Term rider death benefit is any death benefit on the policy created by the addition of a rider that adds death benefit to the whole life policy. These riders can take several different shapes depending on the insurance company. This rider is also the basis of whole life “blending.”

Paid-up additions death benefit is death benefit created either by the elective paid-up additions rider or the dividend option to purchase paid-up additions.

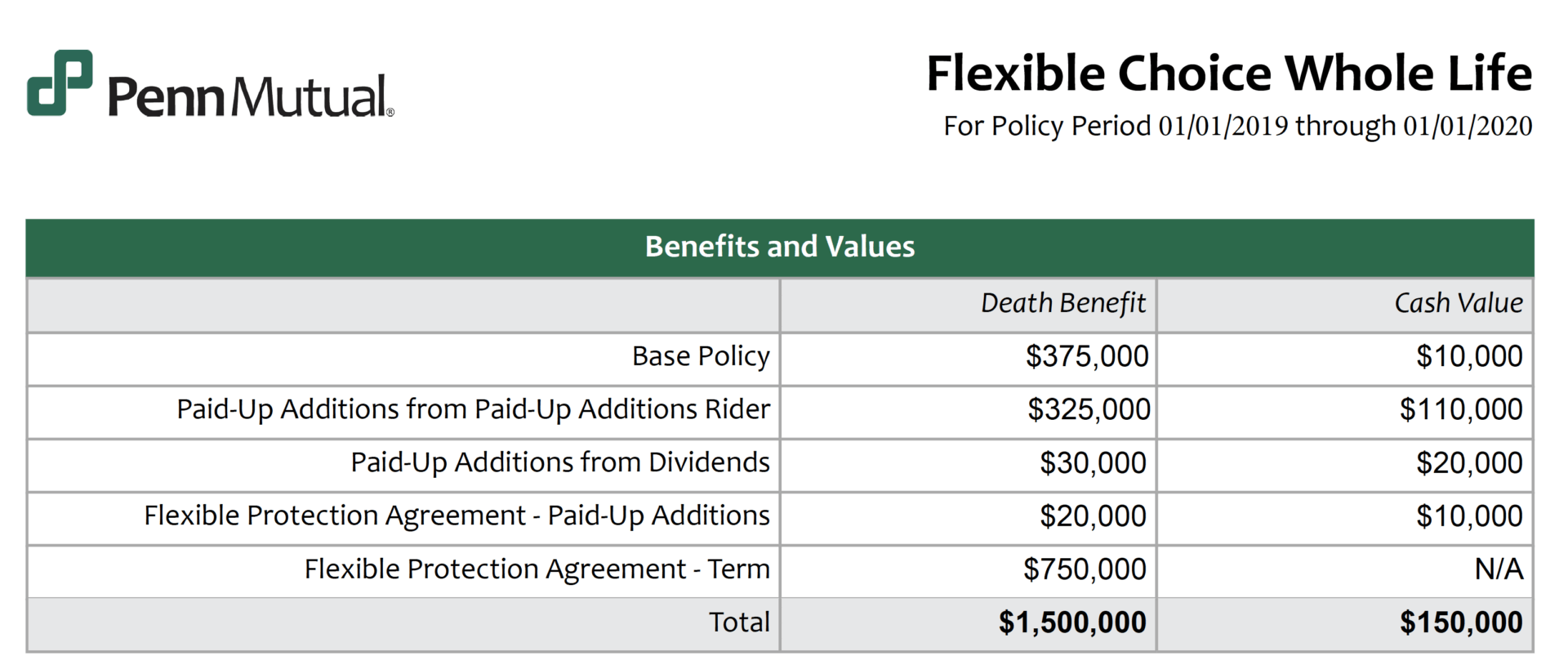

Here's an example of a policy statement with the death benefit breakdown:

Here we see that the policy has $375,000 in base whole life death benefit. There is a term rider that adds $750,000 of death benefit to the policy. The policy has also gained a total of $375,000 of death benefit through the use of paid-up additions. This particular insurance company breaks the paid-up additions into three categories, in this case, some companies will only break it down into two categories. It doesn't matter, the functionality is the same.

By the way, paid-up additions can add an incredible amount of value to a whole life policy, and it's a feature that is well worth understanding. You can gain a master-level understanding of the paid-up additions rider in The Ultimate Guide to Paid-up Additions. Available for immediate excess, now!

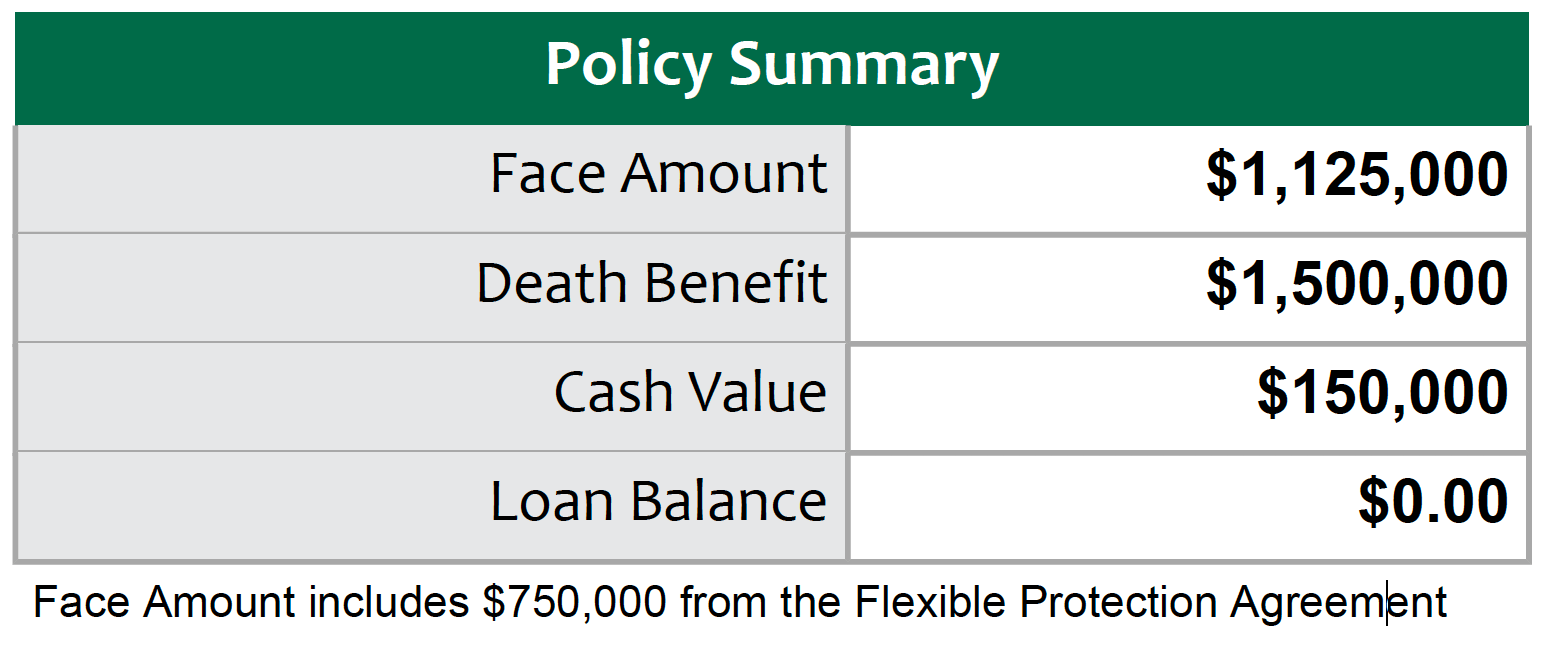

Some whole life statements will report the death benefit and face amount as separate values. This can cause some confusion. Here's an example:

Here the insurer is reporting the original face amount of base whole life and term death benefit and then giving an aggregate value for base whole life, term, and paid-up additions death benefit. This reporting can confuse some people, and insurers may differ on how they report this.

Whole Life Cash Value

Whole life cash values typically breakdown into two broad categories; they are guaranteed base cash value and paid-up additions cash value.

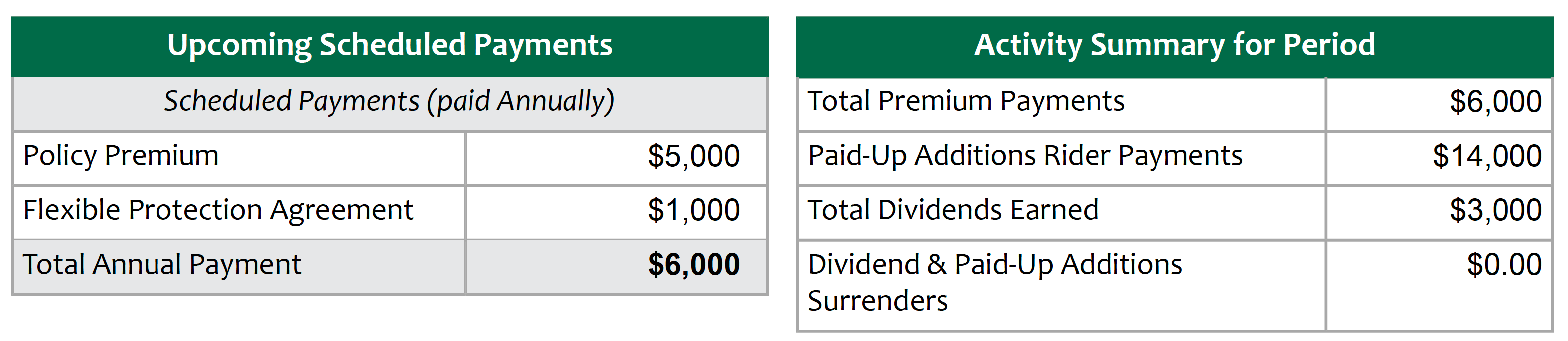

Looking at the example from before we can see a detailed breakdown of the policy's cash value:

The policy's base cash value is $10,000. This is the cash value attributable to the base whole life policy with a $375,000 death benefit. The rest of the cash value in the policy comes from paid-up additions. This includes both the paid-up additions rider as well as the dividend option to purchase paid-up additions.

Some life insurance companies will refer to the base whole life cash value as the “guaranteed cash value.” This is a confusing nomenclature as any cash value presently in a whole life policy is the guaranteed cash value. This is most likely a holdover from older systems and obsolete reporting practices. If you see this, do not worry, all of your cash value achieved in a whole life policy is guaranteed cash value.

Whole Life Insurance Premiums

The annual statement usually breaks down the premiums associated with the policy. This may or may not delineate the exact amounts paid to each premium and also may or may not include the elective paid-up additions rider. But it will normally state what the payment frequency of the policy is. Here's an example from the same policy we reviewed so far:

Here we see that the scheduled premium that includes the base whole life premium and term rider premium are $6,000. The paid-up additions paid in the past year are $14,000. Because the paid-up additions are not considered “scheduled” this company does not include them in the scheduled premium payments section.

Loan Activity

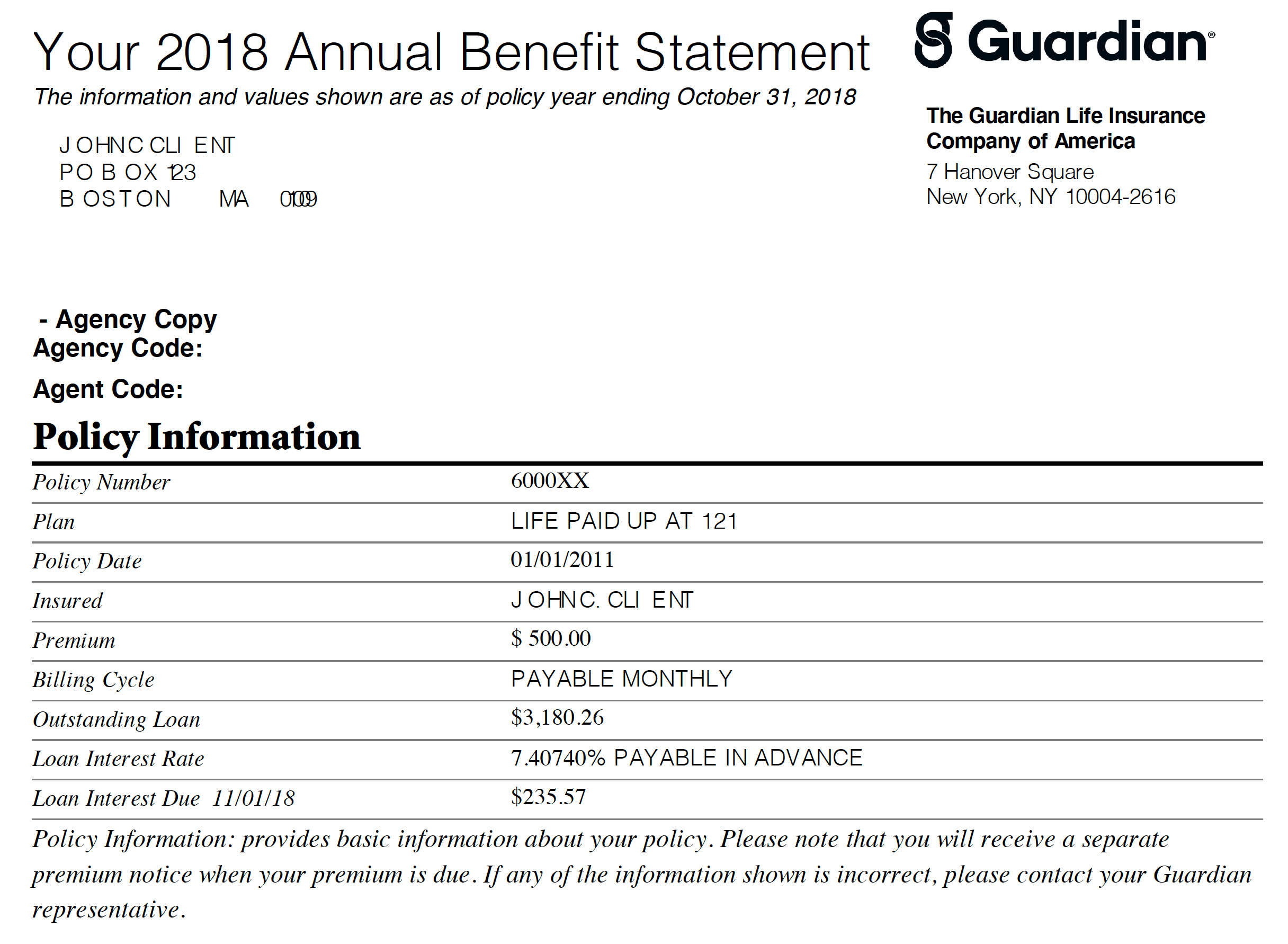

The annual statement will report on any outstanding loan activity. This normally will only report the current loan balance and any loan interest that may be due at the policy anniversary. Here's an example from a different policy with an outstanding loan:

Here we see the client has an outstanding loan of $3,180.26 and the loan interest due on this loan is $235.57. The policy owner can choose to pay the $235.57 or he can choose to add the interest to the loan balance. The company will normally send a separate document to the client around the same time that details the loan, and the option regarding the interest due.

Some of these notices can be a tad confusing and can make the policy owner think the policy is at risk of lapsing. Why insurance companies do this is beyond me, but if you receive one do not immediately worry. There is a good chance your policy is fine and a quick call to the insurance company or your agent can confirm this.

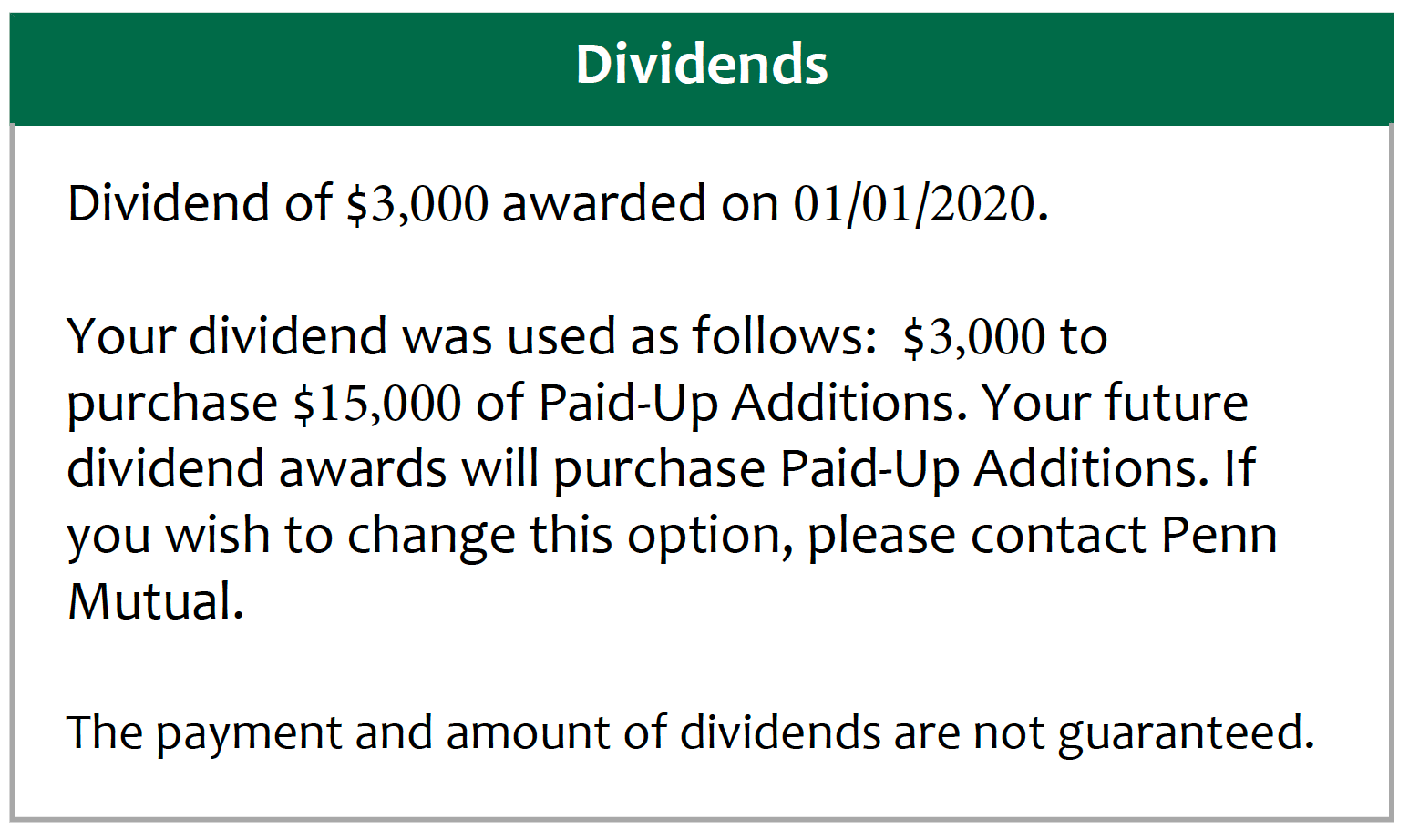

Dividend Activity

If the whole life policy is eligible for dividends, the annual statement will generally report on the dividend received and the dividend option used. Here's an example from the earlier policy we looked at:

Here we see the policy earned $3,000 in dividends and that $3,000 went towards the purchase of paid-up additions. This purchased an additional $15,000 of death benefit for the policy owner. The statement does details this, but this also means there is now around another $3,000 in cash value in the whole life policy.

Notice the statement also mentions that the policy owner has the right to change his dividend option and instructs him how to do this.

Dividends can sometimes cause some confusion for policy owners because they want to reconcile the dividend payment to ensure the life insurance company did the math correctly. Unfortunately, there really isn't a way to do this as the dividend calculation is proprietary information to the insurance company.

The loose rule of thumb is to deduct the guaranteed reserve value from the dividend interest rate (assuming the company publicly announces is) and then take this difference as a percentage against the policy's cash value. This should give you a product somewhere close to the dividend payment, but this is not an exact figure. In addition, multiple variables can influence the dividend payment itself and this might create a higher or lower dividend than this calculation produces.