Podcast: Play in new window | Download

The U.S. stock market just wrapped up one of its worst weeks ever. The Dow Jones Industrial Average dropped around 17% this week alone. The S&P 500 finished the week down 13%. And the NASDAQ fell 12.6%. All of this comes following additional losses in earlier weeks. It's been over a month since the S&P 500 closed up for two consecutive days. The year-to-date numbers are even uglier.

The panic over the Corona Virus is real, and the impact it has on the economy is severe and likely to linger. Despite this, many– I included–hold optimistic views that this will end in the intermediate future and with that end, we're likely to experience a remarkable surge in stock market prices.

But in the meantime, the system is under stress and while owning cash value life insurance certainly brings me a whole lot of comfort, many people want to know what effect this all has on the life insurance industry.

Whole Life Insurance and the Corona Virus Market Crisis

The great thing about whole life insurance is that it's contractually guaranteed to increase in value regardless of market conditions. So no matter what happens with financial markets, policyholders can bank on the guaranteed interest accumulation of their whole life policies.

On top of this, we also have extremely high levels of confidence those whole life policies that earn dividends will continue to receive dividends even the wake of the Corona Virus crisis. The slow down caused by the Corona Virus is serious–no doubt. But, the slow down needed to risk suspension of dividend payments on whole life insurance is still much greater than what the Corona Virus is likely capable of producing.

This being said, I don't want you to assume from the above that whole life insurance is entirely immune to the economic impacts of current market conditions. Falling interest rates will likely place a strain on life insurer's investment income. This strain has a high likelihood to lower dividends–but not completely eliminate them.

The exact impact on dividends paid by life insurers is entirely speculative at this point, but we do have one piece of data that could help offer some insight on who is best positioned to weather the economic storm.

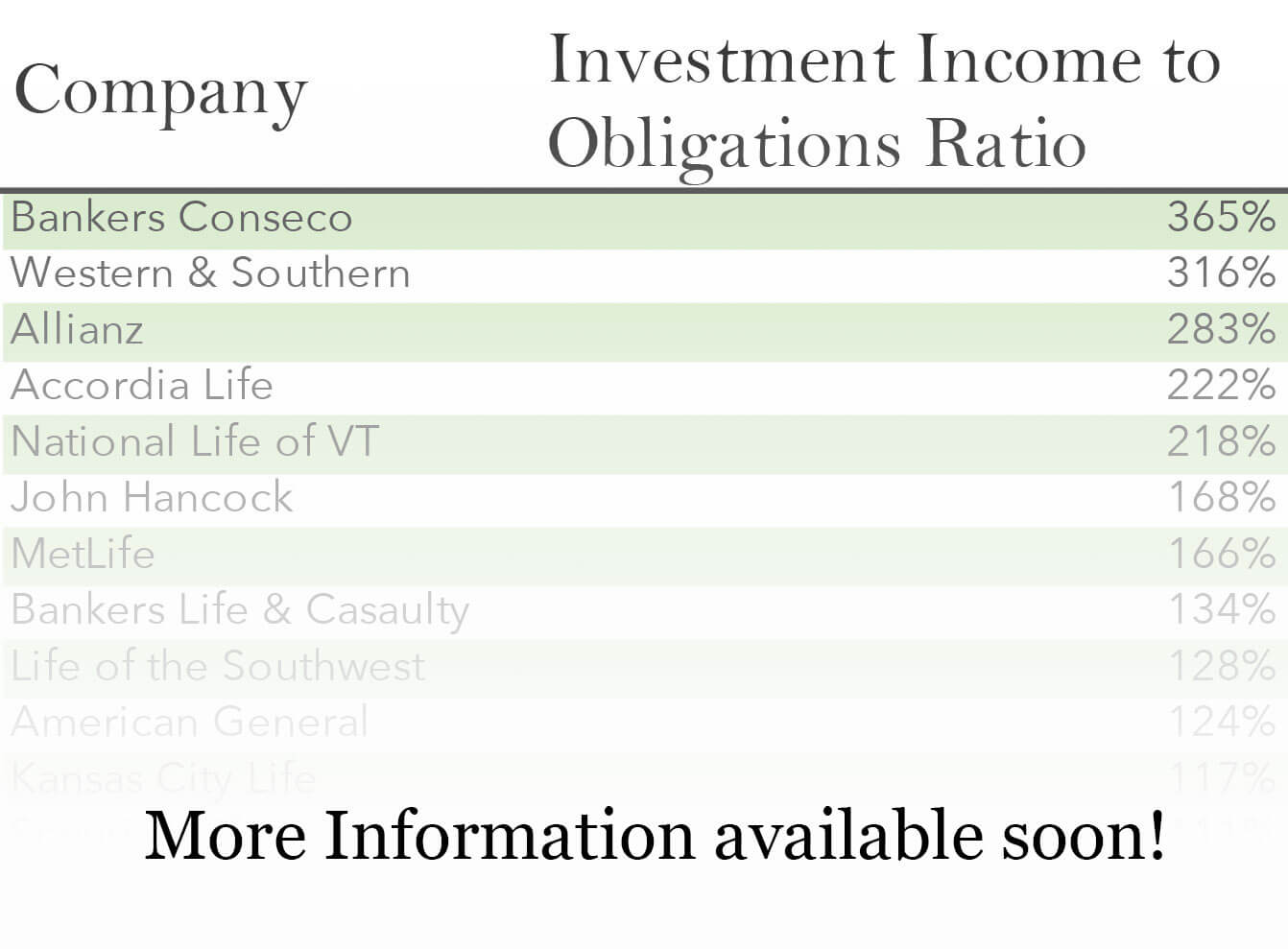

For years, I have mentioned the spread between investment income and contract obligations as a means to check the short term health of life insurance with respect to dividend-paying capabilities. This is the money a life insurer generates from investments in excess of the obligations it owes policyholders–obligations being things like guaranteed accumulation on whole life contracts. Since the inception of The Insurance Pro Blog using this metric to predict dividend action proved accurate.

I've compiled a list of 40+ U.S. life insurers and ranked them by the difference in investment income relative to outstanding obligations. Not all of the life insurers actively sell whole life insurance. Here's an abbreviated version of the list:

Wanna see the complete entire list and hear us discuss it in detail during a private, “members only” podcast? Click here to learn more about that.

Among the companies that issue whole life insurance, there is a wide range in terms of this spread. Some insurers produce investment income that exceeds obligations by a factor of two or more. Other insurers produce as little as 20% more investment income than they must commit to policyholders' obligations.

Universal Life Insurance and the Corona Virus Market Crisis

Talking about universal life insurance in the face of current market conditions requires me to specifically mention each type of universal life insurance because universal life insurance has a wider range of product focuses.

The first and easiest to address is guaranteed universal life insurance. This is a type of life insurance that functions much like term life insurance, only with a longer guaranteed premium payment period than most term policies. These policies exist solely for death benefit protection and have little to no cash value accumulation (you should never touch the cash value in these policies). These policies will continue unaffected by market conditions. With the exception of life insurers insolvency–an extremely unlikely event–policyholders of this type of life insurance will see no change in their policies.

Variable universal life insurance is directly tied to mutual fund-like investments directly tied to the market and will certainly experience serious reductions in cash value if left entirely invested in the U.S. Stock Market. This could lead to increased expenses as the gap between cash value and death benefit (known as the net amount at risk in insurance-speak) increases in this event. Variable universal life insurance policyholders need to take extreme caution in monitoring their policy performance for the next several months to a year. They might want to consider moving cash values to the fixed account available in all variable universal life policies until market conditions normalize.

Current assumption universal life insurance is the old style of universal life insurance that kept all of the policy's cash value in a fixed interest-paying account. The interest payment varied each year when the insurer declared the new interest rate.

These policies do have a guaranteed minimum interest rate payable, and older policies tend to have a higher guaranteed rate than a lot of current fixed interest products on the market. The one thing policyholders of these policies should do is check with their company or agent to determine if the premium they are paying is adequate to sustain the death benefit for the planned time period.

You can read more about this here. Beyond this, these policies will continue to earn interest, perhaps slightly lowered from current interest given recent cuts to interest rates.

Indexed universal life insurance is now the universal life insurance product for cash accumulation. It replaced current assumption universal life insurance for this purpose many years ago. Insurers like it because it opened up an opportunity to lower guaranteed features while at the same time offering a product with the potential to pay significantly higher interest rates than current assumption universal life insurance.

The buying public showed immense interest because they gained protection from losses while also gaining the potential for much higher interest payments than other fixed life insurance policies.

Indexed universal life insurance will likely face lower cap rates given the current market conditions of lower interest rates and higher volatility. This is the case because indexed products are created through the life insurer's purchase of bonds and call options to produce the index feature. Lower bond yields and higher options cost created by market volatility lead to a lower overall maximum reachable return from the investment strategy.

This being said, we predict that 2021 will very likely be a higher interest-paying year for almost all indexed universal life insurance policyholders because the market is very likely to surge higher once the Corona Virus problem passes.

Again, the gap between insurer investment income and policyholder obligations will likely be an indicator for whom in the indexed universal life insurance space can keep cap rates higher and who cannot.

Additionally, I'd predict that life insurers with proprietary index options will have an easier time keeping cap rates higher on those index options. This is due to the uniqueness in the options these life insurers will buy to execute the options strategy for the indexing feature.

How the Corona Virus Market Affects Current Policyholders

For current policyholders of whole life insurance and fixed universal life insurance contracts, the good news is the risk of loss is off the table. Cash values in these policies will remain at current levels and most likely grow while other assets decline and face a multi-year process to return to premarket crash values.

Whole life policyholders will earn guaranteed interest and (almost certainly) dividends in the coming year. Any adjustments to dividends won't impact policyholders until next year.

Indexed universal life insurance policyholders are likely in for a minimum interest payment this year. This means zero or perhaps 1% (if they own a policy with a 1% floor, for example). But the very likely coming market surge as selling pressure eases and recovery begins to take shape will position these policyholders for a really great year most likely next year.

Because indexed universal life insurance policyholders won't ride the market down, the coming surge in the market will be especially nice for cash value growth and accumulation.

Ultimately, policyholders will sleep a little sounder at night knowing that of all the things they have to worry about right now (and there's quite a bit going on to worry about) their life insurance policy isn't one of those things.

This virus has a huge impact on the economy. Everybody is affected especially by the entrepreneurs, so we should not ignore it.Because when it goes on it is really going to cost us a lot. Thanks for sharing this blog with us.