Podcast: Play in new window | Download

The Modified Endowment Contract is mostly an unfavorable reclassification of a life insurance contract that strips it from most of the tax preferential features cash value life insurance enjoys.

This includes:

- FIFO distributions

- Tax-free loans

- Tax-free collateral assignments

There are several subtle but important tax consequences of owning a MEC. A big and often overlooked one is the taxable income recognized on outstanding loans for capitalized loan interest. This means when you take a loan it will accrue interest. When you have a MEC and your cash value is greater than the sum of the premiums you paid, taking a loan creates taxable income. The loan interest that accrues can become additional taxable income if you allow the interest to become part of the outstanding loan.

So many agents learn very early in their careers that MEC's are bad, and most people who research life insurance come away with the same impression.

While not every situation involving a Modified Endowment Contract necessarily means doomsday, the reasons to own one are few and far between. That said, how easy is it to actually have one?

How do You Avoid a Modified Endowment Contract?

You avoid the Modified Endowment Contract by either not paying a premium that violates the 7 Pay Test or not reducing the death benefit to a level that violates the 7 Pay Test while still inside a 7 Year Test Period. This sounds simple, and in truth it is. But for the layperson, this is a much more intimidating task.

We bring this up because a lot of people worry about their life insurance policy becoming a MEC. A lot of people come away with the impression that it can accidentally happen and then they are up that proverbial creek of excrement without any means of propulsion.

But is this fear warranted? Our vast experience says no.

Everyone should understand that all life insurers test cash value life insurance policies for MEC compliance with every premium received. If a violation takes place, the insurer notifies the policy owner. In fact, most insurers send the premium back to the policy owner or hold the premium in limbo awaiting instruction from the policy owner regarding what he or she wants to do with the access premium.

So even if you aren't paying that much attention to your policy and you cross the line violating the 7 Pay test, the insurer will intervene and ensure that you really intend to do what you are about to do.

We've never seen a situation where an insurer allowed someone to pay a premium, violate the MEC test, and no warning occurred. Quite the opposite. Lots of warnings bells go off.

So there's really good news here, the onus really isn't on the policyholder to figure out if he/she has a MEC. The insurance company will take care of this for him/her.

But what about life insurance ledgers that say eventually the policy will become a MEC?

This is based on planned premiums in the future. There is nothing you can do at policy issue that will ensure your policy will eventually become a MEC. In other words, the die cannot be cast on you in terms of MEC violation. You must either pay a premium or reduce the death benefit in the year of the projected violation. This means you can avoid that future projected violation simply by not doing what the ledger assumes you will do in that year.

But what about people who buy a MEC at issue without knowing it?

Hard to do. Very hard to do. The industry adopted plentiful disclosure that will not allow the prospective policyholder to move forward without signing off on the fact that he/she is purchasing a Modified Endowment Contract.

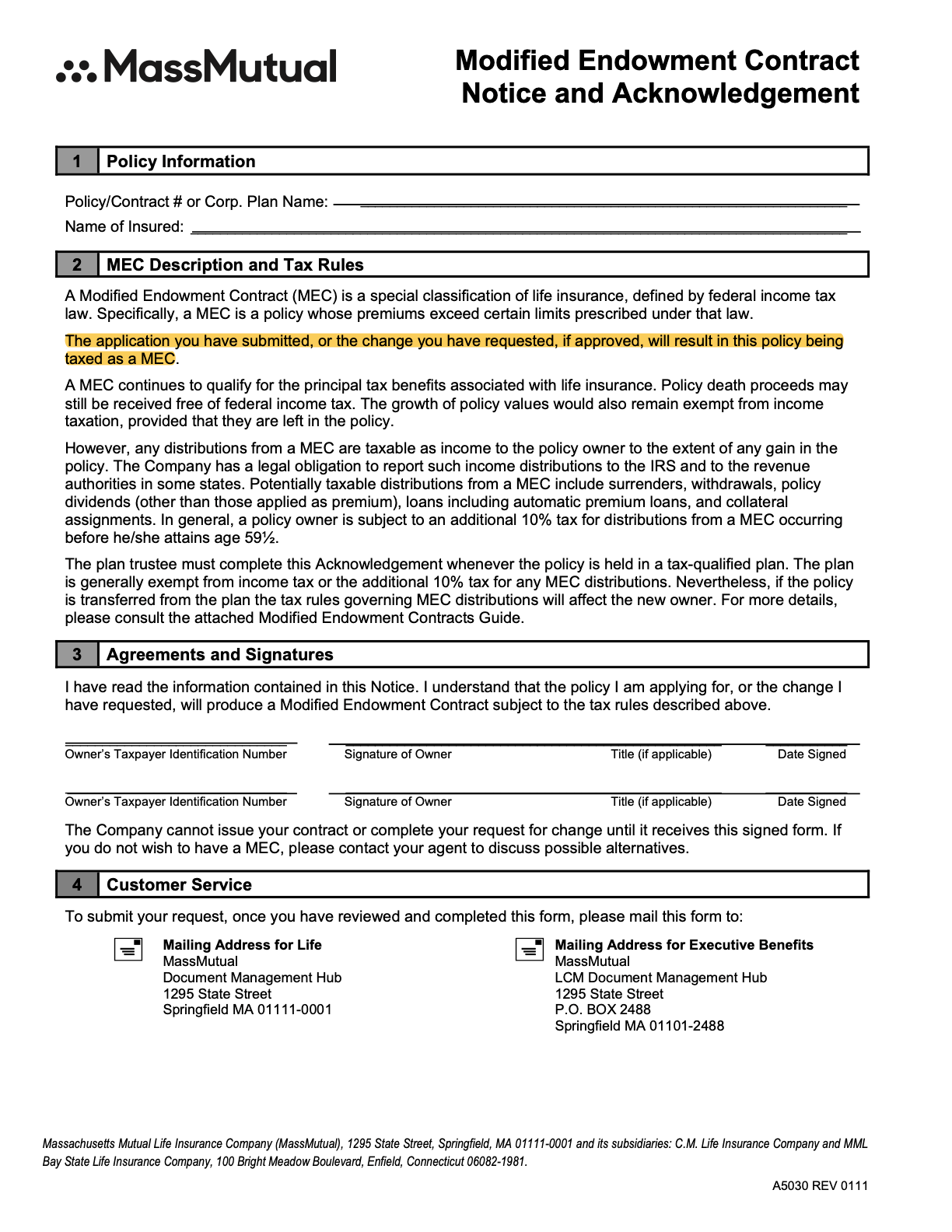

Here's an example of such disclosure from one major mutual insurance company:

I highlighted the section that specifically calls out the purpose of this disclosure. Also notice that the title of this document in bold letters at the top right reads: Modified Endowment Contract Notice and Acknowledgment.

Any MassMutual policyholders (current or prospective) who does something to a life insurance policy issued by the company that violates the 7 Pay Test must sign this form.

Can a Modified Endowment Contract be Reversed?

Yes, you can reverse a violation of the 7 Pay Test and prevent the creation of a Modified Endowment Contract. You do this by requesting the insurance company refund the premium you paid that violated the 7 Pay Threshold. You have up to 60 days after the close of the policy year in which the violation took place. This is quite a lot of time for most situations, and this brings me to my next point.

Given all the warnings and time one has to avoid/reverse a 7 Pay violation, the notion that one can accidentally create a MEC, not know it, and then do nothing about it becomes more dubious by the second.

We have even run into a few situations where the insurance company made an error and thought a violation took place when it did not. There were several warning letters issued, and we were more than welcome to undo the payment that created the violation. Once the company recognized their error, it turned out there was nothing to do. A minor inconvenience, but also peace of mind knowing that the system does trigger.

Bottom Line: It's not that Easy to Create a MEC

So some of the MEC horror stories you might read about on the interwebs are largely overblown by financial “gurus” who either wish to throw shade at cash value life insurance or who don't really know much about the subject. It's extremely difficult if not impossible to accidentally create a MEC and you have to really go out of your way just to buy one.

Of all the people I personally met with a MEC, they either ended up with one when they first bought the policy (e.g. single premium life insurance) or they intentionally paid premium into a policy that created a Modified Endowment Contract. I can recount more than a handful of times where clients of ours crossed the 7 Pay threshold and received an adequate warning that this premium turns their policies into MEC's.

I requested an in force illustration and a second illustration presuming I purchase the max paid up additions without MEC-ing each year for 10 years. Both illustrations came back saying the policy would eventually MEC. I’m about to start my 4th policy year. With the in force illustration of just making base premium payments, how can I “just simply not do what the ledger assumes I will do”, i.e. continue paying the required base premium to keep the policy in force? Besides a 1035 exchange, I suppose I could eventually do a reduced paid up. Is there any way to salvage my policy if it’s not a MEC yet? Concerned about having to start a new policy with new mortality tables, older age, Covid, etc.

Hi Jacob,

I may not be following you correctly, but if you are now going to just pay the base whole life premium and no paid-up additions, you can do that until you reach the MEC limit (if you ever do). The insurance company will tell if that happens and you can opt to not pay the premium out of pocket. This would normally avoid MEC violation.

If you pay the base premium moving forward, do future projections show a MEC violation?

Thanks for the reply. Yes, the in force illustration of just making the base premium going forward (I had made PUAs in policy years 2-3) say I will MEC in year 25. I know that’s far away, but it’s right near retirement when I may want to access my cash value tax consequence free for a variety of reasons. And if I only make the base premiums going forward, I’m not building much cash value. Also, my policy will be a year or two away from being fully paid up. Would using cash value instead of paying out of pocket those last two years possibly prevent the MEC? But then again, I wouldn’t have that much cash value under that scenario. What are your thoughts on a 1035 exchange?

It’s tough to say from here without actually reviewing the policy. It might come down to a change in policy to correct if there really is no way to avoid the problem. We can provide more guidance, but reach out to us through this contact link so we don’t put your personal information all over the internet.

I have been using a MEC account as a cash accumulation and preservation method with growth opportunity based on CAPS. I am not very interested or need the insurance; just a nice side benefit. I am wondering what your experience is with various MEC providers, and what advantages vs disadvantages you see in the various providers offerings? In particular, I am interested in growth CAPS and any withdrawal issues (I am 63 so not worried about tax penalties at this point)?

Hi Elliott, unfortunately, this is way too broad a question for me to answer.