Indexed Universal Life Insurance is the dominate form of fixed (i.e. not involving any direct investment in mutual funds) universal life insurance for cash accumulation, and just like whole life insurance can be manipulated by agents and brokers to maximize cash value produced by the policy.

Just like last weeks discussion, the change that we make to optimize cash value does not require that the policy owner place any more money into the policy than he or she was planning, it simply comes down to properly designing the policy to focus it on cash accumulation.

It should also be noted that with universal life insurance, there tends to be a greater divergence in terms of cash value development between policies that are designed to provide cash accumulation and policies that are designed to focus more on sustained death benefit—and this goes beyond the simply distinction between universal life insurance policies that are designed to have an indefinite secondary guarantee. If you don’t know what that last statement means, don’t worry too much about it.

Just know that correct policy selection for universal life insurance is just as critical as it is with whole life insurance.

Again, a Huge Difference

Just as we noted with the whole life insurance post, there is a huge difference between the cash that can be generated from a properly designed policy, and the type of policy most agents and brokers tend to implement for people. And in this cash the difference is even more substantial.

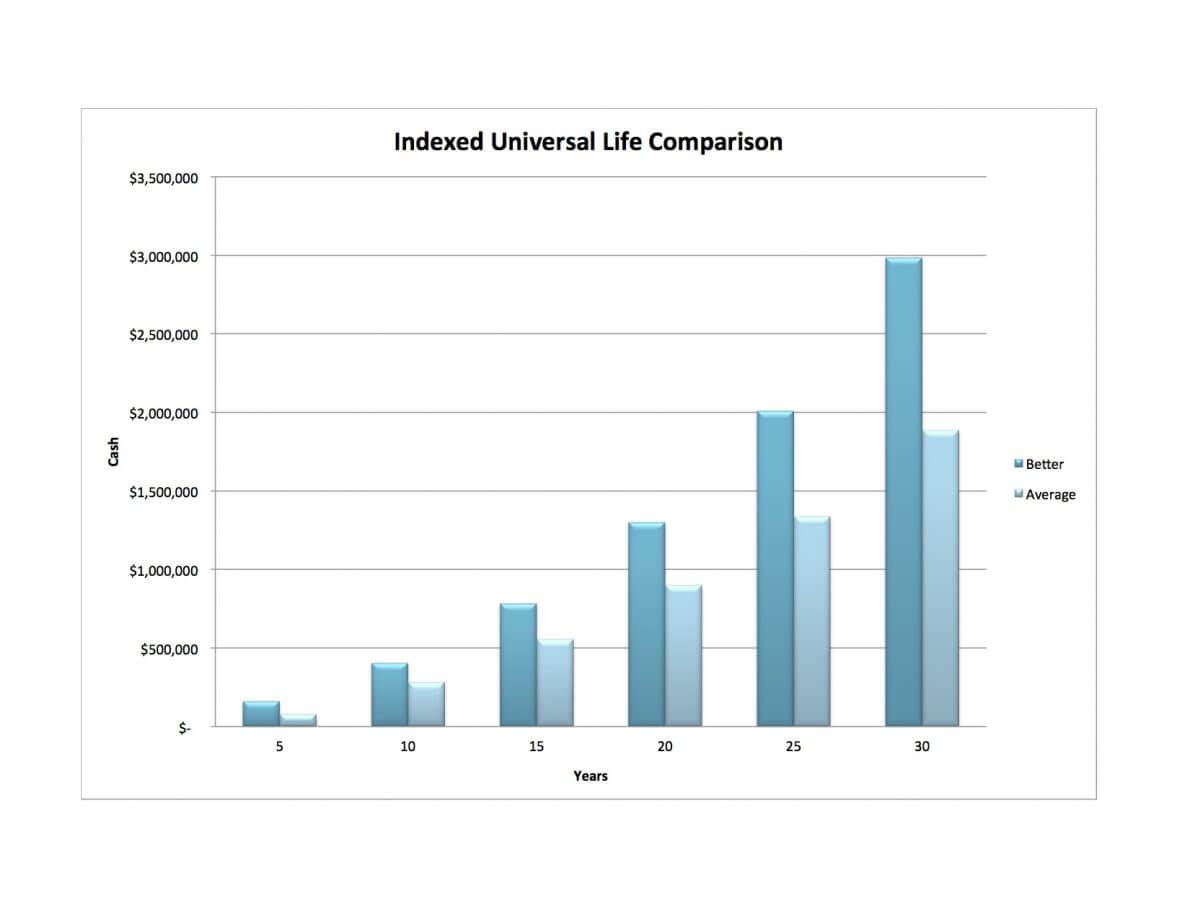

This time we took 10 different examples from leading indexed universal life insurance policies designed the way they are generally put in force and took the average results from this 10. We then took the top performing indexed universal life insurance policy from the crowd and designed it to maximize cash value.

Looking at the difference in cash value performance over a 30 year period, we see the average increase in cash value for the “better” designed policy is over 50% more cash value.

Let’s depict that difference graphically from our actual numbers:

Just like last time, we used a $35,000 annual premium for a 40 year old male. You’ll notice from the graph above that there is more than $1 million more cash value in the properly designed indexed universal life insurance policy.

Reduction in Death Benefit

Unlike whole life insurance, we generally will have a reduction in death benefit with a properly designed universal life insurance policy. This is due to the unique difference in the way universal life insurance qualifies as life insurance.

The reduction in death benefit means that after year 30, the policy designed for cash value had about 12% less death benefit than the policy not designed to optimize death benefit. It does, however, have 58% more cash value.

Indexed Universal Life Insurance Versus Whole Life Insurance

It’s also worth noting that difference between the optimized whole life and indexed universal life insurance policy. The universal life insurance policy has more cash, a little less than $500,000 more. That’s 20% more cash value.

The whole life insurance policy has more death benefit. A little over $500,000 more death benefit. That’s about 13% more death benefit.

So again, we see an aged old key consideration driving between the two product types. Those who think that death benefit will be crucial later on, should give more consideration to whole life insurance (providing that additional death benefit beyond what the indexed universal life insurance policy provides is needed).

On the other hand, those who are more focused on cash value will likely benefit more greatly from universal life insurance. Let’s remember that there are also a few more key considerations between these two.

One Potential Benefit to your Old Universal Life Policy

Unlike whole life insurance, it’s possible (note the emphasis, please) that universal life insurance that has already been put in force can be changed later on to optimize cash. So if you bought one, and it wasn’t designed to maximize your cash, it might be possible to make some changes and salvage the money you’ve already spent on the policy.

If you have questions regarding how indexed universal life insurance or whole life insurance can be maximally benefited for you, don’t hesitate to contact us we’ll be happy to help you out.