Podcast: Play in new window | Download

The debate between life insurance company structure rages on into the 21st century. It's not as big a headline as it once was in the industry.

So, does that mean that we've decided that it really doesn't matter? Obviously, there are real structural differences in the capital structure and there are perceived differences in the culture of the two types of life insurance company, but are there any real, practical differences?

For more of a primer on the distinction here's an excerpt from a post Brandon wrote back in 2013:

Maybe you’ve heard this one before, the claim that mutual life insurance companies are better than public life insurers. Of course, the mutual life insurers all think so. But we’re willing to bet that the so-called public life insurers would tell you differently.

So is it true that the non-mutual life insurers are just out to swindle everyone out of their money and represent all that is wrong with American capitalism? Or are the mutual just stodgy companies that have a problem embracing modernity…and the capital markets. 😉

Let’s Set the Stage

So a little background is in order. Mutuality is arguably the original insurance design. At least this is what you’ll hear if you let a mutual company employee tell you the story. In truth insurance actually gets the majority of its origins more from fraternals/benefits societies but those are details and who has time for details?

The claim is that mutuality is the natural starting point for a stock insurance company. A provider of insurance places ownership in the company in the hands of the individuals who hold insurance policies from the company. Because of this, the company is beholden to its policyholders and this perfectly aligns the company’s values and goals with the policyholders’ values and goals.

She’s Gone Public

Excuse me for making an obscure reference to a country music song I can’t actually tell you the name of (I’m the one from Vermont). Starting about two decades ago, several mutual companies decided to ditch the restrictive nature of mutuality and go public. Doing so enables them to raise capital via the U.S. capital markets (i.e. selling pieces of yourself or issuing public debt, though mutuals have some choices regarding that last one, just not quite in the same way).

This corporate structure turns the company into a public corporation, one with stock holders and a board of directors whose fiduciary responsibility is to deliver profits to those stock holders who may or may not be policy holders. There’s no requirement to be a policy holder, you simply have to pony up cash to buy company stock. This very fact, according to the mutuals is pure evil.

Us vs. Them…we have a Problem

The first big problem we have in comparing company structure is that fact that it’s not so clean cut. The world isn’t composed exclusively of mutual insurers and public company insurers.

No, that would be too easy. In addition we have other corporate structures like privately held insurance companies, or insurance companies held by a corporate entity known as a mutual holding company. While neither of these companies have public stock holders, ownership depends on structure.

For some ownership may be placed with a individual or corporate entity, for others ownership rests with the policy holders…sort of.

We’d be remiss if we pretended that this third category didn’t exist. And in truth it’s more like a 3rd, 4th, 5th, and so on category, but for simplicity’s sake, we’re going to combine them all into a catchall category. Not quite mutual, and not quite public.

Us vs. them vs. them

So now that we understand there are actually three different categories, the question still remains. Is one really better than the other? The mutuals, of course, would still have you believe that nothing but pure mutuality is worth your time. The public companies would highlight their access to quick cash when in need, and the third group we just learned existed would have some great story we’re quite sure to highlight why they are special (probably something in between the other two).

But for those of you who have spent any time reading anything else I’ve written, you likely know that I’m not big on feel good stories. I like numbers, because numbers tell truths. So, let’s try to quantify this just a bit.

Methodology

I’ve broken life insurers into the following three categories:

- Public Insurers, which is actually insurance companies owned by public companies (more on that in just a minute

- Mutual Insurers

- Hybrid, the catch all category that represents companies that are owned by private entities or mutual holdings companies

I took the top eight companies—top eight due to limitations of Ebix’s Vital Signs software—in each category ranked by general account size as of the 2011 issue of the American Council of Life Insurer’s Handbook (2011 happens to the best the latest edition I have in my possession).

I specified insurers owned by public companies above because life insurance companies themselves are rarely public companies. Instead, a public entity like a financial holding companies tends to own the insurer. In these cases I used only the major insurer owned by the public entity.

For example, MetLife, Prudential and American General are companies represented by the public company cohort. And the actual public company in all three cases is a holdings company that owns numerous insurers.

So, I’ve taken data from the Metropolitan Life Insurance Company, the Prudential Insurance Company of America, and American General Life Insurance company only (none of their sister companies were included).

At the same time I should specify that I only used the primary insurance company when evaluating the mutual insurers. For example, New York Life is a mutual life insurer that happens to own an extremely large insurer whose primary function is to manufacture annuity products. That subsidiary company was not included in the mutual companies.

The hybrids vary quite a bit. From the somewhat awkward not-for-profit insurer TIAA-CREF to bona-fide mutual holdings companies like Pacific Life and Ohio National to privately held insurers like Midland National.

I then looked at the following eight (this time no limitations, that’s just the number it comes out to) critical company performance metrics:

- Surplus Ratio

- Average 5 Year Total Investment Return

- Risk Based Capital Ratio

- Dividends Paid in 2011 among all companies in the category

- Average Expense Ratio

- Average Interest Margin

- Interest Payments

- Total Insurance Inforce

This last one has nothing to do with soundness of the company, and everything to do with keeping a few other metrics in relative perspective.

Results

I’m going to walk through each category and explain what we’re looking at and why. And then give the results among the categories of companies.

Surplus Ratio

Surplus ratio tells us the amount of capital the company holds in excess of its legally required reserves relative to the total size of the company. For example, if insurance company A has $100 billion in assets and holds $10 billion in access capital (above reserves) than it’s ratio is 10%, the higher the ratio the better in most cases. You could also think of this as the rainy day fund in a crude sense.

This is a metric that the mutuals spend a lot of time talking about. Their conservative nature, and in some cases statutory requirements, leave them with usually high surplus ratios. So how do they stack up to everyone else?

As you can see they certainly boast surplus well in access of their public company counterparts. But this isn’t a category they dominate. The Hybrids actually maintain slightly better surplus positions on average. Meaning they too could be considered just as secure with respect to saving for a rainy day.

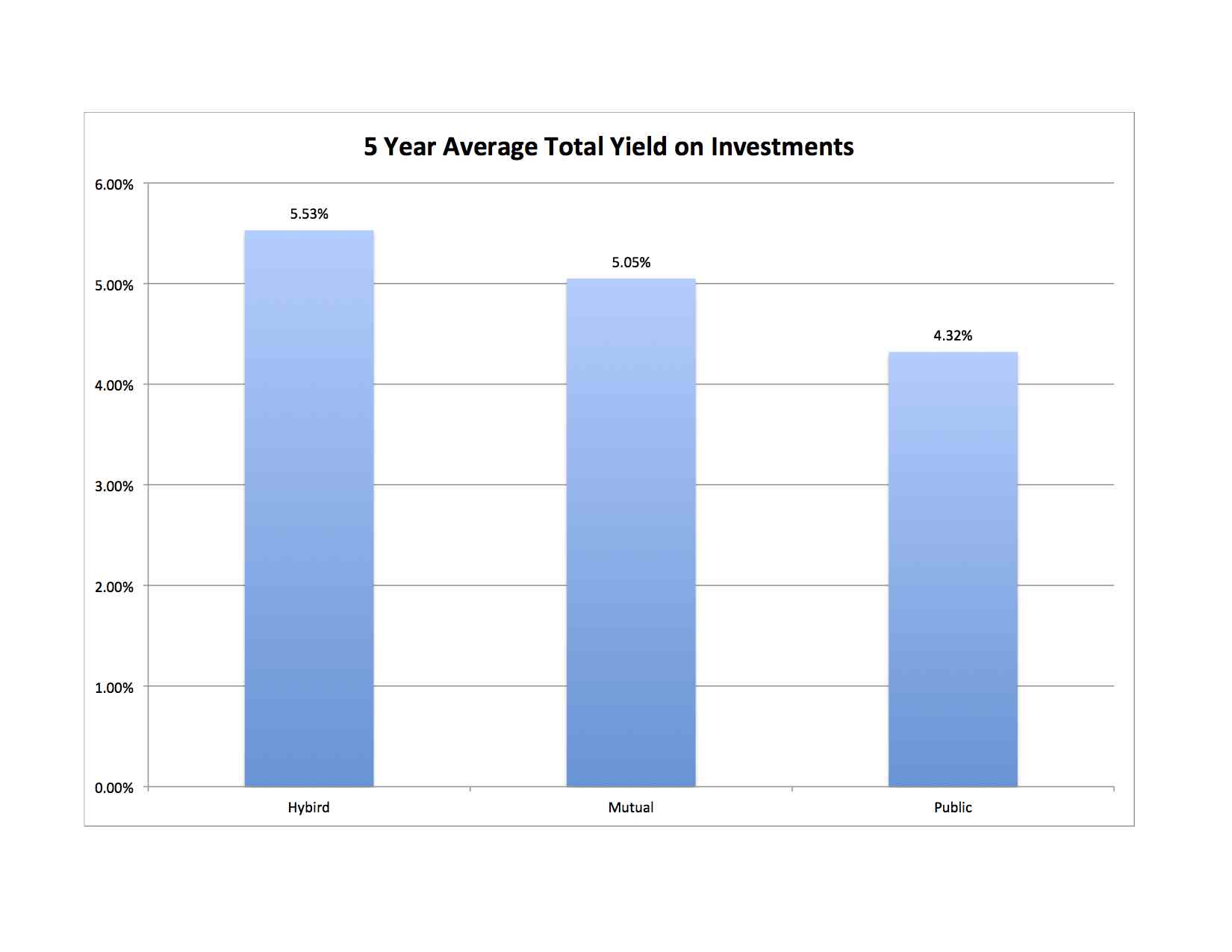

Average Investment Return

I’ve talked about the importance of investment return on the general account before. This is a metric that shows us how well the insurance company's CIO is doing with company assets, and helps us predict to some degree how successful the company will be at maintaining competitively priced products and yielding attractive returns on their cash value focused products.

This is a category all insurers would like to boast superiority in, so who comes out on top? The hybrids win, again.

This is interesting and some what counter intuitive. In large part because (as I’ll detail later) the hybrids mostly make up much smaller life insurers. Theoretically the larger companies should be able to attract top talent. Who doesn’t want to say I’m an investment strategist for Prudential vs. saying I’m an investment strategist for American United Life Insurance…who the heck are they?)

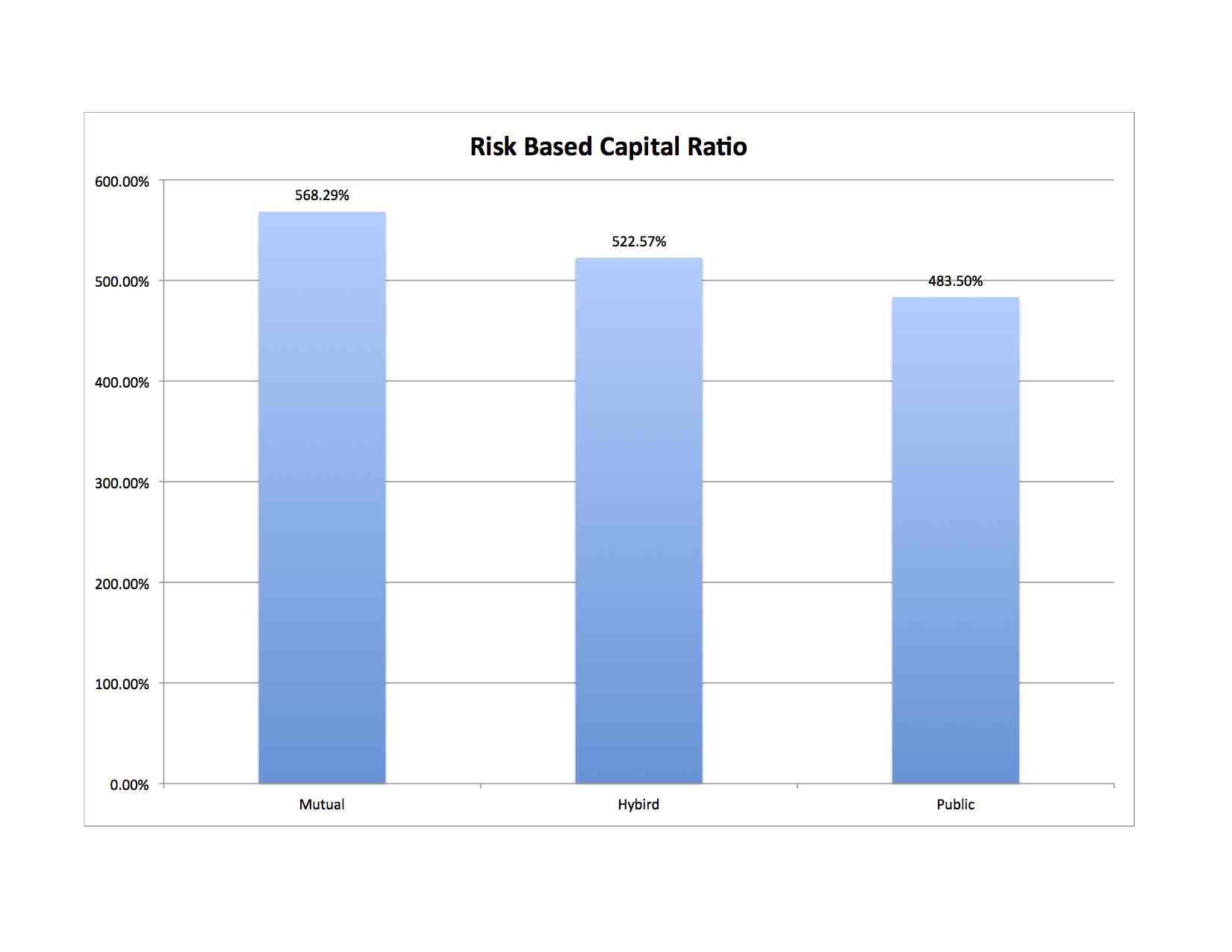

Risk Based Capital Ratio

Risk Based Capital Ratio represents the amount of capital the insurer has above it’s legally required reserves adjusted for default risk. Like the surplus ratio it’s another rainy day fund-like measure where the larger the number the better. Of course then, it seems obvious that this would be another metric the mutuals are all over.

Georgia and Vermont.. and no mention of the Super Bowl in the past 2 podcasts..

It’s still too soon 😉

And we (Atlantans) appreciate it 🙂