Podcast: Play in new window | Download

In exploring what we should talk about in episode 44, we realized that we've somehow gone almost an entire year without dedicating an episode to a discussion of taxes in relation to life insurance. Oops!

Sometimes we get caught up in focusing on finer points and miss the big picture. But we are correcting that today.

We've actually published quite a bit of information on the topic over the last 5 years and for those of you who prefer the written word…carry on. You'll be please with what you find in the proceeding paragraphs.

Rather than re-inventing the wheel I'm going to pull from a piece that Brandon published a few years back.

Full disclosure: at no point is Brandon or Brantley referring to life insurance as an investment. That gets certain regulatory agencies in a dither and ain't nobody got time for that 😉

Always consider the impact of income taxes.

They have a tremendous compounding effect on a buy term and invest the difference strategy over a 40 or 50 year period. Don’t discount the eroding effect of taxes.

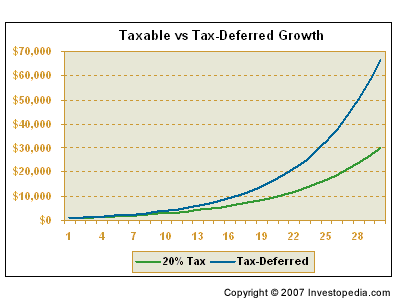

Tax Deferred Growth

This one is so simple, and yet people remain mystified by it. The math is easy, if X > Y than df(x)/dtime > df(y)/dtime, where f(x) and f(y) is defined as the compound annual interest of X or Y for a given interest rate.

What?

Sorry for the dork out moment, it simply means if X is larger than Y than the the growth rate of X for the same interest rate compounded annually will be larger than Y.

Graphically it could look something like this:

The difference between the green and blue lines represents the taxes paid each year on the investment represented by the green line and the loss of earnings by virtue of having a lower principal base.

Tax Free Death Benefit

As of the publishing of this article, Google reports several thousand monthly exact searches in the United States of various combinations asking if life insurance is taxable.

While some of those inquiries probably seek out information on cash values (something I'll be discussing a little further down) I'm guessing the majority of them are focused on the actual death benefit.

The answer 99% of the time is no. I made that statistic up, but I'm willing to bet it's true with a 95% confidence interval (I'm on fire today!).

Circumstances that would create a taxable death benefit include the following:

-

- Goodman Triangles. This happens when the insured, owner, and beneficiary are all different people/entities. It creates a gift tax implication.

- Taxable Estates. Life insurance owned directly by the deceased, or gifted by the deceased where a gift of future interest exists (contact us, and I'll explain what that means) is included in the deceased's gross estate. If the gross estate goes beyond the Federal exemption (currently $5.25 million, the fiscal cliff debate actually did something useful) than any amounts in excess of that amount are estate taxable. In certain circumstances that might make life insurance proceeds taxable by estate tax

- Group insurance beyond $50,000. This one requires some careful attention. Group insurance under $50,000 is always tax free under current law. Death benefits beyond $50,000 are taxable at income tax rates provided the employee on whose life the benefit covers does not recognize the premium that provides the benefit amount beyond $50,000 as imputed income and as such would pay income taxes on that imputed income.The imputed income is the One Year Term insurance cost of the death benefit (typically a very small number). The good news is, most HR departments are skilled enough to know this, and they default benefits in excess of $50,000 to imputed income. Technically you have a choice, but choosing not to recognize the premiums as imputed income and making the death benefit partially taxable would be extremely odd.

- Improperly implemented EOLI, COLI, and/or BOLI. Those acronyms stand for Employer Owned Life Insurance, which is what both Corporate (sometimes Company) Owned Life Insurance (COLI) and Bank Owned Life Insurance (BOLI) are. EOLI requires certain documentation in order to comply with current insurance law and ensure the death benefit remains non-taxable to the employer. Further, in circumstances that makes use of additional non-qualified (i.e. not tax deductible to the employer) benefits to the employee, there are tax implications that must be recognized by the employee to maintain the tax free status of the benefit offered by the employer.

As you can see, all of these circumstances involve some degree of complexity, and most people (99% I'm telling you) can purchase life insurance without a lot of worry about taxable implications of the death benefit.

First-In First-Out

When it comes to calculating your taxable implications of a withdrawal from a tax deferred account there are generally two methods, First-In First-Out (FIFO) and Last-In Last-Out (LIFO).

FIFO

FIFO means that withdrawals take out the tax free basis of the policy. The basis is the amount you put into the policy (i.e. the money you already paid taxes on).

Wait, I didn't pay taxes on my 401k? How does that work?

401k's do not have a cost basis, and as such all money withdrawn can be subject to taxes.

LIFO

LIFO is the exact opposite. It means all money withdrawn is the taxable gain first as that's the last part of the growth in the policy–so it comes out first.

What's the big deal?

FIFO allows you to touch money in an investment account without a taxable implication. This is why you'll hear “withdrawals to basis, and then policy loans,” mentioned as the method for creating tax free income on a life insurance contract.

Also, having access to the basis first allows you to drop money into a contract and take advantage of any growth by dividends or interest, and then withdraw the money to use elsewhere (usually not an ideal method, but workable in several circumstances).

Tax Free Income

This one is the big one. We know we can draw out the basis tax free, and we touch that money before we touch any of the growth. And then we make use of policy loans to further access money without realizing it as income.

Now, there are those who like to play games with semantics to suggest this is evil. The insurance company charges you interest to use your money. 😯

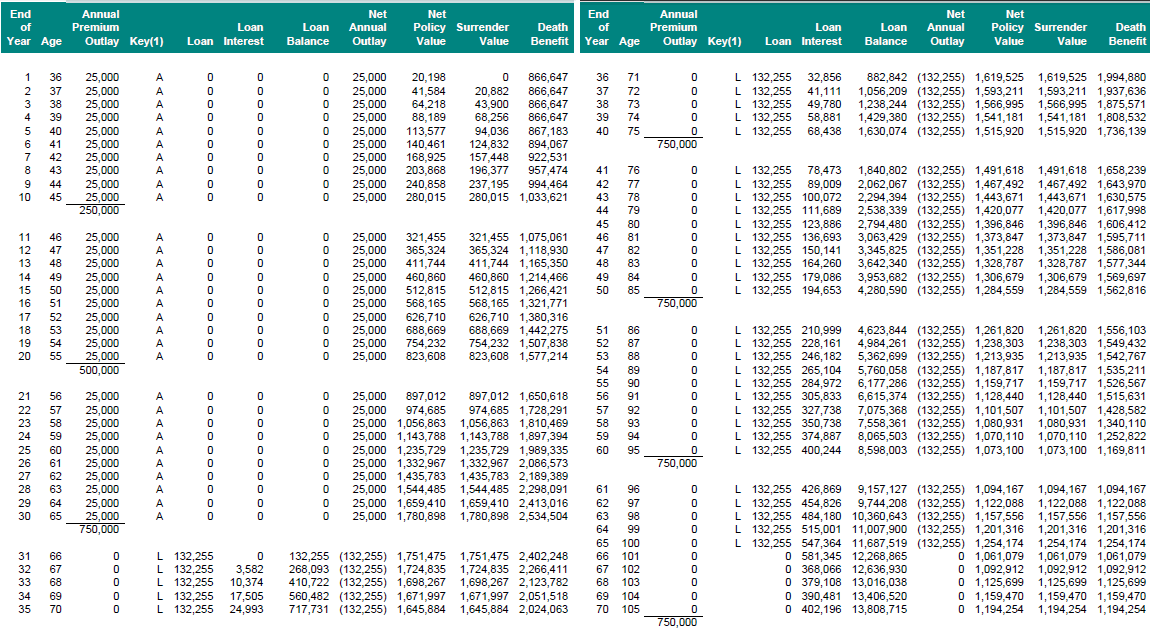

And for the less observant among us, you might just fall for it. Truth is, you can generate some substantial tax free income despite “paying” all that interest to the insurance company. Here's an example:

This is an indexed product and we are using a 6% assumed average rate of return.

Notice that when the income begins we're withdrawing 7.4% of the principal. And what would be needed if we were using a taxable account? Let's assume a 25% effective tax rate, it means we need to increase our withdrawal to $176,340 to match the same buying power.

This represents just a hair under 10%. So, we'd need to do better on the actual return side.

What is the effective annual rate of return? The TI-83 tells me 5.11% per year.

So what number would I need to hit my taxable goal of $176,340?

The answer: $2,382,972, meaning I need to achieve a 6.69% rate of return, completely doable. But wait, should I really pull 7.4% out of an account that is subject to ups and downs like the stock market? Fidelity and Vanguard tell me no.

So what if I was going to be daring and scale back only to the old magical 5% withdrawal rate? Then I would need $3,526,800. My annual rate of return needs to be 8.75%. Not necessarily unheard of, but now we're reaching into the upper bounds and our probability of achievement is dropping exponentially.

And what if taxes go up? Could they?

Yes, they could indeed.

Hey Wait a Minute! Wasn't I Paying Interest and Insurance Fees?

Why yes you were. And the depiction above takes all of that into consideration. So, despite those terrible insurance costs that destroy your investment rate of return potential, and that interest that the insurance company charges you on your money the net effect isn't so bad when you know how to properly design life insurance.