There's little doubt you’ve read a great deal of swirling about in the media regarding Long Term Care Insurance (LTCi).

And, you may be asking yourself—should I buy the coverage or not?

As usual, my answer will be…that depends.

There's little doubt you’ve read a great deal of swirling about in the media regarding Long Term Care Insurance (LTCi).

And, you may be asking yourself—should I buy the coverage or not?

As usual, my answer will be…that depends.

For a while, Brandon and I have been discussing the coming 401k bond blood bath for people who are retiring and have been planning for years to shift their asset allocation to a much more conservative posture. Remember when the conventional wisdom was that during your retirement years you would shift the weighting of your investment portfolio to income producing assets…think bonds.

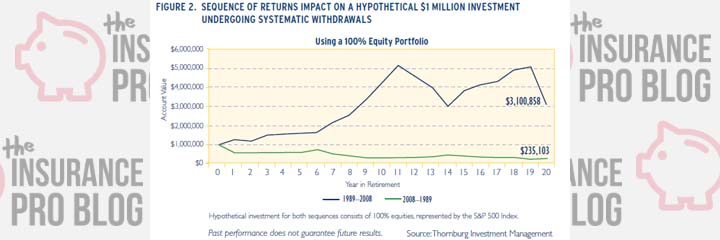

We've heard a lot recently about the fiscal cliff and the second dip, so recently I decided to spend a weekend reviewing stock market charts. Some of you might remember this guy from last year. Consider this part two.

Bill Gross of PIMCO, the authority on bonds (or so they say) announced earlier this month that the days of investing in equities for the long run (you know the sales slogan of Merrill Lynch, Morgan Stanley, Edward Jones, and company) is over.

Now, does it surprise us that the head of the the largest bond fund in the world is suggesting stocks are toast insofar as they are a long term investment/savings strategy? Does it surprise you that a blog dedicated (at least in part) to alternative asset classes would be talking about it? Now that we have everyone's self interest out of the way, lets get into what's interesting about Bill Gross' comments in his proclamation.

If you've read any of my previous posts, it's no big surprise to you that I'm very passionate about the subject of retirement income. Honestly, I think this is one of the biggest boondoggles for financial advisors, investment companies and life insurance companies.

None of them have been prepared for the growing demand that is now upon us to help our clients distribute their accumulated wealth in the best way during their retirement.

Many consumers and most agents assume that because interest rates are at an all time low and thus cap rates are at an all time low, the fixed index annuity is no longer a viable alternative to other investments such as CDs and the stock market. However, this is an extremely narrow point of view and one that could seriously damage a client’s future retirement income.

See, my opinion is that a retired person should be more concerned with their income than with the growth of their assets.

Today the most fascinating experiment on the human condition took place on (of all places) Facebook. When I took my somewhat usual stroll into check Facebook this morning I happened upon a post with a very simply math equation: 9-5+5*0+3=?

Let's start with a brief discussion of modern portfolio theory (MPT) just to make sure we're all on the same page. To avoid a less than exciting academic foray into MPT, I'll provide a basic definition.

Basically, the theory is that individual investment (a particular asset i.e. stock or bond) selection should not be chosen on their own merits. What's more important is how each asset's price moves relative to all the other investments in a portfolio. Harry Markowitz was the first to articulate this concept back in 1952.

Typically a multi-year guaranteed annuity and the term “CD annuity” are used interchangeably within marketing literature. While the description is accurate in describing conceptually how the product works, I feel it could be a little misleading to consumers.

An annuity is NOT a CD, it’s not related to a CD, and the two really shouldn’t be compared as much as they are. Later on I’ll get into some of what really makes them different. The differences may seem subtle to some but they are vitally important to understand.

Ah the Pension. A long sacrosanct retirement vehicle known for its rigidity and stability. The anchor that led many American's into a comfortable retirement. That was, until the late 70's early 80's when a few pieces of legislation dramatically changed the retirement planning landscape and gave way to a new (and much cheaper for some people) focus to retirement planning.

We'll ignore all of that for a minute, and instead focus on what exactly a pension is, and then come back to why it has sort of gone the way of the dodo.