Cash value life insurance, also known as universal life or whole life insurance, is a form of life insurance that builds cash value. You can use this cash value for a number of different options including pay premiums due, withdraw a portion of the cash to use as retirement income, or surrender the entire policy and move the cash to some other investment.

Unlike term life insurance, cash value style policies do not have an expiration date. This means they can remain in force for your entire life. But some cash value products do have a maturity date that might require you to accept the cash value built up in the policy and cancel your death benefit.

How Do Cash Value Life Insurance Policies Work?

Cash value life insurance requires a premium for a death benefit chosen by the policy owner. Paying this premium also causes the policy to build cash value.

Once the policy accumulates cash value, the policy owner can choose to access the cash value through an array of options. This might include exercising a nonforfeiture benefit offered by the life insurance contract. Alternatively, it could be taking some of the money out of the policy through a withdrawal or policy loan.

Using the cash value in a policy comes with little strings attached. Cash value policy owners have the option to remove money from their policies without facing limits or taxable consequences found on many retirement investment accounts.

Additionally, cash value policies offer a wide array of tax-favorable benefits that attract many insurance buyers to the product.

What Kind of Fees does Cash Value Life Insurance Have?

Some people criticize these types of life insurance for their fees. Cash value life insurance policies definitely have fees and some policies have considerable fees.

For some products, these expenses are clearly spelled out in a special report that accompanies the life insurance illustration. But for other products, the costs are very difficult to ascertain. This, not surprisingly, leads to criticism and warnings about cash value-style products.

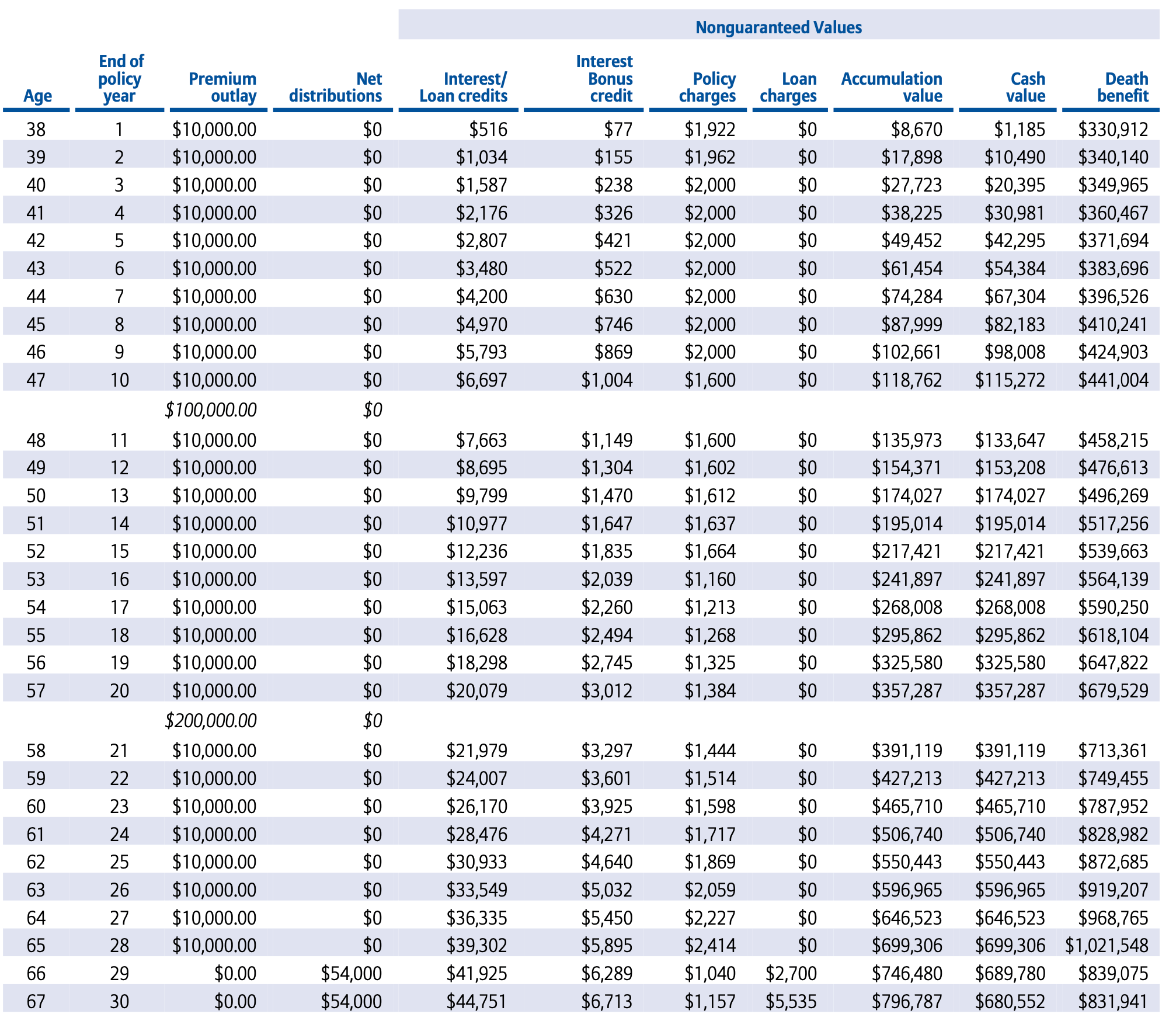

Universal life insurance products will provide a detailed breakdown of policy expenses. This report accompanies the life insurance illustration. Here's an example of a typical policy cost breakdown report:

This report shows us the annual charges assessed against the policy in the column titled “Policy Charges.” This report also details the loan interest charged if a policy loan is outstanding (see years 29 and 30).

Whole life insurance, on the other hand, does not provide details on policy costs. Some people refer to whole life insurance as the “Black Box” for this reason. The product operates in relative secrecy and never discloses the actual fees the insurance company deducts from the policy.

Types of Policies

Life insurance options for cash value-style products come in two basic forms; whole life insurance and universal life insurance. Both types of life insurance operate under the same basic principles of any life insurance policy. They both offer life insurance coverage, have a premium payment you must make for a certain length of time, and they will both pay death benefit proceeds to your named beneficiary upon death.

Additionally, both policy types provide a cash value account and they are both considered permanent life insurance policies, which will last for your entire lifetime.

A whole life insurance policy will offer several guarantees. These include guaranteed premiums, guaranteed death benefit, and guaranteed accumulated cash value. A whole life policy will tend to have a much more rigid premium payment in exchange for these guarantees. Whole life policies do not have surrender charges, so the cash value of your policy will also be the cash surrender value of your policy.

Whole life policies tend to come from mutual insurance companies. These are insurance companies owned by their policyholders. Mutual insurers' financial obligations are to these policyholders.

Universal life insurance gives up most of the guarantees offered by a whole life policy to provide higher potential non-guaranteed features. A universal life policy also offers considerable flexibility of policy premiums. Surrender charges are a common feature found on universal life insurance so this means the policy's cash value is not necessarily the cash surrender value.

There are several different types of universal life policies. They include variable universal life insurance, indexed universal life, and “current assumption” universal life. Variable life insurance puts the policy's cash value in an investment account where it rises and falls with the performance of the investment. Indexed UL insurance pays an interest rate that tracks a stock market index. Current assumption products set an annual interest rate payable on the policy's cash value.

How do you Access the Cash Value?

The major draw to a cash value insurance policy is its cash accumulation feature. Many people like to use this type of life insurance as a savings account. The appeal is the much higher effective interest rate on their savings versus a traditional money market or savings account. The cash in these policies grows at a rate more similar to bonds, but also provides considerably better liquidity.

The way you access the cash value in these policies does differ a bit depending on the type of cash value life insurance you own.

You can access the cash value through either partial withdrawals or a loan. UL policies allow partial withdrawals of all policy values whereas whole life policies only permit partial withdrawals of non-guaranteed cash values.

Loans work similarly across both life insurance types. Both accumulate interest, which you can choose to pay out of pocket or add to the outstanding loan balance. Loans enjoy special tax advantages that prevent them from creating an income tax liability–this is true for both product types.

You can also use your whole life insurance cash value for the three nonforfeiture benefits: extended term insurance, reduce paid-up, or surrender for cash value.

Universal life policies allow only the surrender for cash value nonforfeiture benefit.

What Insurance Companies Issue These Types of Policies?

Mutual insurance companies often issue whole life policies. But whole life can also come from other forms of insurance companies. Additionally, fraternal companies often issue whole life policies. Fraternals are not technically insurance companies, but they operate under very similar protocols.

Universal life insurance policies come from a much broader mix of life insurance companies. Some mutuals do offer UL policies, but it's more common to see this type of cash value policy from a stock life insurance company.

It's important to understand that not all life insurers issue every type of life insurance policy. So while some companies might issue one or the other, you shouldn't just expect that they will offer both types.

Do I have to Buy from an Agent?

If you are seeking a cash value policy, you will have to buy from an agent/broker. While you can buy a term life insurance policy from a number of different places that don't use insurance agents, cash value policies are different.

The complexity of these policies makes it very difficult to offer them in an automated fashion as some companies do with a term life policy. The insurance premiums you pay for the policy's death benefit can vary greatly depending on several factors. This includes various policy features and any chosen rider.

In addition, cash value policies can create a tax penalty situation due to the Modified Endowment Contract (MEC) limitations imposed on them by the IRS. Having a knowledgeable life insurance agent available to help guide you through this could save you from a significant hassle.

Will I Earn Dividends?

If you buy whole life insurance you might earn a dividend. Life insurers do not guarantee the payment of dividends, and you'll have to ensure that your whole life policy is “participating” in order to earn them.

UL style policies do not pay dividends. Instead, they pay interest that can fluctuate from year to year. Or, in the case of variable life insurance, cash value will change based on the value of the investments used in the policy.

What Sort of Rate of Return will I Get?

Your rate of return on a cash value policy will depend on several factors. The chief variables that influence the rate of return are the life insurance premium you pay relative to the policy's death benefit. Your gender may play a small role in most states, women tend to achieve a slightly better return at the same age as they enjoy moderately lower insurance costs.

The return on these life insurance policies will track the return achieved by the portfolios managed at the life insurance company–also known as the General Account. You should reasonably expect an annualized return over your lifetime around 4 to 4.5%.