Podcast: Play in new window | Download

In the interest of building newer and sexier ways to lure you into buying life insurance, agents and marketing organizations think it would be super nifty if you harnessed the extra buying power of a bank's money to make the policy you can buy even bigger! The idea looks something like this, buying more life insurance provides you with even more cash value. So if you borrow money from a bank and use that money to buy an even bigger policy you can power up your savings plan with an even larger pot-o-money with OPM–other people's money.

This isn't a particularly new concept. Premium financing originated decades ago and a select group of wealthy people used it as a way to buy life insurance–for a discount–they needed to pay transfer taxes. But as Congress and several states cut back on taxes levied upon one's death, the sales arm of the life insurance industry needed new ways to keep selling life insurance, so they decided they'd take leveraging cash-focused life insurance purchases out for a spin.

This led to fanciful presentations promising big results for those smart enough and special enough to borrow lots of money and plan their retirement like the Rockefellers. We expressed doubt on the viability of such a plan way back in 2015. But anytime there is money to be made–and there's lots of it to be made here–details like the huge risks you take on when borrowing money to buy more life insurance than you could normally afford are minor annoyances and we must bury them under a deluge of meaningless facts and figures used to obfuscate net takeaway.

I Always Wanted Premium Financing to Work

I believe some people think I hate premium financing. That I want it to die in a fiery calamity rivaled only by the Hindenberg. Not true. I actually covet unique solutions to problems and I welcome out-of-the-box thinking. I am the guy who once said, “I want to start a blog talking about how people can tactically accumulate personal wealth with life insurance policies.”

There's also money to be made with premium financing. A lot of money. We'll get more into just how much a little later in this article.

I've tried for years to make premium financing work in a number of different scenarios. For most of them…it just doesn't. That's not because there is no situation ever that warrants the strategy. It's because there just aren't that many situations that warrant premium financing as the answer to a current problem. That doesn't make it good, evil, or anything in between. It's just the reality.

More People Looking to Sell it than there are People Eligible to Buy it

Sadly, we find ourselves in a situation where there are more insurance agents looking to sell a premium financed case than there are people who actually fit the fact pattern that qualify them for such a plan. Premium-financed life insurance candidates are, I assure you, a very rare breed. And finding someone in such a situation for whom you can solve a problem with the strategy will net you a handsome payday. I'm not begrudging the fortune an agent can obtain through premium financing when it makes sense to finance the premiums. There's A LOT of work involved, and I'll argue quite strongly that said agent will earn every last dollar he/she receives.

But anytime there are huge payoffs there is an incentive to arduously search for fact patterns that fit the bill for premium financing–and maybe just maybe relax the guidelines on who exactly fits perfectly and who doesn't.

When upper-middle-class professionals with a very low seven-figure portfolio balance–or less–start popping up on various personal finance forums asking for guidance on financing premiums for life insurance because their “financial advisor” just suggested it to them we know someone made it past the guard tower.

Stress Testing the Idea

I decided, yet again, to give premium financing in its newly taken on fashion a sixth at winning me over. I gathered some information on a typical situation to see what it might provide and how that would compare to what other options might exist to someone in the same situation. The details are:

Male, age 45 will borrow $150,000 per year for 10 years and use that money to pay life insurance premiums. He will pay the debt servicing costs of the bank loan. This means he'll pay, out-of-pocket, interest on the loan, and any other fees assessed by the bank. I used the insurance company's own software to estimate interest as well as bank lending fees–they should know better than I what is reasonable and customary.

Also, to give life insurance the best possible head start for premium financing, I selected an indexed universal life insurance policy with the highest possible indexing credit available.

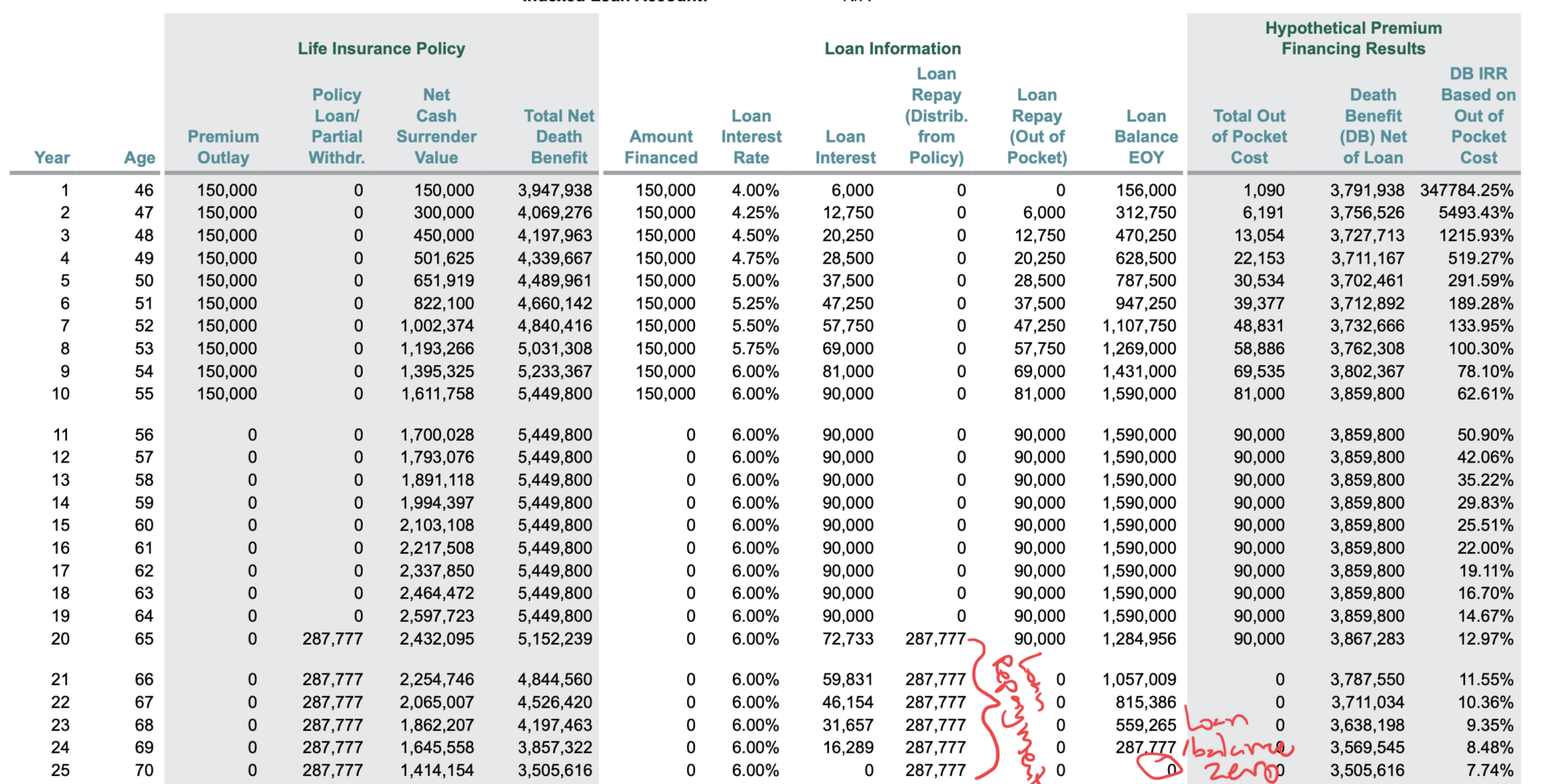

I set up the scenario for the insured/borrower to borrow for 10 years and then designed the life insurance policy to require no premiums beginning in year 11. I originally wanted the life insurance policy to pay off the bank at year 11 but it turns out that would destroy the life insurance policy so I settled on allowing the loan to exist for another 10 years before the life insurance policy began paying the bank off. I gave the insurance policy five years to accomplish this goal–in other words, the life insurance policy begins repaying the bank loan in year 20 and finishes paying off the bank at the end of year 25, here's a snapshot of the ledger:

The year immediately following the payoff of the bank, this policyholder now owns the life insurance policy with no bank encumbrance. But he does have an outstanding policy loan used to repay the bank. This is a pretty typical scenario used for premium financing, and the idea is that the loan will never grow to a point where it threatens a policy lapse. This ledger confirms this–assuming the assumptions hold true and that this policy continues to earn the 6.18% annual index credit and the insurer never increases the expenses of the policy.

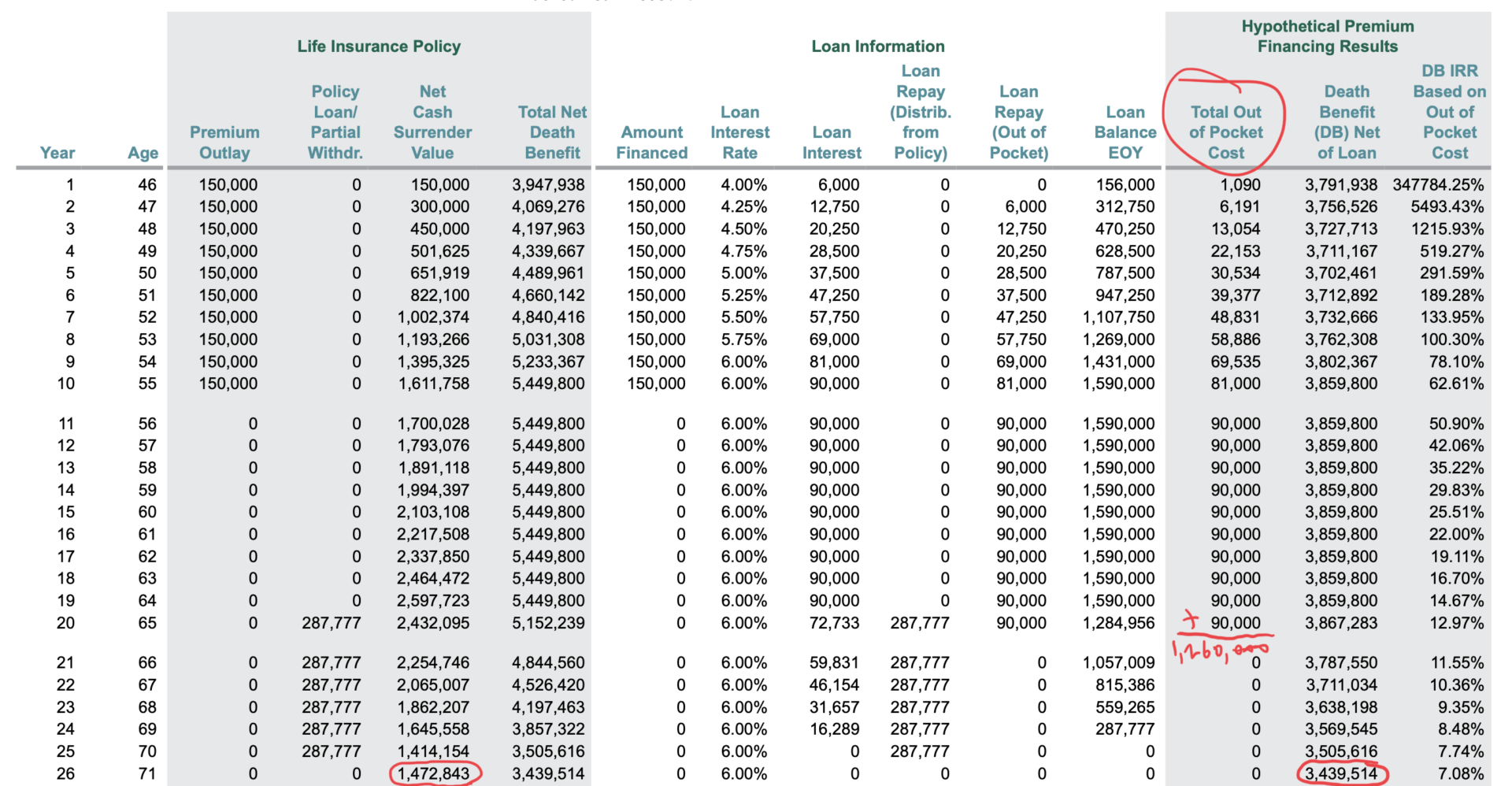

The out-of-pocket cost of this policy was $1,260,000. This expense is the cost of servicing the debt with the bank, and you can see the breakdown of this in this screenshot:

Notice that the policyholder has $1,472,843 in cash value and a death benefit of $3,439,514. These are net figures so they assume the loan currently outstanding on the policy gets repaid. These figures are what is left over after loan repayment.

So the policyholder borrowed almost $1.6 million dollars and paid out $1,260,000 to arrive at slightly less than $1.5 million in cash value and a little below $3.5 million in death benefit. His cost basis is gone, as he exhausted that repaying the original loan–a total of $1,726,662 in loan repayments taken from the policy.

There is a gain achieved on cash value, but it's rather tiny. I calculate the compound growth rate using the out-of-pocket cost and the net cash value in year 26 at 1.06%…how exciting…

So why else could someone look to use life insurance to build wealth do? Glad you asked.

An Alternative Approach to Financing the Premium

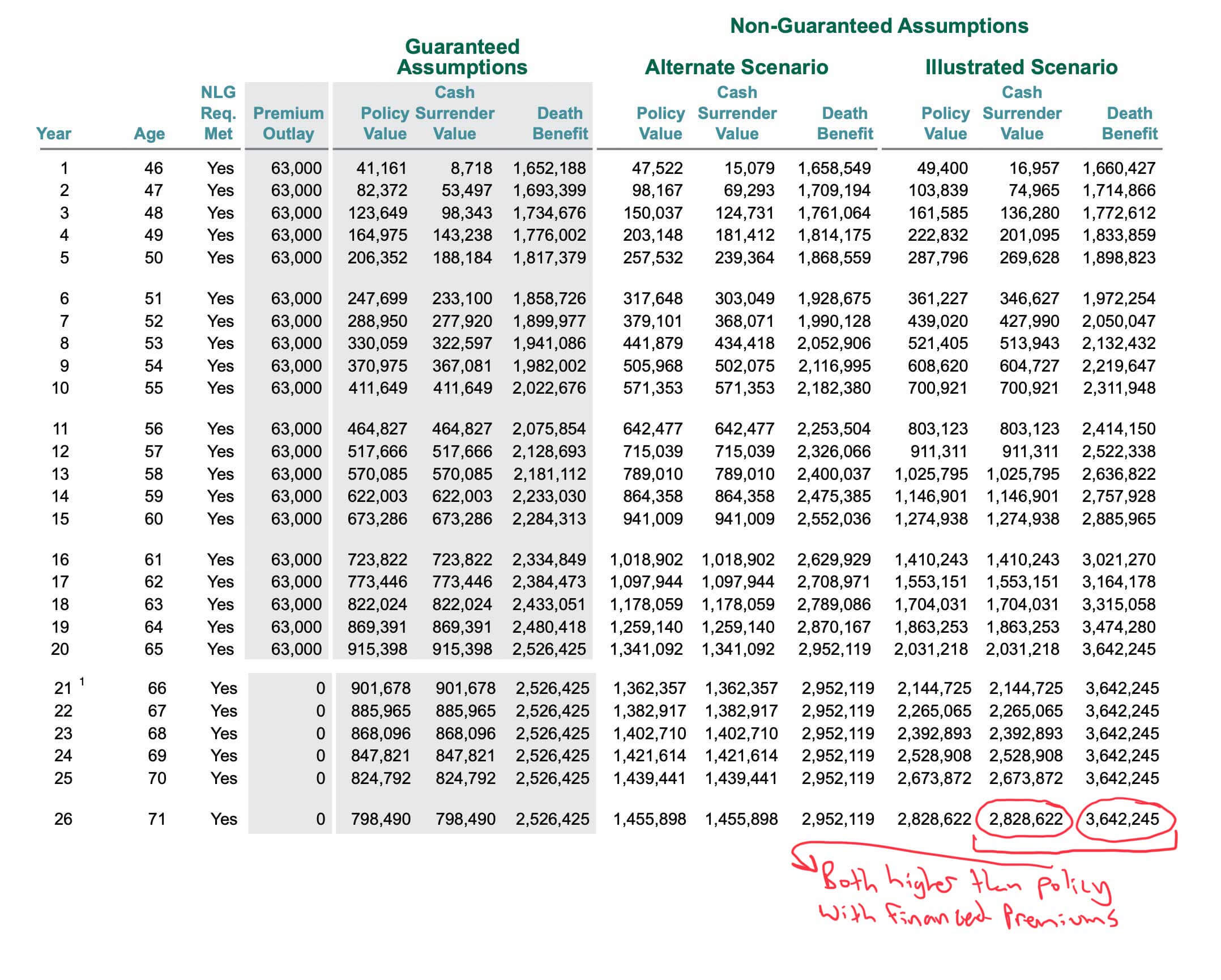

The individual in this example is going to pay out $1,260,000–that's inescapable. So let's level that over the same period and just buy regular life insurance–sans the fancy leverage part–and see what happens. This creates the following policy:

Notice that we start out with a much lower death benefit and a lower cash value amount–we are, after all, paying a lower premium. But by the time we get to the year the financed policy pays off the bank, we have $1,355,779 more in cash value and $202,731 more in death benefit. Financing the premiums fails miserably against the non-financed scenario to create additional wealth through cash value and it even fails to come out on top with death benefit–an area that is supposed to be its strength.

Notice that we start out with a much lower death benefit and a lower cash value amount–we are, after all, paying a lower premium. But by the time we get to the year the financed policy pays off the bank, we have $1,355,779 more in cash value and $202,731 more in death benefit. Financing the premiums fails miserably against the non-financed scenario to create additional wealth through cash value and it even fails to come out on top with death benefit–an area that is supposed to be its strength.

But wait…there's more!

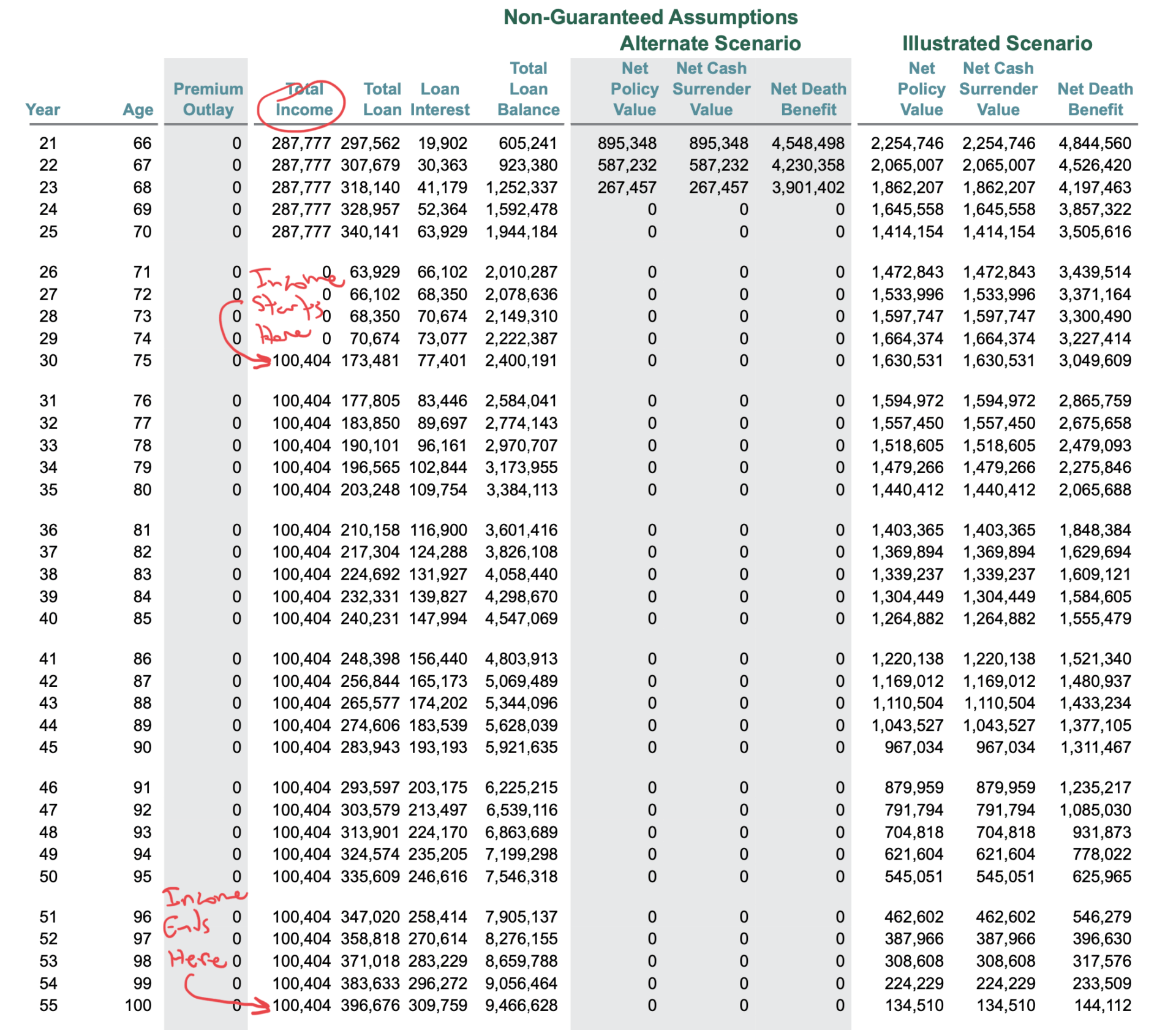

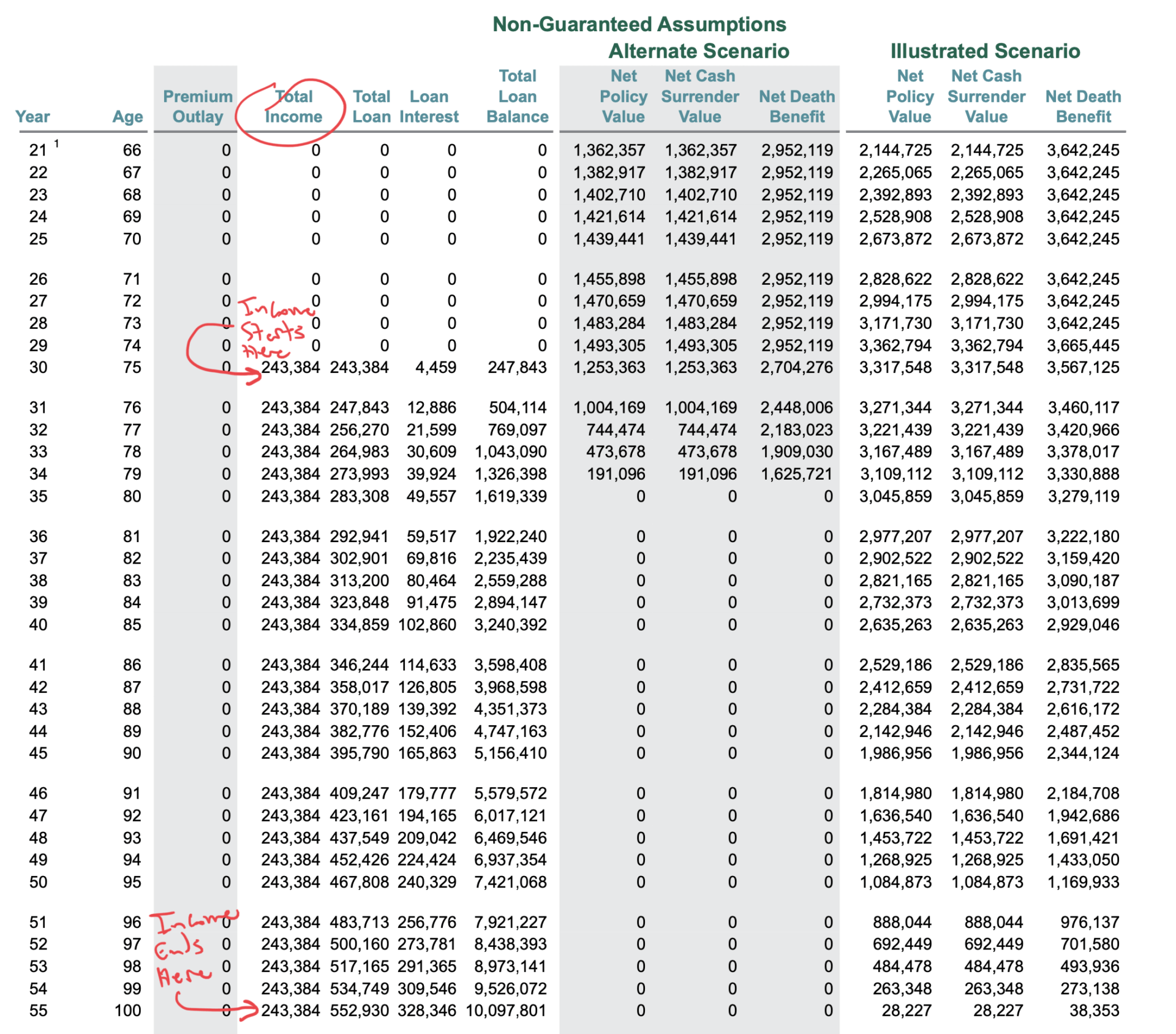

Since a lot of agents pitch this idea as a way to supercharge retirement preparedness, I figured it only fair to look at how these two scenarios stack up against each other regarding retirement income. So I decided to solve the maximum income scenario beginning age 75 through age 100. Here are the ledgers depicting that scenario:

Premium Financed Income Scenario

Non-Financed Income Scenario

You are reading this correctly. The financed version provides $100,404 annually while the non-financed version provides $243,384 annually. That's a $142,980 raise when you don't bother borrowing from the bank. Keep in mind, the out-of-pocket is the same in both scenarios. The underlying life insurance assumptions are the same in both scenarios. Same company, same annual index credit, same everything else except the financing part. Buying more life insurance doesn't create more benefit…well at least not for the policyholder.

There's Money to be Made

I mentioned earlier that there's a serious financial incentive for premium financing. Commissions? Oh yes, commissions. But first, let's talk about the incentives for the bank. If you haven't already done so, take a moment to tally up all the income the bank generates in this scenario. The interest it collects while lending out “OPM” to the policyholder who thinks he's orchestrated a great ruse to enrich himself with “OPM.” The bank's haul totals $1,486,662. Not bad. And all the while the bank had a 100% collateralized asset–it's a non-negotiable stipulation of premium financing.

The commissions earned by the agent. They aren't half bad either.

First, let's talk about the commissions earned by the non-financed policy. I calculate those to be around $27,000. Certainly, nothing to sneeze at. But the financed version of this is all of that and then some. I calculate the premium financed commissions to be $64,685–also known as more than double the other option. Boy howdy wouldn't that be a nice pay raise.

You see, I understand the financial payoff possible with premium financing. It's why I've spent countless hours over the past half-decade trying to come up with a scenario that reasonably made it make sense. I continue to fail at accomplishing this goal. So I don't attack the idea because I have some weird personal beef with it. I'd be more than happy to benefit from it financially speaking. But I can't in good conscience make recommendations that next millions less in lifetime value, just to make several 10 thousand dollars more on a client. Not everyone agrees with me on this.

Thanks – I assume the life illustrations used indexed loans with 50 bp leverage based on AG49a limits. A good related article would be to look at when the policy loan balance becomes a high percentage of the account value (such as 80% to 99%). If there is a 0% credit for a year or two, you would not only have to stop taking income; loan repayments would be needed to avoid a lapse with a loan balance and a whopping tax and no cash value to cover the tax.

The last example above has 28k net cash value with over a 10m loan at age 100. Not likely for the policy to go that long, but similar years where loan repayments would be needed often occur from the early 80’s on. The policy would need careful management and separate liquidity to keep the loan leverage going.

The loan used for this was a fixed loan; not an indexed loan.