Blended whole life is a concept we really like. We maintain that it’s the way to purchase whole life insurance if cash accumulation is your primary goal.

Anyone who has learned that you can use whole life insurance as an asset and income tool should probably also take a look at a blended policy.

If you’ve been shown a standard whole life policy (i.e., no paid-up additions and no blending used to maximize paid-up additions), we invite you to challenge the performance of that policy against what can be done with the advantages of this truly unique blended design.

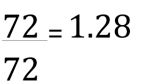

Perhaps you’d first like to see some proof to back up our claims that this blending business is truly beneficial?