This one has been around for a while but is picking up steam recently, are they going to start taxing life insurance?

This one has been around for a while but is picking up steam recently, are they going to start taxing life insurance?

Given the fiscal cliff and the we have an answer no wait no we don't whip saw that has been taking place in Washington, it's no surprise that every fear monger out there has taken a moment to jump on this train. Let's not forget NAIFA and IFA-PAC's constant need to recruit and open up members' wallets by shrilling this one at every luncheon and on every newsletter (they're coming and their coming after us!). We can't always hate them though, props of course, for their work on 151a.

But whether we like it or not we're in a pretty serious financial situation and that means we have to take all theories about how Congress will rob Peter to pay Paul. So, let's discuss why or why not Congress will drill deeper into your pockets and start raiding your life insurance policy for tax revenue.

Low Hanging Fruit?

Most of the chicken littles hawking this idea tell us that life insurance is low hanging fruit. It was targeted once before, and we're kidding ourselves if we don't think it's not in their corss-hairs again.

So, there's two approaches Congress could theoretically take regarding this:

- Tax Cash Values either removing the tax deferral or removing the tax free loan provision or both

- Tax Death Benefit

- Taking everything

So, let's dive through each example.

Bye Bye Tax Deferred and/or Tax Free Income

This one is arguably the big one. Removing the tax deferred treatment enjoyed by cash value life insurance contracts (or their annuity counterparts) and/or removing the ability to access the money from a cash value life insurance contract tax free through a to basis withdrawal and then policy loans would render the products' common use as a wealth accumulation/retirement supplement play would virtually inert. I'm not so sure I'm in complete agreement (treasuries have underperformed well designed cash value life insurance for years and they are fully taxable) but there's certainly a big benefit out the window of this scenario rears its ugly head.

This of course could take a few different forms. On the one hand we could see a loss of the tax deferred status life insurance has. Or we could see the elimination of tax free policy loans. Of course, one would strongly detest the notion that a loan be taxable as it's merely the pledging of collateral to a lending institution (in this case the insurance company) to acquire funds. This however is exactly what took place under TAMRA with Modified Endowment Contracts.

There is potentially a way around taxable loans, at least if taxable when issued by an insurance company. Banks love to issue loans backed by life insurance policies (insurance contracts are stable, and the bank can force its position as a irrevocable beneficiary to the contract to ensure it gets paid). This would theoretically wipe out the problem and bring loans back to tax free status. It also introduces a whole host of fees and headaches thanks to the bank lending process.

Taxable Death Benefit

This one perhaps more bite and more appeal to a worried Congress' attempts to make quick cash a la tax revenue. The need for life insurance from an income replacement stand point is pretty well established and understood. The question I have is, will people buy more or less insurance as a result? I suppose the same amount could be a fair third option.

More

Economic theory would suggest more insofar as the individual's marginal rate of utility had a smaller derivative for the lost benefit of what's given up v.s. the derivative for lost benefit in a declining check going to his or her loved ones et. al.

This means the ones that most appreciate what life insurance does would be likely to buy more to ensure that the originally intended amount goes to those who need it should the individual pass away. Actuarially speaking, we know people have a higher propensity to spend on life insurance when there is some risk that would presuppose a higher likelihood of death. So it can at least be said that the life insurance industry's best (perhaps most favorite) customers would likely buy more.

Less or the Same

Theoretically people who place a lower value on life insurance coverage vs. other things they can bring to their could buy less if the death benefit is taxable. The case could also be made that they would do nothing. As is the traditional case concerning economic theory, taxes generally curb consumption.

In fact a scenario where people buy more life insurance in the face of a taxable death benefit sort of fits the definition of a Giffen Good. And as Behavior Economics has taught us several times, the rigid modeling Modern Economic Theory uses to predict behavior tends to make too strong an assumption concerning the neutrality people have towards such events. One need look no further than Daniel Kahneman and Amos Tversky (two famous psychologists not economists) to see some of the greatest contributions to a re-write on modern economic theory as its applied to individual behavior (especially surrounding loss).

Based on this, I think the case could be strongly made that an introduction of taxable death benefit could result in a strong decline in life insurance purchases. It may appear counter intuitive, but there's a lot of empirical evidence in other circumstances to back this up.

Will it Happen?

So the million billion dollar question is this very question. Tax policy can be a bitch of a policy process to predict, and the big reason behind this is the number of derivatives that must be considered to adequately measure (but say nothing about that, simply begin to predict) the overall impact. For years people derided Art Laffer for his predictions regarding income tax policy, but Art can point to the increased tax revenues that came about following the “Bush Tax Cuts” to give credibility to the fundamentals of his theory.

Because I don't expect anyone who reads the Insurance Pro Blog to be a tax policy expert, the quit and dirty lesson looks like this. Simply increasing taxes never yields a dollar for dollar increase in tax revenues. Instead governments generally realize some smaller number due to changed behavior that avoids taxes or ceases certain activity to product the taxable event (i.e. jobs that net incomes that place someone in the highest marginal income tax bracket don't tend to be the easiest jobs in the world; if you increase someone's marginal income tax they may decide to work in some different capacity because the marginal benefit derived from the income no longer exceeds the marginal cost of the tax vis-a-vis what it takes to earn that income).

That's an overly simplistic example, so let's dive into the some insights regarding the insurance industry to help answer whether or not we believe taxing life insurance in any of the forms above is a good idea from a tax revenue increase point of view.

Declines in Sales, the most likely Event

Regardless to the method (taxing cash value in any fashion) and/or taxing death benefit, the case could reasonably be made that there would be a decline in insurance sales. The life insurance industry itself contributes about $900 billion annually to the U.S. GDP, or about 6% and it employs some 340,000 workers. That's more than automotive manufacturing (an old sacred cow) by a lot.

6% of GDP is a small number relatively speaking, but it's a relatively large number when it comes to the amount contributed to the entire economy. But there's something more. Something a lot of people tend to forget.

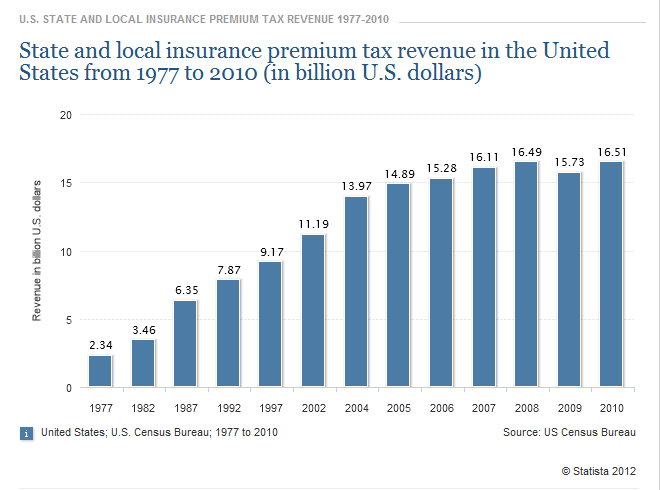

There's a tax that the insurance industry pays to which most people remain completely oblivious. It's known as the premium tax, and it's collected by state governments. How large is this tax? $16.5 billion dollars in 2010.

For state government this is not a tiny number, and placing this revenue in peril is not a move most state governments are likely to go along with. The premium tax is collected on all premiums collected by an insurance company. In truth, you the consumer pay it, as it's factored into the expense structure (you'll see disclosure of this if you look hard enough at policy illustrations). But just as the sales tax is paid by the consumer but collected and handled by the seller in most cases, the premium tax follows a similar path.

Political Muscle

Given the size of the life insurance industry, and it's deep roots to other pockets, I don't think we'll see much of a reformation regarding the taxable status of life insurance, even if the White House and Congress drive us over he fiscal cliff. The draw back is substantial and the industry generates a good supply of tax revenue under it's current form.

The taxable accounts that would be created by changing the rules for these products pales in comparison to other products that could be on the table, and could generate a lot more tax revenue.

So while the crazy fiscal cliff talks may throw a lot of ideas on the table, I don't think taxing life insurance is one that will put he breaks on the bus as it draws nearer to the cliff, and I think Congress realizes this.