Podcast: Play in new window | Download

Indexed universal life insurance reviews are in no short supply all throughout financial media as well as the internet. Recently, a review came from a source that most of us would consider authoritative on the subject. In a mini white paper titled A Critical Review of Indexed Universal Life, Scott Witt rolled out a multi-point takedown assessment on IUL.

Witt is formally trained as an actuary and presently works as a fee-only insurance advisor through his Witt Actuarial Services company. He holds both an FSA and MAAA and worked in an actuarial capacity at Northwestern Mutual prior to launching his fee-only service.

Given his qualifications and experience, we certainly view his take on indexed universal life insurance seriously. In fact, we received numerous emails over the past week or so from insurance professionals who wanted to know our thoughts on his rather scathing review of indexed universal life.

I read it carefully and found it…surprisingly disappointing. Let me explain.

Our Biases

First, in the interest of full disclosure, I find it necessary to point out that I actively sell indexed universal life insurance. While the business we run selling life insurance is overwhelmingly whole life insurance, we maintain the position that universal life insurance, and more specifically indexed universal life insurance, provides unique benefits from which certain fact patterns can benefit greatly.

But in the spirit of full disclosure, you should understand that I am compensated for the sale of and I regularly receive compensation from past sales of indexed universal life insurance (as well as other forms of life insurance, most notably whole life insurance).

Too Long Didn't Read

I intend to address numerous points Witt made in his critical review, so for those interested, I invite you to read on. For those with less time on their hands, my biggest disappointment with the review is that it relied heavily on hearsay and had a touch too much sensationalism.

The review is shockingly devoid of data to support the claims. To be clear, there is a stunningly large number of misinformed agents and marketing professionals who shoot first and ask questions later when it comes to the strengths and weaknesses (they do exist) of IUL. Witt's critical review is warranted for those reasons but I'd like to see clear evidence of the points made.

For those who want to read the whitepaper in full:

[gview file=”https://theinsuranceproblog.com/wp-content/uploads/2020/04/IUL-Witt-0420.pdf”]

Part 1: Stock Market Returns, IUL Cap Rates, Zero is your Hero and Timing

The review begins by setting up a common sales pitch for indexed universal life insurance. It's a product that gives purchasers access to market returns without subjecting them to the risk of market losses. This is swiftly met with the reality that IUL policies have cap rates and that these products follow the value index, which excludes dividends.

The piece goes on to say that the average annual return of the S&P 500 (the most common index followed among IUL policies) from 1955 to 2019 is 10.4% when including dividends but only 7.2% when we remove the benefit of dividends. What's not included is that to accomplish this 10.4% return with dividends one must reinvest dividends, but this is commonly the insinuation when we reference investment dividends included.

There's no elaboration on if this 10.4% return is an average return (I suspect it is) or if it's a compound annual growth rate. The paper references this 10.4% return against the 7.2% when we exclude dividends and says:

Consumers (and agents) are inclined to think of stock returns as averaging 10% historically; doing so overvalues the upside potential of IUL policies as “expected” returns for the index should be far lower, even if future performance doesn't stray from the past.

There's no source for the suggestion that consumers and agents believe the stock returns will average 10%. It's not my understanding that they will.

I'm also not aware of many people who believe they will. At one time I held a securities license and used to talk quite extensively with people about investing in the market and what they anticipated as a rate of return. 10% would be the absolute top of the distribution of answers.

That experience is anecdotal, I do realize. But I also failed to uncover any data that clearly tells me there is a consensus that stock returns are 10% on average. I'm dubious on a consensus regarding how this 10% return might affect indexed universal life returns.

I do know, however, of a few insurance marketers who have, in their attempts to sell IUL, commented that they conservatively used 7% (or something close to that) as the basis for their projections. They then go on to suggest that historically the market did better (again without supporting data) and then suggested that their projections were likely wrong, but wrong in a good way.

That's not a damning attribute of indexed universal life insurance. It's a terrible sales tactic that should bring shame to the conscience of any agent who uses it.

What's more, a consumer's misunderstanding of a product–be it life insurance or anything else–is not good enough reason on its own to declare something bad.

The speculation that a client might think IUL will perform better assumes quite a lot about what the typical life insurance consumer understands about stock market averages. Witt might be right, but there's no evidence to back it up.

Then there's a point about cap rates. He declares that cap rates can go down. I can confirm that they do go down. Witt incorrectly states that they can go down annually. I can confirm that they can go down much more frequently than that–and they have.

But my problem here is the insinuation that cap rate reductions happen for the lol's at the amusement of the C-Suite. I don't have the sense that cap rate reductions are arbitrary.

Reductions happen because they have to when the constraints that create cap rates (more on that later) require it. There is no evidence offered to substantiate that reductions occur trivially. There is also no mention that cap rates can go up when conditions improve, which is something that has occurred over the past 10 years.

Next, the paper notes a common point…

While indexed universal life does protect against loss with its “floor” feature, a zero year can still result in a net loss due to the deduction of insurance expenses.

Unfortunately, the paper chooses to sensationalize this point a bit when suggesting that it will always result in a loss due to these expenses. Taken in a very specific context for the precise example, I suppose we can argue the point is valid.

But it's a myopic depiction of indexed universal life insurance and completely discounts some very critical nuance most contracts provide policyholders. These nuanced features are:

- The fact that not all index options have a zero floor. Any floor above zero might provide the interest earnings necessary to cover insurance expenses

- Several products offer the policyholder to established index accounts in more than one broad index. So if the S&P 500 is down, that doesn't necessarily mean a foreign exchange (for example) is down.

- All IUL products that I'm aware of include a fixed account option where the policyholder can allocate all or some of his/her money. This creates an effective floor that is higher than zero (or whatever the index floor is) and could overcome insurance expenses in a down market year.

There is no mention of any of these features here or elsewhere in the review.

Lastly in this section, the paper notes that the start and end date can change the results of an index credit rate dramatically. He uses an example that compares the stark difference between an IUL policy anniversary date of March 4th versus March 11th.

It notes that a one-year point-to-point S&P500 index that runs March 3, 2019, to March 3, 2020, would be up 12.1%. Alternatively, the same IUL policy with the same index option that runs March 11, 2019, to March 11, 2020, would be down 1.5%.

The policy owner who bought on March 3rd is understandably happier than the owner who bought on March 11th. But that's a single year result. Witt does note that the March 11th buyer is in a much better position for a good one year growth period 2020 to 2021 because of the starting position.

If anyone looking to buy IUL is solely focused on the result of the next 12 months, he or she isn't a candidate for indexed universal life. Yes, the results can vary in any given year. But when we take all of the years spanning a few decades, these variances should mostly go away.

To test this theory I took an older IUL policy I have on the books where the premium payment occurs monthly. I specifically looked at this policy because the monthly beginning and ending segments give me data points to compare the string of 12-month segments for multiple years. For example, I can compare if the Februaries Perform better or worse than the Septembers. I went back six years, and here are the results:

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | Average | |

| Mar | 12 | 10.77 | 2 | 11.25 | 11 | 2 | 8.17 |

| Apr | 12 | 11.7 | 2 | 11.25 | 10.86 | 10 | 9.64 |

| May | 12 | 11.75 | 2 | 11.25 | 11 | 6.41 | 9.07 |

| Jun | 12 | 6.6 | 3 | 11 | 11 | 3.76 | 7.89 |

| Jul | 11.25 | 3.98 | 5.19 | 11 | 11 | 7.02 | 8.24 |

| Aug | 11.25 | 8.64 | 3.69 | 11 | 11 | 2 | 7.93 |

| Sep | 11.25 | 2 | 10.57 | 11 | 11 | 2.28 | 8.02 |

| Oct | 11.25 | 4.5 | 8.38 | 11 | 11 | 3.52 | 8.28 |

| Nov | 11.75 | 2 | 5.07 | 11 | 7.6 | 2 | 6.57 |

| Dec | 11.75 | 2 | 11.35 | 11 | 2 | 9.5 | 7.93 |

| Jan | 11.75 | 2 | 11.25 | 11 | 2 | 9.5 | 7.92 |

| Feb | 11.75 | 2 | 11.25 | 11 | 3.45 | 9.5 | 8.16 |

Notice that there are certain months in a given year that perform better and worse than others. In 2015, for example, someone who bought in May of 2014 was obviously happier than someone who bought in September of 2014. But if we look a the average for all the Mays, all the Septembers, etc, we see that the results begin to converge. This is precisely my point. Yes, month-to-month variations do exist, but over longer periods, this difference fades.

There is one interesting observation here. November. It's lower than all of the other months, but it is not outside two standard deviations from the mean of the dataset. So it's highly unlikely that we discovered November is the worst month to buy IUL, and instead just a coincidence of this dataset.

Also note one more thing, index earnings in 2014, specifically the month of July through February. In July, August, September, and October, the index earning was 11.25%. In November, December, January, and February the index earning was 11.75%. The market was up more than the index earning in all eight months–the policy reached its cap. The reason that November through February is higher is that the cap rate increased for these months. Proof that cap rates do change and that the change isn't always a reduction.

Part 2: Do IUL Policies Provide an Upgrade Over a Good Whole Life Policy?

This section starts by asking the above question and quickly casts doubt on it. He notes that he does not believe a compelling case can be made for IUL's superiority over whole life, especially from a highly rated mutual insurer issuing a whole life policy “optimized to reduce agent compensation and maximize policy efficiency” (hold on to this thought for later).

The immediate explanation of why this is the case has nothing to do with a quantitative fact about the differences between indexed universal life and whole life insurance. Instead, there's an overview of how the hedging investment strategy works to produce indexed returns. I'm not sure how this explains the advantage of whole life insurance compared to indexed universal life insurance?

Massive Early Expenses

Witt then notes that he can say with absolute certainty that the early expenses on an IUL policy are massive. He notes that they are:

…typically the most of any insurance policy I evaluate.

Now one of the reasons I admire actuaries is their love of data. You'd assume that at this point we'd see data comparing these massive early expenses of IUL policies to all the other types of life insurance.

That's what you'd think would happen…

…But sadly you'd be wrong. The statement is made on the paper moves quickly on to an entirely unrelated point that has to be the most ill-conceived out of left field attack he makes in the entire review:

One very concerning observation is that its typical for the very same company that offers a 9% cap rate on an IUL policy to offer a 5% cap rate on an otherwise identical indexed annuity. The annuity doesn't have as many moving pieces, and therefore the crediting methodology is more straightforward and transparent–and without fail that leads to a dramatically lower cap rate.

I don't have any problem with annuities. I don't personally sell a whole lot of them, but I think they have a great deal of value to offer many people. But I've never held the belief that indexed annuities were more straightforward than indexed universal life insurance. And I can speak from first-hand experience when I say that index options on most indexed annuities are anything but straightforward.

Further, even if the point was valid (it's not) there's no evidence that a higher cap rate on an IUL due to complexity is bad versus a lower cap rate on an annuity because it's simpler.

Heavy Lapse Supported Pricing

The next point could be one of the most damning against indexed universal life insurance. Witt points out that heavy acquisition expense assumptions could indicate a high level of lapse supported pricing dependency. He explains the general idea behind lapse supported pricing and notes that we'd suspect this when we see low initial cash values followed by high long term cash values.

It would be great to see data to prove this point, then it would be clear that there is or is not evidence of heavy lapse supported pricing. That would have made for a real nail in the coffin moment. I really wish he had taken the time to do it.

Options Pricing Affecting Cap Rates

The next point concerns cap rates and how the change in options pricing will likely cause cap rates to go down. Earlier Witt walked through how insurers use call options to execute the hedging investment strategy that creates indexed insurance products. He notes here that higher options prices due to recent market volatility will most likely put downward pressure on cap rates. I very much agree with this sentiment. I wish that he spent more time quantify options pricing changes.

Here the review could have used this point to tie back the to next couple of points concerning the assumed rate of return, but since that wasn't done, I'll do that for him.

What Exactly is the Assumed Rate?

Here we see evidence of potential IUL no, and good on Scott Witt for calling it out. He shares some data from an IUL policy he recently reviewed. The policy had a cap rate of 9.25% and assumed the maximum illustratable index crediting rate of 5.76% (this maximum is set by regulations that govern illustrations, most recently codified under Actuarial Guideline 49 or AG49). He goes on to note that the calculated IRR of the cash value in the policy at the insured's age 100 is 7.6%. This raises an interesting question.

How can a policy that assumes the cash value will grow by 5.76% per year (gross of expenses) produce a real net return on premiums paid of 7.6%? That should be mathematically impossible in any year. Unless, of course, the assumed indexing credit is higher than 5.76%.

But how can such a feat be accomplished if 5.76% is the maximum allowable assumption? The answer: bonus interest.

Many IUL policies now have bonuses that enhance returns. There is certainly debate over how these bonuses might cause an agent or marketer to unwittingly inflate the future expectations of an indexed universal life product. We discussed this issue recently, and we're certainly not alone in sounding the alarm.

But the mere existence of a bonus feature doesn't immediately cause reason for alarm. Witt brings up these bonuses and then sensationally declares that:

The illustration isn't worth the paper it is printed on.

His justification for this claim is never explored numerically beyond the spread between the 7.6% IRR and the 5.76% assumed index credit. I agree that on its face that difference appears extreme, but I'll also reserve immediate judgment because I feel we need to first explore the reasonableness of such a result from the company in question.

We have to break this topic into two pieces and then evaluate them independently. Now, for us not to declare ridiculousness on the behalf of the life insurance company, both pieces need to pass the test of reasonableness. Let me explain.

Test #1 concerns the reasonableness of the assumed index crediting rate. Based solely on the fact that it's the highest allowable rate per insurance illustration regulation, I'm already dubious. But since we do know the cap rate is 9.25%, and the floor is zero, we have what we need to evaluate the assumed index interest rate. Running these particular details through a Monte Carlo simulation using 25-year timelines and pulling randomized market returns from the past 66 years, I achieve a result of 5.76% or better about 59% of the time. While this is better than half the time, it's a good bit lower than I would feel comfortable assuming when projecting potential future policy values. In my personal evaluation, the company failed the test of reasonableness on this consideration.

Test #2 addresses the bonus. Cash value life insurance values are pretty tightly correlated to the return life insurers can achieve on assets. What I mean is that the cash in your life insurance policy is part of a larger asset pool held within the insurance company. It even has an official name. We call it, the General Account. The General Account comprises all the assets held on behalf of all policies that have some sort of accumulated value. The accumulation of values for these policies is tied to the return the insurer can achieve on the overall asset pool.

Now it is possible for some insurance contracts to having backing by assets that yield higher than others. For example, an insurer may still hold bonds purchased to support insurance contracts originated 20 years ago. In this case, the yield on those bonds is certainly higher than the yield on a similar bond purchased today, or even five years ago. But with any set of numbers, there is an average and that average is–to some degree–an anchor for all the results of all the insurance policy cash accumulations.

Knowing this, and knowing that indexed insurance products are one part bond and one part hedge created by a long call option collar, we'd reasonably assume that the accumulation of values inside an indexed universal life contract will be something similar to the rate of return on invested assets at the life insurance company. Given the hedging wrinkle, we can certainly permit some contingency for alpha generated by the investment strategy. This might look something like 100-ish basis points above the return on assets achieved in the General Account.

But it's probably foolish to believe that an insurer will consistently achieve a result above 200 basis points over the return achieved on all other assets. So, bonuses included with a net internal rate of return on future values probably shouldn't be a number much more than 100 to 200 (at an absolute maximum) basis points above the insurer's current return on assets. Is 7.6% outside this range? I don't know because we don't know specifically what insurance company was being reviewed.

At this point, you're probably noticing that both Scott Witt and I likely have the same opinion about this specific illustration. There's a good chance it's overstating future projections. And hopefully, you'll see that I've explained quantitatively why that is and I've done it without the need for abrasive commentary and sensationalism.

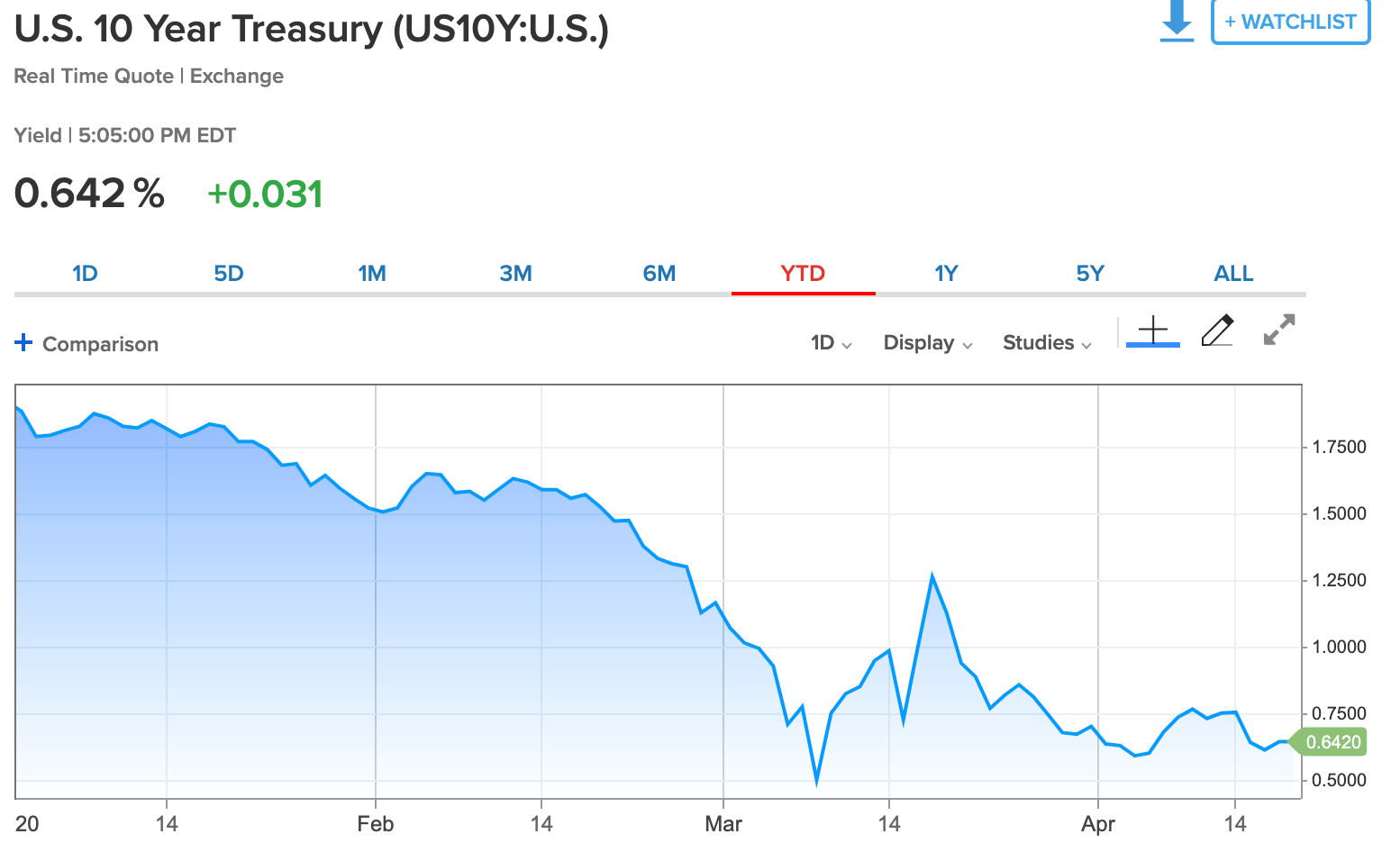

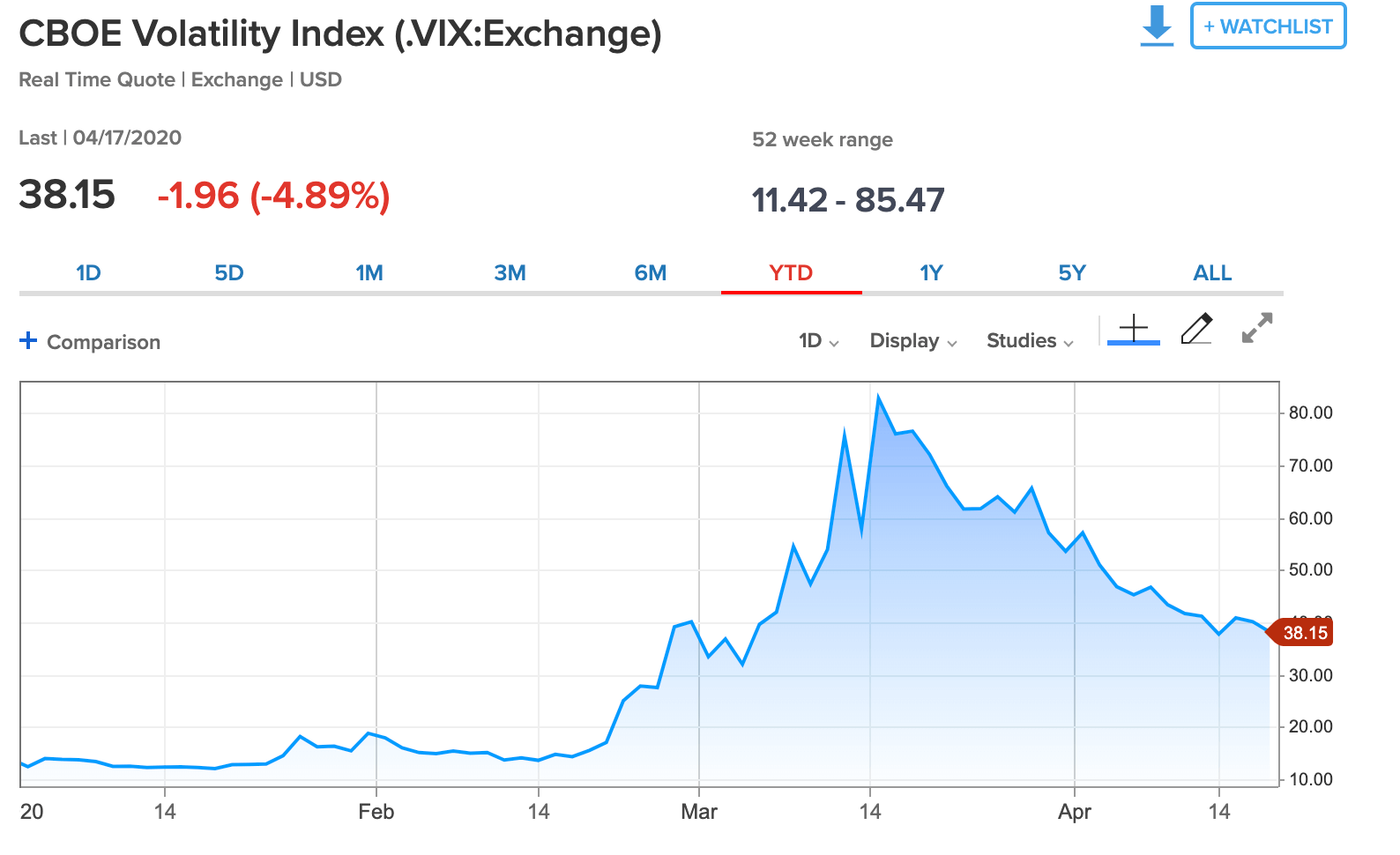

To really look closer at the likelihood of sustaining a 7.6% return on premiums paid, we need to revisit that cap rate vis-à-vis higher options price discussion. And we must introduce another consideration, bond yield. Currently, bond yields are lower, sharply lower due to Fed action to minimize negative economic consequences associated with COVID-19 spread. Market volatility shot up immensely over the past month but has settled quite considerably since then.

Here is a year-to-date chart for 10-year treasury yields for reference:

And here is a year-to-date chart of the VIX for reference:

These two charts show unfavorable trends for indexed insurance products, at least indexed products using broad U.S. stock market indices. The problem is they represent lower bond yields, which squeezes the budget insurers will have to buy hedging investments and they represent a potentially higher cost to acquire those hedging investments due to higher volatility.

When you have less money to spend on call options, and those call options become more expensive, the collar you can create with the traditional investment strategy employed by insurers to generate indexed returns shrinks. In other words, the cap rate goes down.

But here's the thing we don't know, and I assure you there is plenty of debate in opposite directions on this within the insurance community: how long does this current circumstance last? Some will simply decide, don't know; don't care, give me whole life insurance so I don't have to worry about it. I think that's a rather myopic approach to the discussion (I don't think whole life is immune to this reality, though it certainly isn't concerned with the effect of volatility on options pricing…unless your using the newer indexed paid-up additions/dividend options being rolled out). But if things recover within a year, then we will most certainly see an upward trend on cap rates as conditions for these collar strategies improve.

The important take away here is that we cannot allow a singular event to control our decision-making process. Just as I mentioned already that it doesn't matter if you own an IUL that closes on an index segment a week before my policy and end up with a better result this year. After several years, it's unlikely that you'll continue to beat my results based on your start and end date alone.

But there is a complexity to indexed products that consumers and agents should understand. And sadly, I worry that a majority do not understand these complexities. However, once understood, I think well-versed agents and well-informed consumers can implement indexed universal life as part of their wealth accumulation strategy with high levels of success. The complexity is not a reason to run away, it's a reason to dig in.

Lastly, on this gigantic point that probably could have been its very own blog post, Scott Witt references year 16 of his case-study illustration. This year, the policy assumes no premiums paid and no distributions. So it's just the expense deductions and then the index accumulation. Oddly, the policy achieves a (net of expenses) return on the cash value of 12.75%!

This is a very lofty number. I wish we could see the actual numbers to confirm. It's indicative of an inflated projection, and a point that begs for further exploration and certainly bolsters the point that projections are potentially inflated and fictitious.

Illustration Rules Unfairly Benefit Indexed Universal Life

Witt points out that illustration rules provide greater latitude in projecting IUL values versus other insurance products (namely whole life insurance). This is due to the ability to assume historical results an indexed universal life policy might have achieved given its current cap rate and floor, which permits insurers to assume potentially unsustainably high rates of return.

Whole life, for example, must use whatever the current dividend scale is as a basis for future policy values. If insurers were instead permitted to use some average from past dividend scales, the resulting projections would be higher. Witt doesn't argue that whole life should gain the ability to average past dividend scales to augment projection values, but instead that more restrictions are necessary to curb IUL projections.

I agree in spirit with this sentiment. The subject is certainly complex and requires careful evaluation of mechanics that takes more into account than just one really juicy example of a potentially over-inflated IUL illustration. Also, it's worth noting that the National Association of Insurance Commissioner's Life Actuary Task Force is working on amended illustration rules to remove bonus interest assumptions from illustrations.

Lastly, on this point, Witt does correctly call out the unrealistic projections created by spreads assumed in indexed (sometimes referred to as “arbitrage”) loans. The spread sets the projection up to assume a highly unlikely situation, and the industry has done a mediocre (at best) job in curbing the impact of this from an illustration point of view.

Part 3: Do IUL Policies have an Investment Advantage Over Whole Life Policies?

Witt presents these questions and starts off stating:

It's hard to see how an IUL policy would have an investment advantage over the general account of a quality mutual insurance company over the long haul.

There's a statement here that seems to suggest that mutual insurers heavily engaged in whole life selling invest more assets in equities or “equity-like investments” than insurer heavily engaged in selling IUL. The paper states that mutuals invest 10-20% of assets into such allocations and the rest into bonds. Then states that IUL focused insurers invest 95% of assets in bonds and the remaining 5% into hedging instruments already mentioned (i.e. the call options).

That statement ignores the asset allocation exposure differences between a heavily skewed whole life insurance company and a heavily skewed indexed universal life insurance company.

This is certainly an area where one with a penchant for facts and figures can obtain very precise information on how allocations differ (if at all) between these life insurers. We visited this subject numerous times in the past. And I'll tease you to stay tuned for more on this subject in the coming weeks.

Witt then asks if management at life insurance companies engaged in selling IUL is so confident in their ability to achieve high returns with the hedging investment strategy that comprises the majority of the return used to pay policyholders, why not quit the job at the life insurer, establish a hedge fund, and make beaucoup bucks executing the strategy and keeping more of the money for themselves?

This question is silly, and it falls closely in line with the investment salespeople's argument that you and I can achieve the same results life insurers do with whole life insurance by simply investing in the same things life insurers do. If you believe that, you don't understand tactical investing quite as well as you think you do. I'd also assume that Witt is not a proponent of this idea.

Lastly, in this section, Witt makes a comment that severely impaired my faith in his expertise regarding universal life insurance. He references the illustration used throughout the review and notes that cash value will not equal premiums paid until year 10. In other words, the policyholder will not break even until year 10:

So who really cares what the crediting rate (or cap rate) is in the first 10 years of the policy? What's going to drive the long-term value of the policy is the level at which future cap rates will be set.

The suggestion is that current cap rates don't matter, especially because the policy cash values lag behind the premiums paid, so it doesn't really matter what they are. I think what he intended to allude here is that insurers might drop cap rates in later years as the cash value of a policy becomes more substantial and the absolute dollars paid on cash value balances will be higher. I know of no evidence to believe this is likely.

But there is another, much more subtle problem with this discussion that one likely only questions if they have a deep understanding of life insurance policies. Earlier the review states that there are doubts an indexed universal life policy will produce any real advantage over a whole life design that is “optimized to reduce agent compensation and maximize policy efficiency.” This suggests that Witt has a clear understanding of how to manipulate whole life insurance to produce more favorable results for the policyholder.

What's strange is that he doesn't mention the same “optimization” for indexed universal life insurance, which is…I assure you…a thing. Failing to bring this up calls into question his level of expertise concerning universal life.

In fact, the first thought I had when he mentioned the 10-year timeline to break even in the IUL policy was, “it's probably not the most efficiently designed approach to the policy in question.” But instead of bringing this up, the long break even point is used as an indictment against IUL.

Part 4: Premium Financing

Next up in the review is an area I feel many other industry leaders and influencers need to sound words of caution and thank you, Scott Witt, for taking time to do it. He notes that premium financing schemes using indexed universal life insurance add layers of risk that are often inflated when it comes to projected functionality.

To give him as much credit as possible, Witt does reference illustrations for premium financing that assume a year-over-year rate of return of 7.6% against an assumed initial bank loan rate of 4%. He notes correctly that if you can borrow money at 4% and earn 7.6% on it, there's certainly a positive spread that makes the policyholder better off. And he also correctly points out that this is an extremely iffy scenario to unfold that comes with multiple risks not easily discerned from a life insurance illustration.

But here's the thing…

…this doesn't expose indexed universal life as bad as much as using premium financing in this manner is an irresponsible (I'd even say dumb) sales tactic that uses IUL.

That being said, I support the overall notion of this section (i.e. most people should steer clear of it), and I'll be publishing much more on this subject very shortly. We talked about the issue concerning premium financing on the podcast a little over two years ago.

Part 5: The Conclusion

In his conclusion, Witt likens indexed universal life to a house of cards stacked on top of a house of cards. I find this allusion incendiary and he certainly never clearly made the case to arrive at such a bold claim.

He then does a strange walk back by noting that despite all the negativity he does think an IUL purchase can be acceptable provided you use appropriate assumptions about average index crediting rate, which he states should be 5%. Why 5%? No explanation for why this number makes sense.

Lastly, he notes that prospective buyers of indexed universal life should temper expectations for future income distributions by linking credited interest on cash to the loan rate of the policy. I agree.

A Highly Critical Review Lacking the Necessary Substance to be so Highly Critical

I'm sure some industry professionals read Scott Witt's A Critical Review of Indexed Universal Life and nodded in agreement with many of the points made (maybe even all of them). I no doubt believe there are people who, by anecdotal experience, have broad familiarity with many of the issues he raises with IUL–I know I can relate to many of them.

But none of those points are an indictment on the product as a whole. And none of the charges against indexed universal life are well explored with factual data that support the claim that they are in fact bad.

Indexed universal life insurance has unique capabilities that benefit certain fact patterns. This does not make it unique. Whole life insurance, term life insurance, and other flavors of universal life insurance have the exact same reality. Each product has unique capabilities that benefit certain (different) fact patterns. Matching the wrong product to the wrong circumstance results in disappointment.

Indexed universal life insurance is not THE singular answer to ALL life insurance needs. Nor is any other type of life insurance.

There are, I assure you, certain insurance agents and marketers, who do products a disservice by intentionally or negligently trying to sell everyone the same product. There are many things to understand about all life insurance products before you buy, but that doesn't warrant a scathing review that sums up the product as a house of cards piled on a house of cards that produces projected results worth less than the pages used to print them.

I do want to take one moment to say that I empathize wholeheartedly with the review. I sense a large degree of frustration that I'll assume stems from aggressive selling and over-promising for which some insurance marketers deserve ample criticism. Just remember, we should all look to use facts and data as the basis of a critical review.

GREAT ARTICLE AND VERY WELL PUT TOGETHER . EXACTLY WHY I ENJOY

READING YOUR COMMENTS PLEASE KEEP IT UP.

Great response to Mr. Witt’s “analysis.” I got a copy of the article from Joseph Belth and was in the middle of a lengthy reply when your article came out. Your points about the short comings in the Witt article are spot on, as is your take on the general abuses that happen in life insurance sales.

My only addition to your comments would be to point out that there seems to be a strong bias against commissions that comes through in some comments that Scott Witt made. I’d like to draw attention to the fact that when he recommends a life insurance product to a client a commission will be earned by someone and the fee that Witt Actuarial Services charges only adds to the overall acquisition costs. Any competent insurance agent does Scott Witt’s work for free in analyzing the best product to suit his client’s needs.

Thank you for a balanced look at IUL.My team will use this blog post for training.

Gus

I wish you would have started off be describing how you structured your IUL. Many insurance agents don’t know how to properly structure an IUL for growth of the clients cash value. They structure them so they receive a high commission for themselves and the client lose out and their cash value will not grow well and fall into all the problems that you describe in this article. The only way to properly structure an IUL is for it to be a Max Funded option B increasing Death Benefit with a 0 floor and a 10% cap with 2 riders for terminal and chronic illnesses as living Benefits and with a dividend from the general fund of the life insurance company to be used to purchase a 12 month point to point call option so if the call option loses you only lose the dividend and not the money you have been paying as premium payment and you should pay your premiums for life to keep the compound interest growing every year. Also you should make a deal with the insurance company to borrow/leverage their money against your cash value to put back in as additional premium payments to increase your rate of return. This will grow you Compound Interest for a tax free retirement income. To learn more about this, [promotional plug removed].

While your description of how to “properly” structure an IUL is often used (at least an increasing death benefit with max funding to 7702 test limit), cap rate is not a specific requirement for proper design. In fact, agents don’t control the cap rate of a policy. Borrowing money from your policy to pay additional premiums is a sucker’s bet.

Good analysis. I found it illuminating to see Witt’s prior experience disclosed in tiny print at the bottom that showed his prior association with a large mutual whole life giant.