When things are going as expected or better than expected – it's human nature to relax a little bit and let the good times roll. I realize nobody likes hanging out with Debbie Downer or Negative Nancy.

But you gotta be cautious about how comfortable you get when it comes to protecting your wealth. Probably better to be cautiously optimistic. Enjoy your life, hope for the best but always keep your head on a swivel.

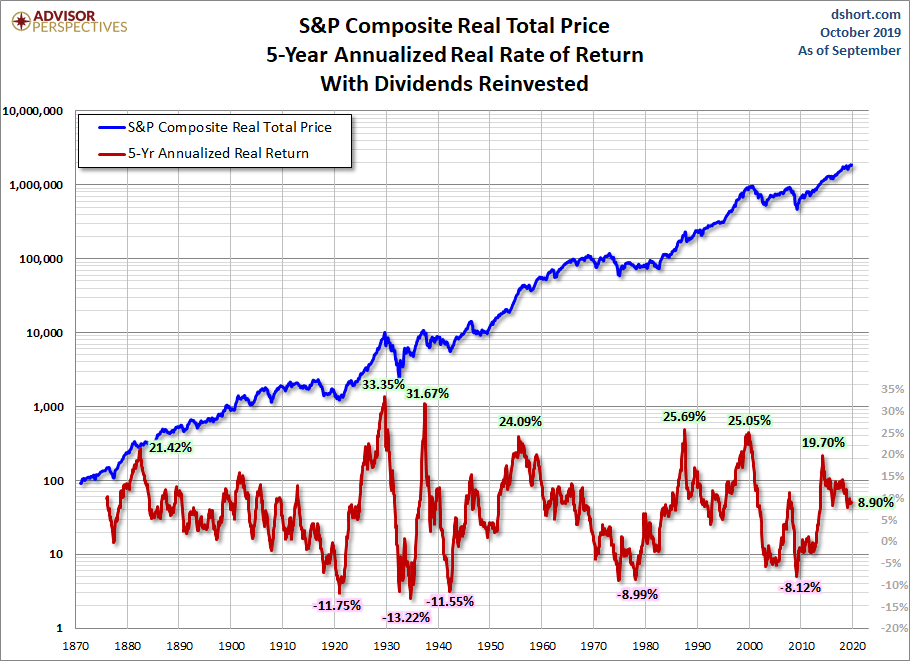

Consider this info from advisorperspectives.com:

Five years ago, you invested $10,000 in the S&P 500. What do you think that would be worth today with dividends reinvested but adjusted for inflation? The purchasing power of your investment is now $15,579 for an annualized real return (return minus inflation) of 8.90%.

Chart provided by Advisor Perspectives: Latest Look at Total Return Roller Coaster

Chart provided by Advisor Perspectives: Latest Look at Total Return Roller Coaster

In March of 2009, the 5-year window had a real return of $6,654 (-8.12%). Yeah, that means you lost about a third of your spending power from March 2004 – March 2009.

The point of saving and investing is to eventually spend the money, right? Not trying to snarky, I know you realize that but I wanna be sure that we can all agree real return is important.

Of course, that doesn't take into account any tax liability. That would of course cut the return yet again.

The point of me sharing this data is to show you that it is near impossible for anyone to know what the market is going to be like 5…10…15 years down the road. No one can tell you with certainty what the market will be like tomorrow.

Fortunately, there are ways to minimize risk to your wealth accumulation. With a solid strategy, you can avoid the chaos caused by volatile markets.

Instead of using the “set it and forget it” method of dumping all your cash into cheap index funds, follow these three steps to minimize your risk right now:

Critical Step #1

Use savings vehicles that aren't directly invested in the stock market.

Save and invest the safe way.

To be sure you’ll have enough money for the future, you can't afford to get hit with steep market losses, like those we experienced in 2000, 2001, 2002 and 2008.

Truth: Investing your money in the market does provide you with the opportunity to experience above-average returns.

Additional Truth: the chance for getting above-average returns is accompanied by the likelihood that you’ll also experience above-average losses.

Unfortunately, most of us focus far too much on chasing higher returns at the cost of keeping safe what we've managed to accumulate. Chasing returns is unpredictable and risky.

Remember the losing streak that we experienced in the early 2000s? The market was down -9.1% in 2000, -11.9% in 2001, and -22.1% in 2002 and -37% in 2008.

That’s four times in recent history we’ve experienced large market declines. What if you had been looking to retire in 2008 and had most of your money invested in the market?

Would that have changed your plan?

There are other options that can get you across the finish line without that sort of risk.

Critical Step #2

Use savings vehicles that produce moderate returns.

It's like the old story of the tortoise vs. the hare. The hare is fast and exciting; the tortoise is slow and boring. But we all know who wins.

Investors have been questioning decades-old investment practices since the great recession in 2008. Many of us have decided to take a different approach.

Safer investing strategies with protection from loss and the potential for decent, stable returns have become much more popular because people have demanded these options. That’s a good thing for you.

The major advantage that creates for you is the ability to earn a moderate return (more than CD’s or saving accounts) while being protected from suffering market losses. It’s true that you’ll never see a 20% annual return, but you also won’t be in danger of suffering a -37% loss as the S&P 500 did in 2008.

Too many people think that “hanging in there” with a buy and hold strategy over a long period of time can wash away the uncertainty. It’s simply not true.

While the averages may stabilize over long periods of time, the size of your portfolio at the end of the day is unpredictable. And as a matter of fact, the longer time period we evaluate, the more unpredictable the result becomes.

The longer the race, the more unpredictable the hare becomes.

Remember, for an investor concerned with the value of their portfolio at the end of a period of time (example: at retirement), the total return (the total amount of money you have) is all that matters, you can’t spend average returns.

Despite what the investment industry has led you to believe, you don’t need to earn 10%+ returns every year to have enough money for everything you want to accomplish in the future.

Here is another one of those hard truths: Most individual investors will never get returns anywhere close to the market average. Recent data from DALBAR tells us that the average stock fund investor has earned 3.88% over the last 20 years.

And that’s a gross number…before inflation and taxes. The real return is less than 2%.

90% of drivers think they are above average. We both know that's not true. 90% of investors also think they are above average. That's not true either.

You should do everything in your power to avoid steep declines in your portfolio. The tortoise always wins the race.

Critical Step #3

Use savings vehicles that are taxed up-front and never again.

You should grow your assets tax-free when possible.

Almost anyone you talk to will tell you that you need to contribute to your traditional IRA and 401k so you can save money on current income taxes. They'll tell you that the government is basically giving you money by allowing you to save taxes now and allow your money to grow tax-deferred.

And they aren't wrong. Throughout your life, you can use traditional IRAs and 401ks to defer taxes. But, there's a catch.

There's always a catch, isn't there?

The catch is that as you compound your nest egg, you’re also compounding future tax liability by putting off paying taxes until after you retire.

Now what happens is that you have to pay taxes on the entire balance of your IRA or 401k when you withdraw the money. None of that money has been taxed because the contributions were made pre-tax.

And what did our old pal Ben Franklin say? He said “there are only two things certain in life: death and taxes”.

Taxable income in retirement also means there's a higher potential tax paid on your hard-earned social-security benefits. Many experts believe that taxes are only going to increase moving forward.

It’s true that we’ve seen some reprieve in taxes in the short term. However, unless you think there’s some great political will to cut spending, taxes are headed up in the future.

You should be very careful to what extent your net worth will be subject to income taxes in your future. Deferring income taxes seems great now, but don't think that you're never going to have to pay taxes on that income.

Keep your eye on the ball. Saving taxes now by placing large amounts of money into your 401k or IRA seems appealing. But you have to consider the actual numbers, the only amount of money that matters is what you have net of taxes.

This problem isn't hard to fix. There are still a few sections of the tax code that allow you to compound your nest egg without compounding your taxes.

BONUS: Critical Step #4

Use savings vehicles that reduce risk to maximize cash on hand.

Opportunities will come your way and having options is the best way to reduce risk in your portfolio.

One thing that unites most successful investors is that they are extremely patient. If the growth potential isn’t there or they don’t see obvious opportunities at a steep discount, they simply sit on their pile of cash until the time is right.

Consider what Sir John Templeton had to say:

“Bull markets are born on pessimism, grown on skepticism, mature on optimism and die on euphoria. The time of maximum pessimism is the best time to buy, and the time of maximum optimism is the best time to sell.”

You won't lose money if you're holding cash in a market that is inflated and subsequently crashes. And when that market crashes, at the point of maximum pessimism, you have the money to buy.

Fortunes are made waiting on the “fat pitch”.

Having your strategy in line with the first three steps will give you the ability to seize opportunities as they come your way.

You'll have protection against loss. You'll be growing your money at a decent clip. And, you'll remove significant stress about your future tax consequences.

You'll have everything you need to create a sizable tax-free nest egg, which means more spendable money for you and your family. No more buy and hold (wait and hope) finger-crossed strategy.

You won't worry about losing 30%-40% each time the market takes a tumble. You won't stress about getting walloped over the head by tax increases when you are finally able to retire.

The wisest decisions you can make with your nest egg are the safest ones. The best way to win the race is to run it at a slow and steady pace.

Whole life insurance is a nice, safe, warm place to warehouse a sizeable portion of your wealth while you’re waiting for those opportunities.

And as I tell people all the time, it works for without any special voodoo or trying to cheat the IRS. Simple, consistent and straightforward.

If you’d like to see how it might work for you, contact us here.

Is Life Insurance for You?

Want to know if life insurance belongs

in your financial plan? Contact Us today to find out.

I love your blog post and very helpful information. However I miss your podcast.

Thanks for the kind words Jamie! You aren’t the only one who’s expressed that about the podcast. We’re trying to figure out how we might do that.

We need more B & B on the podcast, you guys are great!

Stay tuned Frank, I’ve been hearing rumors that we might come back 😉

Hello Brantley

Very good information here. Step 3 is especially astute. I wish that your message could somehow be delivered to every working person in America.

As you wrote, most investment advisors say that a person should save for retirement using a traditional IRA and traditional 401K, to reduce taxes while he is working. However, this strategy will REDUCE the person’s Social Security retirement benefits (which are based on taxable earnings) and INCREASE his taxes in retirement. This is exactly the opposite of what good retirement income planning should do, which is to INCREASE income and REDUCE taxes.

PS: I miss the podcast. Driving home from work just isn’t the same without listening to Brandon and Brantley.

Thanks Harry! We’ve gotta get this message out there. There’s gonna be a lot of people who retire and have a lot less in net, spendable income than they thought. Everyone focuses on fees, commissions and other “evils” but seem to forget about the biggest expense of all…taxes.