Podcast: Play in new window | Download

(Complete Show Notes Below)

![]()

![]()

In the 55th episode of the Financial Procast:

ESOPs Gone Wild

The DOL has filed a lawsuit against the California Pacific Bank. It seems that after the bank unwound their ESOP, they violated ERISA law by shortchanging the employees who were the plan participants.

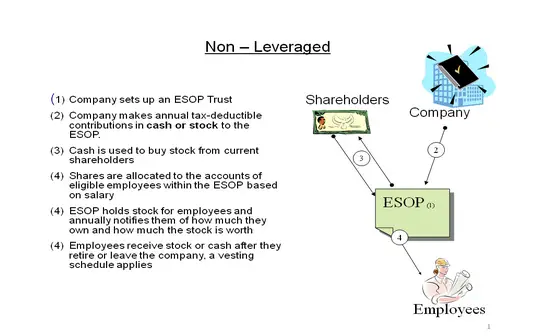

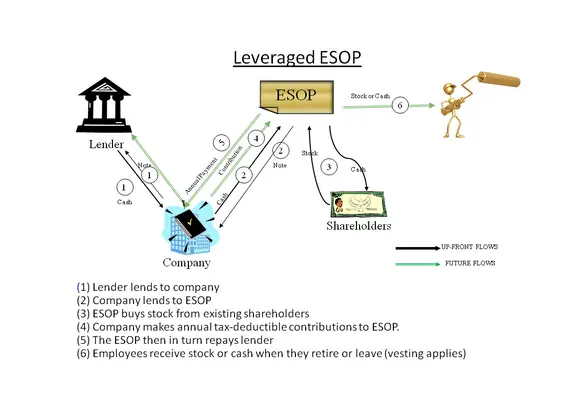

First, we thought it appropriate to offer a high level overview of ESOPs just to make sure that we're all on the same page. ESOP is the acronym for employee stock ownership plan which is just another type defined contribution qualified retirement plan (think 401k, 403b, 457). The major difference being that they employee doesn’t actually contribute anything. All contributions are made on behalf of the employee and in the form of company stock.

The ESOP is established when a company creates a trust and the company makes deferrals on behalf of the employees. There are actually two different types of ESOPs, the non-leveraged ESOP and the leveraged ESOP—I’ve included a couple of graphics to make the explanation easier to understand for us visual people.

Why would a company enter into an ESOP?

Well, typically we see it when the owner(s) of a company would like to sell their interest but don’t have a buyer or a really solid succession plan. That’s not the typical explanation that you’ll hear from organizations that advocate for the formation ESOPs. You’ll usually here those who are pitching the idea of an ESOP as something that will align the values of employees and the company because everyone now has a vested interest in maintaining profitability and viability of the company.

Sounds good right?

Yeah it does, however, the employees really don’t have much control over the company and the primary reason most companies enter into an ESOP is because the original owners can leverage a significant tax advantage and/or force a liquidity event when they otherwise wouldn’t be able to cash out.

In this instance, the California Pacific Bank wanted out of its ESOP. Of the $1.24 million of value in the plan, the employees ended up with much less. The liquidation rules set forth by ERISA for an ESOP dictate that the employees must be compensated in cash, but in this case the fiduciaries of California Pacific Bank decided to compensate plan participants/employees in stock.

What’s the problem with that? Well, besides the fact that it clearly violates ERISA law, it’s a small bank and there’s no secondary market for the bank’s stock–it wasn’t publicly traded.

So, these employees were now in possession of stock that no one wanted to buy. The DOL says, “uhhhh…no” you can’t do that and have since removed the trustees. Additionally, the DOL has appointed an independent fiduciary to administer the plan liquidation and termination.

Alternative Investments Aren't So Alternative Anymore

William Bernstein and others have declared that so-called alternative investments are dead. Well, maybe they’re not dead completely but perhaps it’s just that alt investments have become so mainstream that they can’t really be considered alternatives anymore.

Once upon a time, 20+ years ago, there were true alternative investments—commodities, precious metals, privately traded REITs etc. that were either negatively correlated to the general stock market or not correlated to the market at all.

That is to say that you could make alternative investments that would move in the opposite direction of the market or just didn’t move in tandem with the market at all, they were completely independent of market movements.

However, it seems that so much emphasis has been placed on alternative investments in the last couple of decades as a component of modern portfolio theory (MPT) that all of the alternatives have moved closer and closer to being directly correlated to moves in the stock market.

How does that happen?

Well, in the era of “if it bleeds, it leads” the financial press has talked so much about alternative investments that they’ve become mainstream. William Bernstein says, “As soon as it’s discovered, it’s already gone”.

Additionally, the availability of the alternative investments, the methods of trading and the small required investment minimums have changed the effectiveness of being true alternatives. In the first half of this year, alternative investments have been more correlated than at any other time in the previous five years.

This fact seems to indicate that it really is the mechanism of trading that’s causing a majority of the problem—not necessarily the underlying value of the investments themselves.

There is a much greater opportunity for prices to be manipulated because of the active trading. In the past, average investors didn’t have access to alternative investments because the minimum investments were high and you couldn’t just decide to sell out any time that you wanted to. Most had specific liquidation events throughout the year where you could redeem your investment if need be. This lack of liquidity kept active trading to a minimum and was agreed upon in advance via contract.

Now all of these alternative investment money managers have to deal with the same problems of every other investment manager and it makes the “alternative” just like everything else.

Indexed Universal Life Insurance Fueling the Fire

LIMRA reports that sales of IUL are driving the growth in new premium for life insurance sales. Sales in general are up slightly, but IUL is the runaway leader. It’s been growing at a rapid pace for a number of years, for the second year in a row sales have grown almost 25% year over year.

More accurately, IUL sales grew by 29% in 2012 over 2011 and so far this year 23% growth over 2012.

Even Fox Business News is enamored (they obviously didn’t clear this with Dave Ramsey). In a recent news story Fox Biz said, “An emerging and fast-growing contract design—the indexed universal life (IUL) policy—may come very close to being the ideal contract for most consumers in today’s interest and overall market environment.”

We are starting to see some real media attention focused on IUL. What’s more encouraging as that people seem to be discussing the use of it in a way that we’ve been talking about for a while now—a legitimate alternative to augment returns. In this particular product you can take advantage of fixed interest if you want but you also have the option of choosing to use an indexed strategy that can augment returns. Without getting too lost in the tall weeds the insurance company is able to take a small portion of your premium to buy call options and credit you with a gain up to a cap when the market goes up.

But if the market goes down, you just get zero. No negative returns due to market loss. Now, you still have insurance costs etc. and your interest gains won’t be able to cover the charges but you don’t get hammered with huge market losses.

Another point we’d like to make is that it’s been about 6 or 7 years since the big four mutuals– Northwestern Mutual, Guardian, MassMutual and New York Life called IUL a “passing fad”. All of their career agents are banned from selling any IUL products.

Alas, IUL hasn’t passed…in fact it has gained steam and shows no signs of slowing down.

Stripper Rights

Yep, strippers are making a comeback here on the Financial Procast. We recently had a couple of articles that have come to the forefront that bring this topic to our show.

Evidently there’s now a union for strippers? And the AFL-CIO represented a group of them in a lawsuit in New York to fight for w-2 status and get them minimum wages.

Guess what? The judge in the case sided with the strippers and said that they are the main attraction of the business and you can’t have a long list of micromanaging rules for 1099 status workers. No more stage fees, song fees, late fees etc.

You know what came to mind about this whole case?

Strippers and insurance agents have a lot in common.

Yep it’s true. If you’re an agent working in the “career” agency system you are basically treated the same way.

We’re going to give you a contract to sell our products (exclusively), we’re not going to pay you a salary but we’re going to require you pay us rent, pay for paper, pay for your phone, computer, cubicle etc.

But you’re in business for yourself…yeah right. Or my favorite, “You’re in business for yourself, not by yourself”.

Even though the general agent/career company can cancel your contract at any moment without cause and you lose all of your files, your contacts and we’ll sue you to make you pay for things we made you finance through us. Sounds like a great deal…right?

No thanks, I’ll really have my own business, offer what products are best for my clients, and pay for the expenses I deem necessary.