For years talking heads have been very clear about the use of life insurance in retirement. And still today, despite macro economic events that have shaken a lot of conventional wisdom to its core and caused it to seriously question the validity of axioms used to develop both its most basic and advanced edicts, there is still one subject upon which most of the commentators still agree. You don’t need life insurance when you retire.

For years talking heads have been very clear about the use of life insurance in retirement. And still today, despite macro economic events that have shaken a lot of conventional wisdom to its core and caused it to seriously question the validity of axioms used to develop both its most basic and advanced edicts, there is still one subject upon which most of the commentators still agree. You don’t need life insurance when you retire.

Surely this sage advice, which many in the financial media (and investment industry) have reasoned time and again, holds true–despite recent economic woes that should have caused most us to rethink things a bit.

Might we now be discovering that the problems life insurance seeks to rectify are indeed permanent problems? Nah, everyone knows that suggestion was just dreamed up by life insurance company home offices across the nation as a cleverly disguised ruse to bring in more premium dollars.

Maybe…or maybe not.

What has Conventional Wisdom actually Proven?

The notion that owning life insurance once you reach your golden years is only something fools do is predicated on the same idealized scenario that gets buy term and invest the difference off the ground. There is a carefully crafted set of circumstances that must align perfectly for the advice to actually be good advice. The problem is that life doesn't work this way. It's not something that happens in an orderly fashion. Most people who try to wade through this complex array we call life aren't able to hit these benchmarks perfectly.

Why?

Because there are too many variables and you can't perfectly control the outcome.

In other words, the “proof” that exists to substantiate the claim that life insurance in retirement is only something suckers who make bad financial decisions do is anecdotal at best. The “if-this-then-that” nature of the argument is beautiful in its construction because if the correct circumstances do not come to pass it’s not the adviser's fault that it didn’t work, it’s the individual’s—or perhaps some higher being, but certainly not the adviser.

It’s a perfect example of one of the most wonderful movie scenes created in the current century, Thank you for Smoking. The scene when Nick Naylor informs his son that as long as one argues correctly, one can never be wrong.

That’s great, but what about Me?

But since our concerns are about what actually happens to you, as opposed to whether or not we argued correctly, we're much less concerned that we've constructed a bulletproof argument. We’re forced to ask a much more humbling question, one many people tend not to ask because 1.) people like being right and 2.) we all hate the idea of not having control.

What's the big question we should be asking ourselves….?

Here it is: What if we're wrong?

And by wrong I mean what if we set the whole thing up on a set of assumptions that might not hold true?

Evidence appears to disagree with your Premise

Unless you refuse to listen to modern day news reports on the subject, there’s a pretty well established understanding in America that we pretty much suck at saving money. The country as a whole is in debt up to its eyeballs and the average American has done a poor job saving for retirement. We’ll keep it PG here on the Insurance Pro Blog and just call it “crappy.”

Back in March of this year, Forbes published an article recapping results from Next Avenue’s scorecard on American personal finances. Average net worth for individuals 65 and older was $206,700. Seems a far cry from the money you’d need to self insure under a buy term and invest the difference scenario where you’ve saved up enough money to cover the death benefit by the time you reach retirement age?

In fact, if we take the average income numbers from the same data source we see that individual in their mid 40’s to mid 50’s (aka prime earning years) we get a really quick rule of thumb insurance need is a little under $500,000. We get there by taking the average household income stated and dividing by two (remember it’s household income and we’ll pretend like wage inequality doesn’t exist for just a minute). Then we take that amount and multiply by 15.

Let’s also keep in mind that these net worth figures include homes, so the amount of liquid savings is much less than we’d likely assume.

So what does this mean? As we’ve noted before buy term and invest the different is merely a marketing/sales pitch used by some insurance agents to get a sale by replacing older permanent products or by investment sales people to free up more of your money to fund an investment plan (i.e. sell investments are build assets under management).

Most people buy term and spend the difference.

Ignoring the Problem doesn’t make it go away

So for those individuals who get to retirement and realize that life insurance coverage sure would be nice, what can they do? The answer is simply buy life insurance. But do they? Yes, by the boatload.

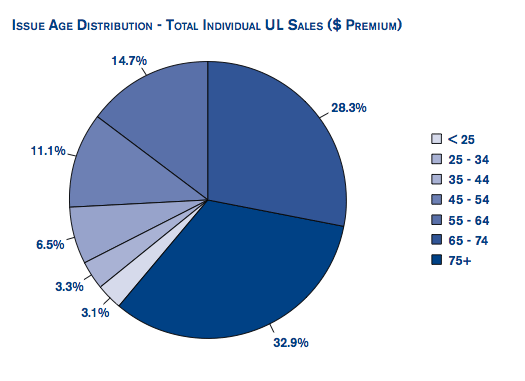

Data from Milliman, an actuarial research and consulting group, researching several topics of universal life insurance tells us that nearly 32% of all universal life insurance death benefit put in place was purchased by individuals who were 65 and older. This data comes from their 2008 report on universal life, and this is an interesting year to look at the data as it’s mostly focused on what took place through 2007—the last year of what amounted to a really good stock market run (click the image to enlarge).

According to US census data, this same age cohort (65+) makes up roughly 38% of the population. So we can tell that the purchase of permanent life insurance by Americans who reach retirement age takes place pretty universally across the age group (i.e. we’d expect to see this group making up a much smaller percentage of purchases relative to its share of making up the total population if, as we’ve been told, there is no need for life insurance in retirement.

But it gets worse as the data tells us another, much more disheartening story.

If you wait, it’s Expensive

The same report from Milliman tells us about the percentage breakdown of incoming premiums by age cohort. Those who are 65 and older make up a stunning 61% of total incoming premiums. Meaning these folks pay a lot more for the life insurance coverage they are purchasing. Notice also that the largest percentage comes from those who are 75+ at nearly 33% of all incoming premiums.

So to recap, the 65 and older crowd make up a percentage of death benefit that is almost perfectly matched to the percentage this cohort makes up as percentage of the total US population, which suggests most people this age buy life insurance. But there is a substantial expense associated with this as they disproportionately make up way larger a percentage of premiums paid for this coverage.

In other words, people are not self-insuring, they are finding need for life insurance well past retirement and they are paying a lot of money—relatively speaking—for it.

Understanding the Difference between Human Behavior and Idealized Models

I’d like to draw an analog to a subject very near and dear to me. Some of you may know that I’m formally educated in Economics, and more specifically in Micro-Economics. Within this field of Economics a lot of time has been spent building models that explain how people interact with the world from the fundamental premise everyone is a utility maximizer.

And despite some very ingenious modeling built on very beautiful mathematical procedures, Economics has gotten it wrong more times than it probably cares to admit.

In fact, these failures to correctly predict human behavior have given way to an entirely new field of study known as behavioral Economics, which is a sort of crossing point between Micro-Economics and Psychology built largely off a model built entirely from empirical research performed by Daniel Kahneman and Amos Tversky. What they built was way better at predicting human behavior, and it didn’t required advanced calculus to comprehend because it wasn’t conceived from a logical construct that required a set of foundational rules that couldn’t be violated.

The buy term and invest the difference notion that leads us to the logical conclusion that there is absolutely no need for life insurance in retirement may be built on sound logic, but the variables and rules that it presupposes are likely just an unrealistic as the assumptions that created early Micro-Economic behavior models. And just because something doesn’t appear to commit any logical fallacies doesn’t make it practical or correct in terms of real life application.

The Alternative Solution

The biggest fail point for Americans regarding personal finance is a failure to plan ahead. Purchasing permanent life insurance early (when finances allow) allows one to compound the benefits of the product to offer up some truly remarkable things as one’s life progresses.

Even if you can explicitly show a lack of need, there are still many benefits to highlight that might clearly demonstrate a want regarding those benefits.

A lot of conventional wisdom is predicated on salesmanship (i.e. we tell you these things—buy term and invest the difference—to get you to buy) without a lot of consideration regarding the actual application of the product purchased and how it will truly be used to accomplish an end goal. Some of us approach this from a different angle. An admittedly somewhat pompous approach that suggests we know better than you the individual consumer. But to our credit we’ve been there and done that more times than you will so our experience helps support some of that grandiose attitude. Additionally, we're not seeking a promotion to Senior Vice President, practitioner/adviser is where we intend to remain–when you already own the practice there's no where else to go.

The empirical data does not support the efficacy of suggestions about self-insuring and lack of need for life insurance in retirement. The inflated premiums brought on by such late purchases have to be a drag on finances that could be remarkably improved if one jumped on the train a decade or two earlier.

As sought after purveyors of financial assistance we cannot approach our clients from an over idealized construct of what they will do because (in our opinion) it’s in their best interest. It’s almost like a doctor who refuses to prescribe a statin to a patient with hyperlipidemia because he or she feels that if the patient would simply avoid red meat and saturated fat the patient would be fine. It might work, but in practice the likelihood of compliance with such a plan is unlikely, and we don’t actually know that such a diet will, with absolute certainty, fix the problem and avoid further complications.

Heavily discounting and or dismissing altogether the importance of life insurance, the benefits of permanent life insurance, or the ownership of life insurance in retirement is a misstep on the behalf of any financial practitioner and a sign of either ignorance or inexperience; possibly both.

please explain what IS the need for life insurance at age65+ up?

Hi Adam,

Those who continue to work out of necessity. Those who live dependently on two social security incomes. Those who live in families where income is generated from an asset that is contingent on a single life (i.e. pensions and annuities where no survivorship benefit has been elected).

I think more data is needed to really see what this study means. My experience in selling UL to seniors has been solely for the purpose of the IRR of the death benefit for their heirs, i.e. ALL policies were GUL with no cash value (or very little CV at times) to minimize premiums and maximize DB. Additionally, the majority of these policies I’ve written listed the insureds’ grandchildren as beneficiaries, and all were non-MECs.

You wrote at length challenging “buy term and invest the difference”, but I don’t believe this study shows that seniors want to initiate cash value LI for the sake of squirreling away money for themselves in later years. My experience suggests that this merely shows that seniors are learning about UL (specifically GUL) as a great way to get an above average return on money which is intended for future generations….and deliver that money tax free.

What say you?

Hi David,

My point wasn’t that seniors would give up on BTID and switch to cash value life insurance as an asset, but rather that purchasing behavior indicates that these people are finding need and/or value in life insurance after the over idealized axioms that get BTID (and other tangential advice like you don’t need life insurance in retirement) off the ground have been tested.

This was the core move behind my analog to behavior economics. We can assume a 12% rate of return and something like 20% of income and show that if you start at 25 you’ll have a lot of money come age 65 and won’t need life insurance. But few (if any) of those assumptions hold true.

Further, as you pointed out, many people buy life insurance for various reasons once past age 65. I’d argue that while those purchases dramatically augment financial goals, it’s highly likely they would have worked out even better if that individual had jumped on the bandwagon years earlier.

Those who are 65+ have only a few options as the time has passed and cannot be taken back. For those with time on their hands, I’m hoping they’ll heed the advice to think very seriously about what their future holds.