Whole life insurance has a pretty wild reputation around the interwebs. There are those who would have you believe it’s the devil seeking to ruin your financial affairs, and others—like us—who believe it’s a pretty cool place to store and accumulate cash—and we’ve encountered plenty of people who agree with us on that front.

Whole life insurance has a pretty wild reputation around the interwebs. There are those who would have you believe it’s the devil seeking to ruin your financial affairs, and others—like us—who believe it’s a pretty cool place to store and accumulate cash—and we’ve encountered plenty of people who agree with us on that front.

Despite the products long established position as a stable asset, there are still those who champion misconceptions about the product, and so we figured we’d take on the top five misconceptions and set the record straight.

#1 That Rigid Outlay/Commitment

The universal life diehards are in part to blame for this one. The common criticism goes something like this: “whole life insurance has a stated premium that cannot be adjusted and must be paid when the premium is due or else the policy will lapse.” The discussion further goes on to suggest that if the policy holder should find him or herself in a situation where that once seemingly easy to pay premium becomes a bit of a stretch, he or she risks losing the policy because they can’t make the premium payment.

While the rigid premium due bit is true of traditional whole life insurance, nothing could be further from the truth if we were properly designing life insurance for cash accumulation purposes. As we’ve explained numerous times, when done correctly, whole life insurance is designed making liberal use of paid-up additions. And when the outlay is made up primarily of paid-up additions the outlay is largely discretionary.

So, a bad year means little more than reducing the paid-up additions rider in that year. It’s as simple and painless as that.

But that’s not all. Let’s say you didn’t listen to us, and let's say you bought an unblended policy with a great big premium and now the time has come when you ain’t got the money.

Oh dear. Truth is all is probably not lost.

If there is cash in the policy that covers the amount of the premium, that cash can be used to cover the premium due, this can take place either as a premium loan, or as a withdrawal of paid-up additions (either because you put them in there or because dividends did) to cover the premium due.

Or if you’ve had the policy for a while, it’s also possible that the dividends themselves are adequate to cover the premium due. There’s a lot of options to entertain when it comes to this product so all is not lost if you don’t have the money to pay the originally planned premium.

Okay, but what if you don’t have cash or dividends to cover the entire premium due?

That sucks, but let’s get a little more creative. There’s always the ability to switch premium modes, maybe a change to monthly so you can cover part of the premium and take it bit by bit will help smooth things out.

Or, as a last ditch effort, perhaps you should reduce the death benefit…that may create a premium that will be manageable moving forward (this one is permanent so choose wisely).

The big take away here is simply that, your commitment isn’t quite as substantial as some would lead you to believe, and if designed properly, is much less of a commitment than you might think.

#2 They Keep your Cash

This is that old Primerica, Dave Ramsey, etc. stumble mostly regarding non-participating whole life insurance (i.e. sans dividends). But is also applicable technically to participating whole life insurance. The contention is that you get a death benefit paid out when you die and not a death benefit with your cash value as well—because apparently life insurance should be “freer” than health insurance in the United States (oh yes I know that’s grammatically wrong on so many levels).

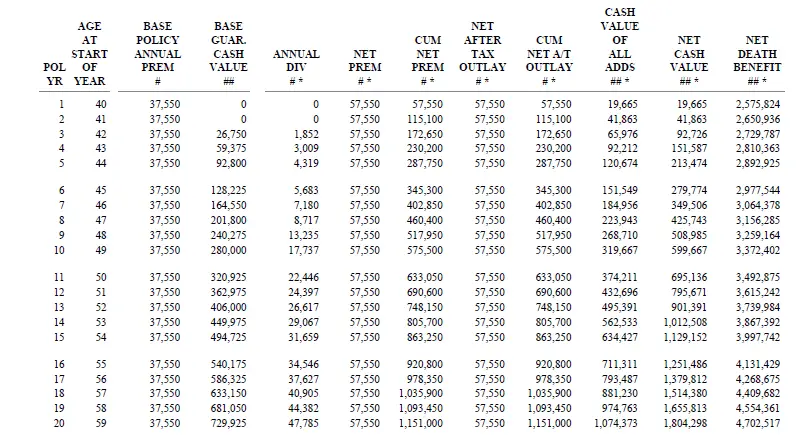

But contrary to this dogged tirade from the “buy term and…oh look a butterfly” crowd, it’s common to end up with more of a death benefit when paying those life insurance premiums. Here’s an example.

[title color=”blue-vibrant” align=”scmgccenter” font=”arial” style=”normal” size=”scmgc-1em”]Click to Enlarge[/title]

Notice I pay the same premium, but 20 years down the road I have more death benefit than I started with. And the difference is more than what I’ve accumulated in cash value.

To be fair, this one does get its steam from non-participating whole life, where the death benefit does not rise and when the insured dies the cash value stays with the company. For this reason, that product isn’t always the best choice for someone, but there are times when it is applicable.

#3 The Return is Terrible

This is one of those absolute statements that always needs a bit of context. Terrible compared to what?

Your savings account? I doubt it.

Stocks? Possibly.

But cash value life insurance in general isn’t intended to be compared to stocks. The risk of principal loss is far greater with stocks and for that there is supposed to be a premium when it comes to return. If there were no potential for a greater upside, stocks would be the terrible idea.

Declaring something bad without some reference to identify what bad means is an invalid argument from the beginning.

What do we have to compare to?

We have current projections, which tell us a rate of return like 5% is not out of the question, and on a conservative savings plan that’s not too shabby. We also have this gem where we say the actual historical return north of 7%…not bad at all.

#4 It’s Fraught with Fees

This one, similar to “the returns are terrible” claim incites the same response from us: prove it.

I’ve always heard a lot grumbling about the fees associated with cash whole life insurance, but I’ve never actually met anyone who could verify it, and I’ve discussed this very topic with a few actuaries who laughed at the suggestion.

Further, if the high fees cry is to be accepted, then we conversely have to concede that the returns aren’t all that bad. Because if fee heavy whole life insurance can yield 5%, what would a fee free whole life insurance policy yield?

On the subject of fees, allow me to quiz everyone today:

Q. What’s the average administrative fee assessed against the cash surrender value of a whole life policy?

A. Zero

That’s right, what fees do exist are generally fixed.

What exists beyond that is an internal schedule assuming cost of insurance (yes whole life has one too, it just doesn’t talk much about it). If you’ve accumulated a million dollars in your whole life policy, however, you don’t then have to share 1.5% of that money with the guy or gal who “manages” the funds for you.

The investment expense component to an insurance contract is part of the premium, not the cash value. Would you rather pay a fee on the million dollars in your policy as an ongoing contingency fee, or just a fee on the $20,000 (for example) that you paid over the course of several years to get there?

#5 The only way to get your Money is to Borrow it

The shrills against whole life insurance commonly bring this one out. They tell you that, “you can’t even have your money, you have to borrow it and pay interest on it!”

We’ve addressed this before. But I will note that there is some truth behind this when speaking purely of the base guaranteed cash of a whole life policy (the cash that is created simply by paying the required premium that includes no paid-up additions). That portion must be accessed through a policy loan. All other portions can be withdrawn.

But so what?

The policy loan aspect to a policy isn’t really a bad thing. In fact, it can be a really great thing.

This one comes down to taking semantics a tad too literally. There are some people who believe that loans incur interest and therefore almost all loans are bad. But there are a great many reasons why one might opt for a loan, and there are great many more reasons why someone might opt for a policy loan on a whole life insurance policy.

Some People have it and some People don’t

Some people hold professions and can be technically considered a practitioner, but their willingness and interest in being truly superlative at what they do is virtually non-existent. There are those who will accept an answer from just about anyone, and those who question the paradigm and dig a little deeper.

I’ve commented before that no one showed me how to do exactly what it is that I spend the vast majority of my time doing (designing cash rich life insurance policies), I figured it out.

And I figured it out because I had enough curiosity to figure it out. It took me an embarrassingly long time to figure out that not everyone has the same amount of inquisitiveness or curiosity stamina as I (in fact I didn’t concede it until late last year, I just always assumed people were trying to be difficult, nope they’re just dumb).

Don’t let someone else’s ignorance be your next mistake. There’s a lot of information out there about whole life insurance spouted out by people who couldn’t identify the product if it fell off a bookshelf in front of them. My alma mater claims that knowledge crowns those who seek it. I very much agree and have been blessed by my pursuit of it.

“buy term and…oh look a butterfly”

I *love* that!