You can find the latest Whole Life Dividend Analysis here.

Whole life dividends are commonly reviewed and compared among companies. For the most part, all we see are current year rates compared. On the rate occasion, someone might bring up the average dividend interest rate among carriers over a certain time period—most often 20, because the people in marketing vaguely remember something about sufficient sample sizes from the one elementary stats class they took in college, problem is they’ve misapplied the rule.

Why can’t We go back 20 Years?

Going back 20 years poses problems because we can’t make the suggestion that investment environment, especially one so significantly grounded in debt investing and as a result is heavily interest rate sensitive, is the same over the entire 20 year period. It’s also entirely possible that much of the staff involved in making investment decisions and managing general account assets has largely turned over.

For these reasons, it’s not prudent to extend our reach of historical performance much past 10 years. This gives us a closer look at what is going on in the more immediate past.

Why Analyze Variations?

Analyzing variance allows us to infer based on trends that we recognize. For example, if we take the average dividend interest rate of each company over a 10 year period we can evaluate who has, on average, maintained the highest dividend yield on policies, but we don’t have any clear picture of how that changed over time. Is it possible that the highest average dividend rate is propped up by an exceptionally good year? This is a common error made by people who simply look at averages and try to infer with that data alone.

Further, since we focus specifically on the use of whole life insurance as an asset building and income producing strategy, it’s very helpful to have a more constant dividend, vs. one that bounces around a lot.

In addition to this, reviewing the dividend rate itself is helpful rather than base policies at a given death benefit for a given age, and gender because it allows us to control more variables.

The Process

We looked at historical dividend rates over the last 10 years for what we would strongly argue are the top 7 whole life carriers in the industry. They are: The Guardian, MassMutual, MetLife, New York Life, Northwestern Mutual, Ohio National, and Penn Mutual. We wanted to include American United Life (part of One America) but they opted to ignore our request for a dividend interest rate history. All data was taken from carrier provided resources.

We took the dividend rates and calculated averages, standard deviations, and change from year one to year ten. The average is of relatively little use to us, but we did want to know how that worked out. The standard deviation let’s us know the variability of the dividend rate during this time, the larger the number the more the dividend rate has tended to change year over year. The year one to year ten change is a review of the dividend trend. In truth a highly variable (high standard deviation) dividend rate with a positive 10 year trend is not really a problem—in fact that would be good news. A highly variable dividend rate with a negative trend, on the other hand, would be problematic.

One Quick Note on Gross vs. Net Dividends

Some of the quoted dividend rates are gross rates while others are net rates. This is the primary reason why looking at the average is mostly useless. But, the fact that this isn’t constant across the board does not effect either the standard deviation or trend review as these only review changes within company numbers.

For example, it doesn’t matter if I was going to measure the standard deviation of height distributions between two groups of people and choose to measure one in inches and the other in centimeters. While it would be odd, it wouldn’t nullify the results as we’re comparing the same type of data (ratio data), and all we’re doing is reviewing how it changes.

The Results

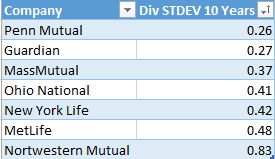

First we’ll look at the table for standard deviations:

All numbers are decimals of a percent

Penn Mutual and the Guardian have the lowest amount of variation in their dividend interest rate over the last 10 years while Northwestern Mutual by far has the most. In fact, at 0.83% they are almost double the average of the group.

But, as we already covered above, this alone doesn’t necessarily mean we can make definitive inferences about the superiority of dividend stability or performance of Penn Mutual or the Guardian and the lack thereof at Northwestern. We still need to review the 10 year trend.

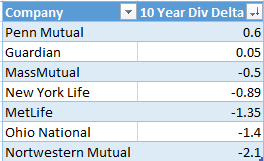

All numbers are decimals of a percent

These are really interesting results. Penn Mutual and Guardian are the only two insurers with positive 10 year trends. The fact that most everyone else has a negative trend isn’t entirely shocking given current interest rates. What is interesting is Northwestern Mutual’s again being the widest change and again well above the average—way more than double this time.

What is also interesting here is that New York Life, Ohio National, and Northwestern Mutual have noted some exceptionally strong years within this 10 year period, and despite this, they’re dividend interest rates have been on the decline.

What we Can Infer

We can note the superlative performance at Penn Mutual and the Guardian with regards to keeping their dividends pretty constant and on the rise. MassMutual deserves recognition for great performance as well since their variation wasn’t all that much higher than the top two and and their 10 year trend is very slightly negative.

The biggest concern would be Northwestern Mutual as they appear to almost be an outlier. This doesn’t seem to reflect some of the positive performance they’ve been happy to report. And while we wouldn’t suggest its any sign of weakness—we can assure you that the Quiet Company is very sound financial speaking—it doesn’t call into question just how great a return we can anticipate from Northwestern moving forward. We suspect this is a direct result of their sheet size of issued policies. They payout a lot of dividends, but they also have the largest number of policies on which they have to pay dividends.

Only one Piece of the Puzzle

It should surprise no one that I’ll declare this piece of information useful, but by no means a single source from which anyone should base a purchasing decision. There are many other factors included in evaluating a company and or its products. There’s even more evaluation that ought to be done on the topic of whole life dividends, but that will have to wait for another day.

Hi Brandon,

I was wondering if you could help me understand exactly how a dividend is paid. I’ve been in the business about 5 years and started to integrate whole life about 2 years ago. While I have a good enough understanding about how these policies perform on a non-guaranteed vs. guaranteed basis based on the IRR report, I wanted to educate myself a bit more on HOW a dividend actually is calculated for a particular policy.

I’ll provide an example of where some of my confusion is coming from. I write most of my business through Penn Mutual so I will use that as an example. A paid up at 100 whole life policy on a 35 year old male, preferred non-tobacco, begins accumulating cash value in year 3. However, using a current-scale illustration, the first dividend in not paid until year 6 (this is using just the base premium, no additional PUA’s). So, obviously this isn’t a simple calculation of dividend percentage (6.35% for 2013) x Cash Value = Dividend. I’m trying to figure out where that 6.35% actually comes into play. Mind helping me out?

Hi Zach,

Very generally speaking the dividend calculation works as follows:

The total dividend interest rate is quoted as the dividend yield and the guaranteed interest rate so in the case of Penn Mutual where the current dividend interest rate is 6.34% for this year we’d subtract the guaranteed rate (4%) from the dividend interest rate and have 2.34 remaining. This is the amount that we can apply to the policy’s reserve to figure out what the dividend amount should be.

Now the reserve is often something close to the cash surrender value (and when the policy is heavy on PUA’s they are generally the same thing) but not always the same. Also, the insurer has the ability to assume various expenses (especially in early) years that would prevent it from paying dividends on a newer policy. This is precisely what you are seeing take place on the policy you referenced (where there is only guaranteed cash value accumulating in years 3 through 5).

This is why we really don’t like the non-blended design. It places a lot of control in the insurer’s hands and takes a lot of it out of the policy holder’s hands. We can generate a lot of cash and a lot of dividends from year one when we blend and load up on paid-up additions.

Hi Brandon,

Thanks that helps clear things up. I’ve been tinkering in Excel quite a bit, trying to dissect everything a bit further (tinkering with the assumed dividend, comparing the illustrated result with my spreadsheet).

I definitely support a heavily PUA funded design, at least on a paid up at 100 policy. My experience with a paid up at 65 policy is that it has been difficult to get much in the way of PUA’s without creating a MEC. I usually use a paid up at 100 design for enhanced flexibility, so yes, use of PUA’s is a must.

I’ve really enjoyed reading through some of the other articles in your blog.

NM’s $5.5 BILLION dividend for this yr! Really no competition out there! Happy Holidays , Russ

Yes Russ, because using one metric/statistic to declare a company’s superiority is always a good idea.

Speaking of dividends, this coming from the company that admitted in a competitive situation a year ago that their UL product was superior to their whole life product in cash accumulation scenarios…

Happy Holidays to you as well

Are the dividends generally paid off of the Guaranteed Cash Value or the Net Cash Value of the policy with most companies? Does it vary allot as it seems that the actual or illustrated dividends are much lower with some companies than others.

Hi Alex,

Dividends are paid based on the policy reserve. This is neither the guaranteed nor net cash value, but usually closely tracks the net cash value. The policyholder will never know what the actual reserve of the policy is as this is not information disclosed by the insurance company.

Hi Brandon,

I used to think like you, based on a rather complex explanation I have seen from Guardian explaining how they calculate dividends. However, I just came across https://www.northwesternmutual.com/products-and-services/life-insurance/how-we-determine-dividends which explains how NorthWestern calculates dividends and it seems rather simple.

But to address Alex’s question, it seems like dividends are calculated off the current Guaranteed Surrender Value (which INCLUDES Paid-up-additions purchased by previously paid dividends!)

Hi Oren,

Again, as per SNFL, policy reserve is >= the policy’s cash value, which would be the policy’s guaranteed cash value in the specific year the company pays a dividend.