Bank on Yourself® is the creation of Pam Yellen and is a process of using whole life insurance as a means to finance major purchases. The claims made by Bank on Yourself® suggest that following the program will unlock hidden wealth secrets employed by savvy investors and business people.

But does it work? We get a fair number of questions on this subject, and I've brought it up in the past. Today we'll focus specifically on Pam's system and discuss where it's correct and where it's incorrect.

What Does it Mean to Bank on Yourself?

The system uses dividend-paying whole life insurance and loans from these life insurance policies to finance major purchases. This includes things like:

- Buying a car

- Going on vacation

- Paying for a home renovation

- Buying a house

- Paying for college

This is not an exhaustive list.

The Bank on Yourself® system is part whole life insurance quirk and part habit-forming process. The system exploits the fact that whole life cash value continues to grow, earning interest and dividends even when you take a loan out against it.

The system also requires that you follow a behavior pattern that results in your putting more money back into the policy than you took out to “finance” your purchase.

Putting more money back into your policy than you took out takes form as a pseudo interest payment you make “to yourself.”

For example, let's say that you wanted to finance a home renovation that will cost $20,000. You take a $20,000 loan from your whole life policy and you set an interest rate on the loan that is something higher than the loan interest charged on the loan from the insurance company. This additional interest is paid back to your cash value through the paid-up additions rider.

Two things happen when you do this:

First, the cash value in your life policy continues to grow per the normal mechanism of whole life insurance. Second, your additional payment of cash into your policy creates a cash value balance that is larger than originally assumed had you not taking the loan because you put more money into the policy.

So Bank on Yourself® plays a subtle mind trick in order to establish a behavior pattern conducive to long-term saving. If you're going to “splurge” on some major purchase, you are also going to commit an additional savings paradigm as a sort of quid pro quo.

It's sort of like committing to saving a dollar for every time you go out and buy a latté.

Is It Too Good to Be True?

The Bank on Yourself® system doesn't so much unleash a secretive world of limitless wealth potential, but instead introduces a new behavior and capitalizes on an age-old feature of whole life insurance. In fact, you could use the whole life feature and skip the other facets of the program to realize a net benefit.

Conversely, you could adopt the fake interest payment policy and skip the whole life insurance and…most likely…realize a net benefit.

So at its core, this is all Bank on Yourself® does. Taken to this level and practiced diligently, the system will help a great many people accumulate more wealth than they likely otherwise would.

But…

There are times when Bank on Yourself® practitioners and the company itself try to stretch reality and claim the system employs magic you'd otherwise never find. At one time, the company–or its parent company the Howard-Yellen Limited Partnership–trademarked the term Spend and Grow Wealthy™. The company wasn't always super clear about how exactly one achieved more money in their “Bank on Yourself Account” and liked to make obscure references to unsubstantiated stories about famous business tycoons supposedly using the system to reach their stratospheric success.

The sizzle that accompanies many Bank on Yourself® presentations often oversold the concept and had a bad tendency to flat out mislead potential buyers on how whole life insurance dividends worked in relationship to loan interest paid to an insurance company.

That said, the system works in much the same way self-help systems work. It resonates with some people; not with others. Following it will absolutely create behaviors that assist in building more wealth over time. Whether you need to adopt those behaviors is where the possible controversy lies.

What is an example of a Bank on Yourself® Whole Life Policy?

Bank on Yourself® has done a remarkable job highlighting the fact that whole life insurance is a versatile product that requires careful attention to the buyer's specific needs. The company marketed hard on the notion that few insurance agents truly know how to use whole life insurance in the context of Bank on Yourself®. In truth, they simply meant a blended whole life policy that maximized cash value.

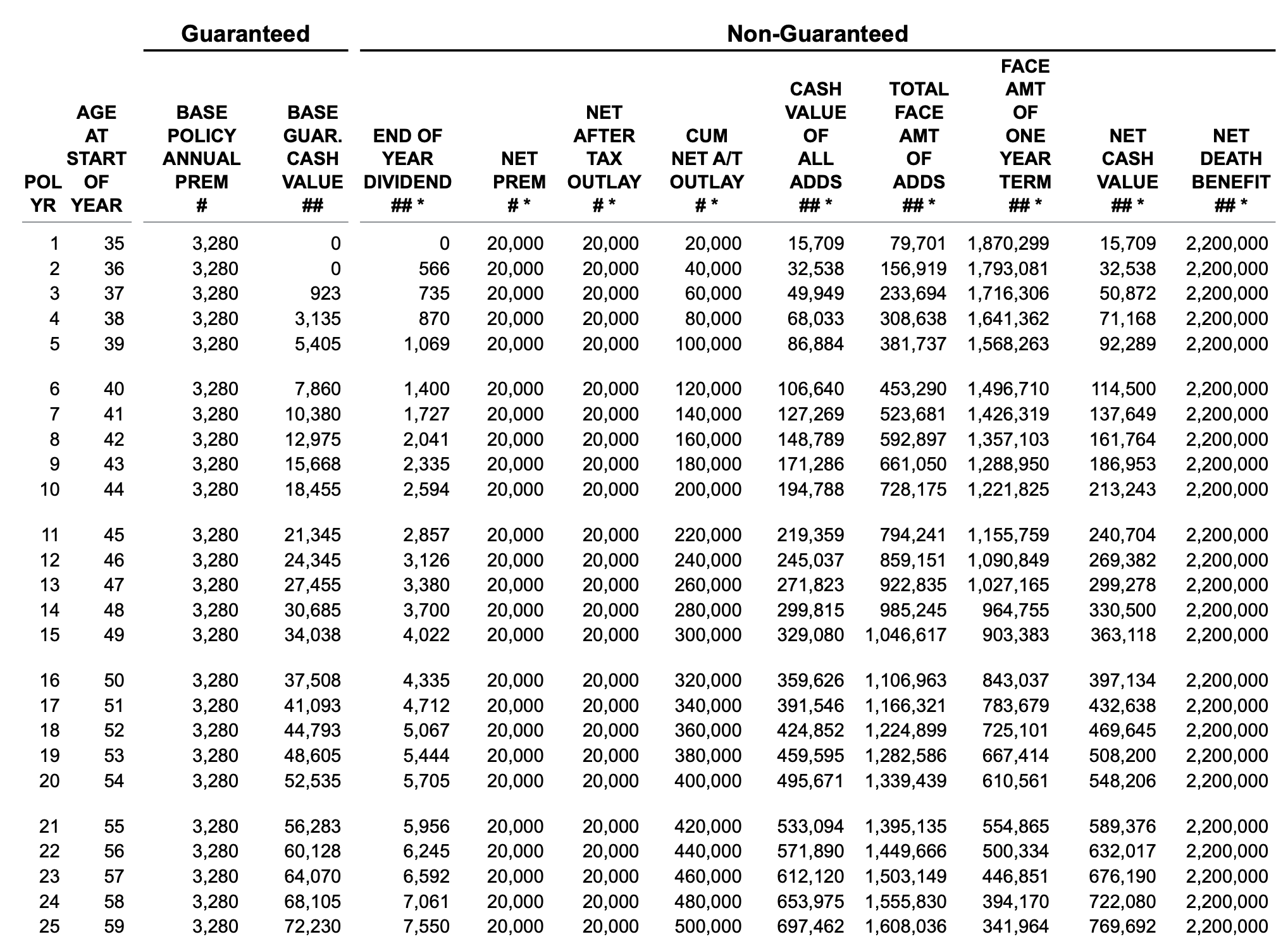

A Bank on Yourself® whole life policy is one that maximizes the paid-up additions feature of a whole life policy and produces as much cash as possible as quickly as possible. Here's the ledger example of such a policy:

This policy has a $20,000 annual premium. For a lot of whole life policies, the cash value after the first year would be zero. But this policy has $15,709 in cash value. Within the first 10 policy years, the policy has more cash value than the sum of the premiums paid, and the gap between premiums paid and cash value continues to grow each and every year after that.

The policy owner could take a loan against this policy as early as the first policy year if he/she wanted.

The important takeaway from this example is simply there is not a specific Bank on Yourself® whole life policy. Instead, there is a design protocol that makes a policy better for the program. That design protocol is one that enhances the cash value of the whole life policy. Doing this gives the policy owner greater capacity to use the life insurance contract to finance major purchases.

Bank on Yourelf® Pros and Cons

Bank on Yourself® does establish a disciplined approach to spending money with a commitment to save additional money after making a major purchase. The system also puts the spotlight on a key feature of whole life insurance that can more efficiently deploy your dollars when it comes to maximizing money saved/accumulated over your lifetime.

In other words, the program is a track to run on and most people find greater success in accomplishing most goals when they have a systematic path to follow.

But…

The program doesn't really create additional dollars out of thin air as it sometimes suggests. It also requires you to buy whole life insurance to execute properly. This can be a major problem for individuals whose health precludes them from such a purchase.

It's also a system sometimes half-heartedly followed by life insurance agents who wish to espouse it only to the point where they sell a policy. There's a considerable commitment an agent must make to the program if he/she truly wants to help people “Bank on Themselves,” and not all agents are willing to undertake such a responsibility.

Your article is, as with all these critiques, not completely factual itself, so let me see if I can help you, without muddying the waters more.

1. Roth’s article compares buying a car through a policy to NOT buying a car at all. Yellen’s concept compares financing through traditional means to financing through your life insurance policy. Are they the same thing? You give him way too much credit. He’s a Wall Street shill. What did you expect him to say?

Furthermore, Roth himself said in his article that the illustrations showed he had more money when borrowing from the policy to buy a car and paying it back the way Yellen describes in her book, than when he didn’t use the policy to buy a car.

She probably can’t sue him because she is a public figure. You may end up finding out more about that yourself in the not-too-distant future.

2. I attended a training session where I saw a spreadsheet showing two $30,000 loans being taken from a non-direct recognition insurance policy, and each being paid back over four years, at the interest rate the insurance company charges. The policyowner recovered all of the interest he paid plus an additional $267.

I would challenge you to produce evidence that a non-direct recognition insurance company “isn’t going to return all of the interest collected through a policy loan”.

3. Some direct-recogniton companies go to extremes to discourage their policyholders from taking loans, for example, my policy with a direct recognition company sends me documents (yes, several) to sign signifying that I acknowledge that my dividends may be reduced if I take a policy loan. Not the case with non-direct recognition. They just ask how much I want to borrow, and continue to pay me the same dividend.

I hope this helps clarify some of your misconceptions about this type of strategy. You should take heed of your last statement, that her “overstatements” of benefits are less egregious than some of the financial gurus (Roth) who rail against her. I hope you’ll take this with the best of intentions.

Hi John,

So let me see if I get this straight. First your contention with Alan Roth is that he compares action vs. inaction vis-a-vis purchasing a car but your point is simply that you cannot make that comparison because the whole point of Bank on Yourself is to compare the impact of borrowing through “traditional” means vs. borrowing from a policy.

But then you state, you have seen spreadsheets showing loans of $30,000 where the borrower made back all of his or her interest plus $267. And despite telling me this, you don’t suddenly see a problem with your first contention outlined above.

The suggestion from Pam and friends is that I pay back more than the company charges me. And, correct me if I’m wrong, the suggestion is to make that additional payment in the form of a paid up addition, not just a simple pay down in principal.

It should not shock anybody that if I take money out of my left pocket and stick in in my right, I’ll have more money in my right pocket. There’s no magic taking place here, and I could accomplish the same thing if I simply took the money out of a bank account, assumed a rate of interest on a loan, assumed a higher rate of interest over that loan, and put money back into the bank account at that higher assumed repayment based on the higher interest rate (i.e. I don’t have more money in there because the insurance company gave me anything, I have more money in there because I put it in there).

The CEO of Lafayette Life himself admitted to Alan Roth (allegedly) that he (Alan) was correct.

Now, if you have hard evidence, why not bring it out here? We’ll even take just a policy illustration that shows us that the insurance company paid more dividends to the insured by virtue of taking a policy loan. Answer this question, if NDR pays the same dividend no matter what, how is the insurance company paying more dividends back to the policy holder who takes a loan? Again, simply paying back more than you owe in the form of additional paid-up additions isn’t magic, and saving more money will always net you more money. You aren’t netting anything magical because you took out the loan.

Taking the loan does not make you better off. Saving more money is making you better off. Just be honest with people, they’ll appreciate it.

Now, we’re not saying the idea is wholly a bad one. The use of a life insurance policy reduces economic loss that would be incurred from simply taking out a loan. But stop with the overly rosy depiction. These products don’t need to be over-hyped, they’ll stand just fine on their own merits.

Thanks for your response. I didn’t write your critique, you did. I think the burden of proof should fall on you, don’t you? Prove that my statement about the additional returns are false. Use real numbers and lets see your illustrations. You wrote the review, now back it up.

Even you must be suspicious about Roth’s comment from the CEO of Lafayette Life.

And your comment about being able to do this with a bank account simply by paying yourself the additional interest is interesting. Is that what people do? Do you do that? Do you know anyone who does that?

And, as a further correction, LEAP is not the same as Bank on Yourself. I have two LEAP policies from 1996 and neither has a Paid Up Additions Rider. LEAP is about the “velocity of money” theory.

Your “truth” isn’t helping. What are you trying to prove? That you know more about this than anyone else? If so, write a book. I’d be happy to buy the first copy.

John we’re not going to play the “I asked you first game.” You come to our venue and claim we made a mistake, now prove you’re right.

This is the same thing we’ve criticized Bank on Yourself for doing. Making claims that could be conceptually correct, but have never been proven by any hard evidence. You failed to explain how NDR pays higher dividends if it’s paying the same amount regardless.

Great discussion taking place. As a third party looking in I think BOTH of you should use examples and numbers to back up your arguments.

Correct me if I am wrong but don’t ndr companies like Layfayette charge a variable loan and ndr companies like ONL have a fixed rate on their loans to prevent funds from being arbitrated?

Lately this blog has been a bit stale, this post was a much needed refreshment.

Justin–Thanks for the feedback.

As for your question regarding loan provisions in relation to NDR and DR companies, the two things are unrelated.

Brandon and I use real numbers every day in our practice to help clients make educated decisions about what company/product they should use. We have no problem sharing openly with our readers and will take your suggestion in to consideration.

I agree with Justin about wanting examples, and numbers.

I disagree with Just about the blog being stale lately… I’m learning something new with every post I read and podcast I listen to. I’m better able to understand this stuff and discuss it with others (and with my friend who are insurance agents).

And it makes me laugh. I know… weird.

Hey Jeff,

Thanks for supporting us! Glad you feel that we offer something new for to learn on a regular basis as I can assure you that we put a great deal of time and energy into everything we publish.

As for examples and numbers, we may consider doing a side-by-side comparison, thanks for the suggestion.

Thanks for sharing this precious knowledge, it extends my knowledge about banking thanks again

Thanks for sharing the perspective on bank on yourself. What I have come to realize is that basic principles are basically being rebranded and marketed to make them look new and give the impression that this is the ‘be all end all’ approach for financial challenges. The only thing that seems to be different between IBC and BOY is the addition of term rider. Otherwise in principle they are both similar. Both parties, Nelson Nash and Pam Yellen, seem to suggest paying more than you borrow and both illustrate how the policy comes out much better. Instead of coming out straight and indicating that the extra money is going into PUA, they give the impression that some sort of magic in whole life is causing the policy to grow. Then there are others who indicate that the money in PUA is going into cash value straight which again I feel is a distorted truth. The PUA buys paid up death benefit and the insurance company basically assigns this money to pay off a future claim. In the interim they are just making it available to the insured in the form of a cash value. So the increase in cash value is more of an indirect consequence arising from buying additional paid up death benefit. I will be curious to see what happens to premiums in policies with term rider given that we are in a low interest rate environment. I came across a WSJ article that indicated about some section 7702 changes and how without this whole life would have been abandoned by companies. I dont completely understand the implications of these changes to existing policies, especially those designed with term and PUA riders. It appears that the change may allow insurance companies to reduce guarantees on a whole life which I assume will be for new policies. Will be curious to know how you think this change will affect existing whole life policies, especially ones that are term blended and have PUA

Hi Jay,

Yes there was a rule change, but all of the reporting on it has been quite mediocre. The one thing reporting on it has shown with absolute certainty is how little journalists spend attempting to understand the subject at hand.

The rule change will potentially permit a higher premium per level of death benefit due to the lower reserving rate insurers are allowed to use. But, this all requires insurers to develop and bring new products to market that benefit from the change. That’s task is quite lengthy.

The suggestion that whole life might go away if not for this change is hyperbole. It was a good lobbying concession on the behalf of the life insurance industry. It likely benefits universal life insurance more so than whole life insurance, but we’ll see how things shake out. Ultimately, not much of a significant change impact wise blended vs. non-blended whole life.

These discussions are all very interesting. I have been trying to understand if there is benefit from baking on your own. I have a copy of the original book by Nash that was given to a friend of his in Cincinnati Ohio. If I am to understand, the whole BYOB concept hinges on putting back more money into the policy than that you have borrowed? If this is the case, couldn’t you do the same thing with a regular bank account, put more money back than you originally borrowed? Is the only difference is that the premium charged on the life insurance is greater than the money that you have in your cash value over a period of time? Just trying to understand some of the intricacies. Also, can you put a significant amount of money into the life insurance policy to the extent that you don’t create a modified endowment contract?

The concept hinges more on the fact that whole life policies pay dividends even on cash value pledged as collateral for a loan. So the idea is that you still have accumulation leverage with the money despite the fact that you are accessing it for some sort of purchasing power activity.

I’d need a specific definition of significant before answering your second question.