In our practice, there's often a discussion that develops around the idea of universal versus whole life insurance and we know this sacred battleground for many of our colleagues. Indeed people do have choices which as we all know can be a good thing and a bad thing all at the same time.

Something that happens for us very often as we discuss with our prospective clients the idea or using life insurance as an asset, leveraging the cash value accumulation to create retirement income, et. al. is a certain degree of “analysis paralysis”. I think most people are familiar with the concept but I'll clarify briefly.

For us, it just means typically that people get a little hung-up on which type of policy is the right policy for them. And we are certainly not making light of the decision. Many times our clients are making a substantial financial commitment that will continue for some time well into the future. Not the sort of decision someone makes without a fair amount of consideration.

Podcast: Play in new window | Download

We are well-versed in both universal life insurance and whole life insurance and we hold no allegiance to one or the other. When we have circumstance where one is the clear winner, we recommend that our client go with the option that works best for them. For us it's not often a universal versus whole insurance discussion as it is a which one makes the most financial sense for our client.

Why It's not Universal Versus Whole Life Insurance?

We deal with both products every day, so we are comfortable with either one. There's no fundamental bias from us toward either product. Ironically, it seems that often times when a person really would be better served by universal life insurance, they choose to use whole life insurance and vice versa.

So along the way we hypothesized “Why not just do both?”

You could certainly own a whole life policy and a universal life policy, we have clients who do own both and they certainly have their reasons for doing so. So, the idea of owning both seems to check of the “diversification” box that is so coveted in a world that has been infiltrated and brainwashed by modern portfolio theory. And it would seem better than getting bogged down in the universal versus whole life insurance minutiae.

But there are times that diversification isn't the answer. And this is one of those times. There I go again saying things that will likely get me in trouble with the financial media overlords…oh well.

Seriously–sometimes diversification just waters down your result. Sometimes it means a lack of focus will result in a mediocre returns when we put it in the context of the investment world.

Don't overlook Scalability

The issue at hand for you with life insurance is that there is a certain amount of scalability to these products. And so, when you don't split your money between two products you don't have to pay to fixed costs associated with owning a universal life insurance policy and a whole life insurance policy.

There are times when more premium into the policy equals a higher yield on the cash that is received. In other words, there's a certain scale that exists which allows a higher rate of return on cash by paying a higher premium into one policy. The truth is that we (Brandon and Brantley) live in a world where we are trying to maximize and enhance certain efficiencies within the product for our clients. Which is why we don't spend much time debating such things as universal versus whole life insurance.

There are some people within our industry that having many different policies is a great idea. We are not two of those people.

Sometimes it is simply unavoidable, for people to have one or more different policies with different companies. Many times those policies were purchased at different periods of their life. Financial situations have a way of changing as we move through life.

But from a diversification standpoint it just doesn't work out all that well.

And you will not be disappointed, as we have plenty of numbers to back this up. We are going to prove that it doesn't have to be a universal versus whole insurance debate but we're also going to show you that it may not be good to split up your available capital for both.

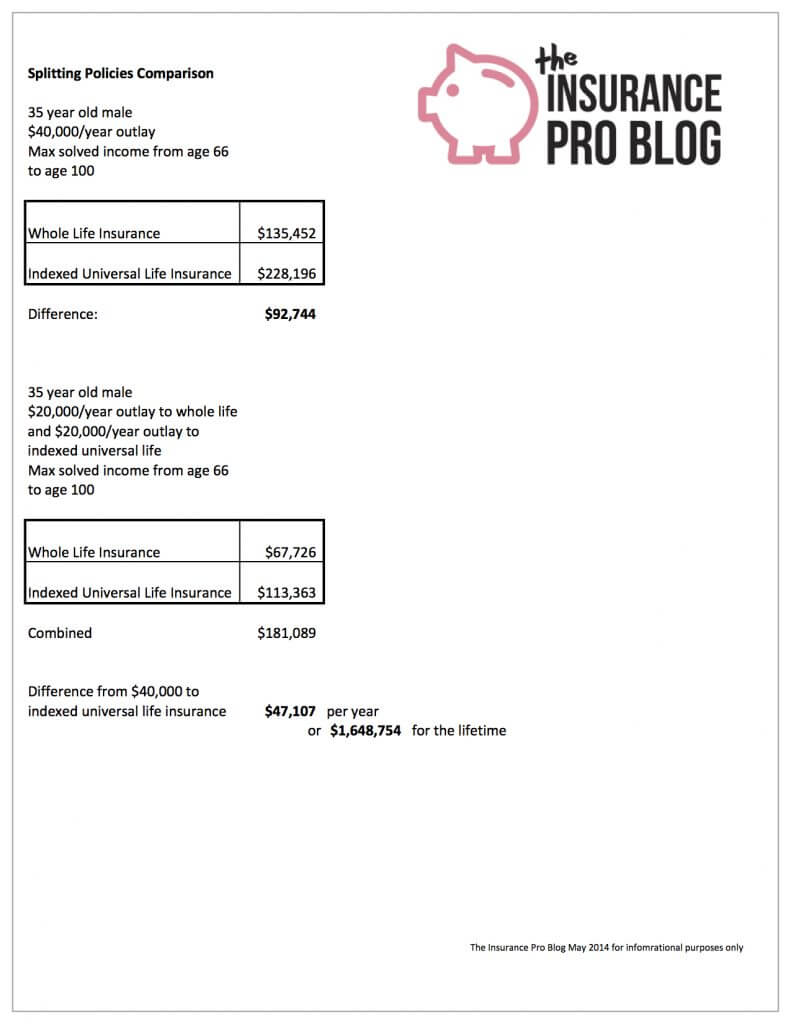

Gimme the Numbers

At this point, I would highly encourage you listen at 15:45 or so to get the discussion surrounding all of these numbers.

![]()

![]()

No need to be concerned with universal versus whole life insurance and there's likely no good reason for you split up your money between both types of policy. If you have a set amount of money to apply toward the strategy, pick one or the other and focus on that strategy.

In most cases, there will be a clear winner, so you don't have to make it a universal versus whole life insurance from the standpoint of one being better than the other.

Hello Brantley,

Thank you for the examples. It seems to be a no-brainer to me to put $40,000/ yr. into the IUL policy, if the IUL cap rates would not change significantly, as you addressed.

Can you tell me approximately how much more cash value these policies might accumulate if a ‘Private Banking’ method would be implemented by borrowing and repaying $25,000 for a new car, etc. every 5 yrs. beginning in policy year 7, as the Banking on Yourself experts recommend?

Also, what kind of criticism do you imagine would these options receive from a broker, who would definitely recommend pouring 40 grand annually into stocks, bonds, and other risky funds, while telling you life insurance for any retirement funds is a total waste of one’s money.

I am an independent life agent in Florida. Do you provide any recommendations for policy design to independent agents?

Thank you,

Dan

Hi Dan,

To more fully explain what our feelings are on any of the “private banking” methods you should read this post https://theinsuranceproblog.com/bank-on-yourself-infinite-banking-et-al-unraveled/

And to answer your question regarding policy design, we do assist agents with policy design and implementation.

When people have two policies don’t they interfere with one another on a tax basis? Or are these cash flow policies completely independent of each other as far as avoidance of Modified Endowment Contract status or other IRS hoops one has to jump through? If a person has two policies do they have to insure two different people?

Hi Scott,

Nope, each policy is independent of the other. Owning more than one policy on one life does not mean that they together affect MEC calculations.

I have two polices on two people. Me and my significant other. My adviser, BOY, set them both up with Lafayette Life. You had criticisms of Lafayette Life saying that they have a rather cavalier attitude to MEC testing. A couple of months ago I received a letter from them telling me that I would be receiving a free Term insurance rider to make my contracts fit MEC status (I interpret that as they screwed up and they are making up for it). I was assured by my BOY adviser that my policies did not go off over the MEC cliff, that if a premium payment did that that Lafayette Life would return the check.

My mother passed away this year and left me some money. I was thinking about starting another Whole life policy on one or all of my Kids but your blog says that this is not a good way to shelter large sums of money since insurance companies are reluctant to insure children for large amounts. That is OK since I don’t have large amounts! If possible I would like to have a small policy for each of the kids. I consider starting other contracts with Lafayette Life to be putting all of my eggs in one basket. What would you recommend? You can ask me more questions if you wish.

Hi Scott,

We sent an email to you with some details. Hope to hear from you, soon.

Thanks.