Cash value life insurance and taxes is a conversation that usually goes hand in hand. You see, life insurance and taxes are old friends—kind of like how Alexander Hamilton and Aaron Burr were old buds.

Cash value life insurance and taxes is a conversation that usually goes hand in hand. You see, life insurance and taxes are old friends—kind of like how Alexander Hamilton and Aaron Burr were old buds.

So life insurance has often been touted as a no brainer idea for those who dislike the April 15th. Some agents might even suggest that only those so patriotic that they’d willingly open up their check book to payoff he national debt if they had the money would pass on the tax benefits that cash value life insurance affords.

While we certainly don’t prescribe to the notion that paying taxes has anything to do with patriotism, we do note that cash value life insurance boasts an impressive lineup of attractive attributes when it comes to tax considerations.

Tax Deferral

The cash values inside a life insurance contract grow tax free. Much the same way that money in an annuity or regular and non-deductible IRA grow tax free. For those of you who have been exposed to this notion before, you know that this sheltering from taxes due each year helps compound the money to grow at a much more rapid rate than a savings plan that required taxes be paid on gains each and every single year.

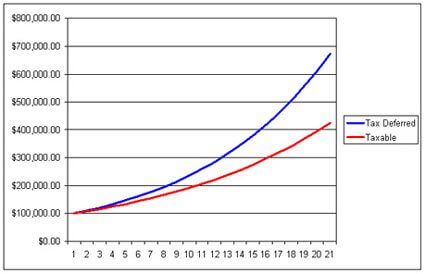

For those who are new to the idea. The math is pretty easy to conceptualize. Any principal amount will compound more if there is more of it to compound. In other words, if you don’t have to take money out of the savings plan to pay taxes, it remains in the plan and compounds. If on the other hand, you must pay taxes on the gain, you’ll lose some of the money that would have been part of the plan and this will slow down the growth rate of the money. Graphically this looks as follows:

Some people refer to the difference in the money you have under a tax deferred scenario and what you have in a taxable scenario as the ignorant tax. While there may be some circumstances that make sense to opt for a taxable account, most people will benefit from a tax deferred scenario.

Any cash placed into a life insurance policy will earn interest and/or dividends (where applicable) and compound tax free. So, cash value life insurance avoids making you pay the ignorance tax. But tax deferral isn’t the only game life insurance can play.

FIFO not LIFO

There are two accounting methods for recognizing the withdrawal of money from a tax deferred account. On is Last-in Last-out (or LIFO) the other is First-in First-out (or FIFO). The names are pretty self-evident, but lets take a moment to ensure understanding.

LIFO simply means that any money removed from the policy comes from whatever ever money last came in (i.e. the gain). So when one takes a distribution from a savings product that uses the LIFO accounting method, they will be withdrawing gain (if gain exists) and this will create a taxable event.

FIFO on the other hand means that what came in first can with withdrawn first during a withdrawal (i.e. the cost basis). This means that when one withdraws money from a product that uses the FIFO accounting method, they can pull out their cost basis first, which does not create a taxable event since this is money that you’ve already recognize as income and paid taxes on it.

FIFO has numerous strategic advantages to is when it comes to withdrawing money. Quickly, without getting into the too many details, these benefits include:

- Withdrawals at any time so long as the withdrawal is basis since there is no taxable event

- Withdrawals that do not disrupt other income sources like Social Security

- Access to money that doesn’t cause increases to income that might cause further tax problems or reduction of certain benefits you might qualify for if you have to claim additional income

Life insurance uses the FIFO accounting method.

But that’s not all

In addition to using the FIFO accounting basis, life insurance has that whole loan benefit. And those loans aren’t recognized as income. So distributions from life insurance can be withdrawn down to basis with no taxable implication, and then one can take a policy loan once the basis has been completely withdrawn to further keep withdrawals tax free.

So once the money enters the life insurance policy, it can grow tax free and be accessed with no taxable implication so long it’s accessed correctly.

But Surely Taxes will be due at some Point

No not really. There are things that could be done to create a taxable situation, but these a pretty easily avoidable. And eventually you will die at which point in time the policy will pay a tax free death benefit to your named beneficiary(ies).

So to recap, the money goes in and grows tax free, it can be accessed tax free either by a withdrawal to basis or a policy loan, and despite withdrawals or outstanding loans, if the insured dies while the policy is in force the policy pays a death benefit that the beneficiary(ies) usually receive tax free.

So yeah, if taxes really aren’t your thing. Or you just happen to like setting up savings plans that give you more flexibility because you don’t have to do the lets-try-to-avoid-taxes dance, than cash value life insurance is definitely a product you might want to seriously consider.

I like you guys, and appreciate the points you make about CV insurance. So I care enough to point out, most folks will not tell you — they’ll just quietly take you LESS seriously because there are a couple of dozen silly elementary school spelling, usage, and grammar errors — they’ll wonder what else you might be sloppy about.

Hi Marc,

Thanks and we appreciate your taking the time to send us any notes about errors that you find.

But…how do you know we don’t intentionally do this to scare off the grammar Nazi’s because we don’t want to deal with them? 😉