For years the investment industry—and various financial gurus—have told us that we can achieve an 8% (or better) return on our money by “investing in stocks.”

That statement is vague on the details so it’s difficult to determine exactly what it means, but the consensus on the inference is that investing in stocks (perhaps even a few bonds) brings with it at least an 8% return. Again, 8% when, where, and on what exactly remains a tad iffy, but silly details such as that need not keep you up at night.

So…what exactly should you anticipate as a return on your money?

Eight Percent…Where did it Come From?

Anyone who spends anytime at all researching U.S. financial markets generally comes to understand that there is this widely held belief that 8% is the “average” return one will achieve on his or her investments “over the long haul.”

This…or something similar to this…is touted by financial advisors and financial gurus all across the country. They often throw in that “over the long haul” bit in an attempt to be somewhat more descriptive.

It allows them to prop open the backdoor of vagueness just enough to prevent anyone from pinning them down to any precise degree of exactitude—you see what I did there?

But from where exactly does this 8% thing come?

I’ve been in the insurance and investment industry for a while now and I’ve spent way too much time (probably more than is healthy) studying the industry and its various data points. And I have to be honest, I’m no clearer now on the origins of this statistic than I was when I first started digging.

Perhaps the closest thing we can get to an origin for this suggested rate of return is simply a rough average return calculated for S&P 500 data “over the long haul.”

There’s even one rogue guru who thinks 8% is chump change and 12% is more like it based on his misunderstanding of what an average is and how it applies to periodic investing. (Sigh)…math is hard.

Using Technology to Establish Expectations

Given the rising popularity of so-called robo-advisors I decided to enlist the assistance of Wealthfront the “largest and fastest growing automated investment service” (their words not mine).

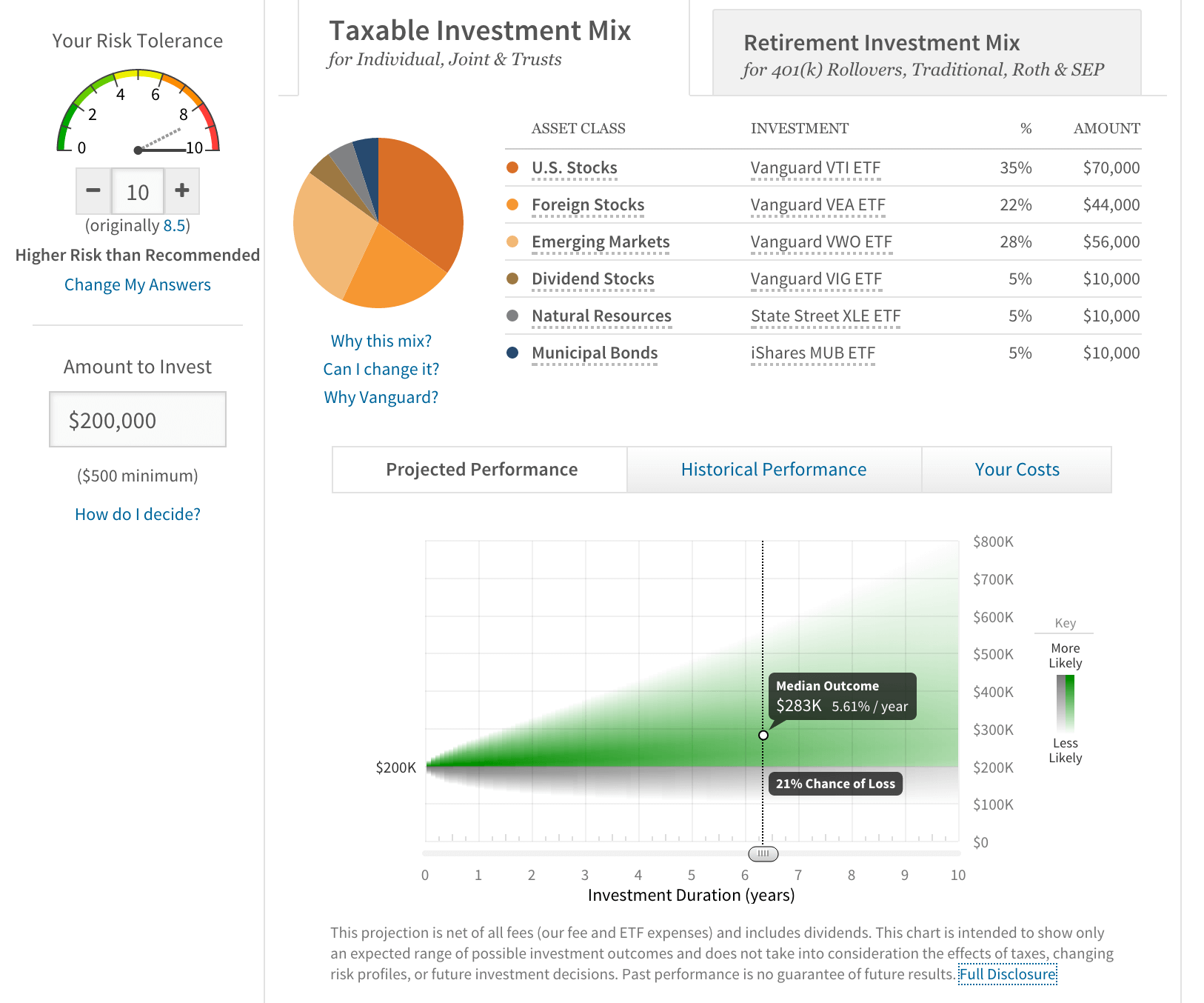

One of the nifty things all robo-advisors make easily available is a brief survey that quickly calculates your investment risk profile. I intentionally wanted investment recommendations that tended towards the riskier side of the scale so I answered the questionnaire like a true risk seeking junkie.

Interestingly, I only ended up at an 8.5 out of 10 (higher numbers representing riskier profiles) on the Wealthfront scale. Not to worry, however, since Wealthfront let’s me tweak the gauge to evaluate the recommendations and projected investment expectations of said recommended portfolio.

So, what does the latest and greatest in terms of Modern Portfolio Theory-loving technology think a dyed-in-the-wool investment thrill-seeker will achieve with the most aggressive investment recommendations it can make? …5.61%.

That felt a little anti-climactic.

Here’s a screenshot from Wealthfront’s web site to confirm my claims:

The $200,000 initial investment is completely random and I can assure you, after plugging in other numbers, that it does not appear to influence the final portfolio recommendations. Moving the slider does not affect the assumed rate of return but it does change the “chance of loss.” I have a number of comments on that piece of data, but that will have to wait for another day.

Now, I have a number of concerns regarding Wealthfront and how it arrives at its investment recommendations, but its apparent acceptance of rather muted return expectations are noteworthy.

The Evils of Overconfidence

Overly rosy assumptions about rate of return can spell trouble for anyone’s retirement or future savings goals. It’s arguably the biggest piece of the puzzle driving the $248.2 billion shortfall private pension funds are facing and the much scarier $4.7 trillion shortfall public pensions funds currently face.

If some of the largest and most sophisticated trading pools are struggling to hit 8% assumed annualized returns, why on earth would you think you will?

We’ve laid out the approach one should take regarding retirement income planning and in truth you could apply this same process to any savings goal with some minor adjustments. But it’s critical to understand that proper rate of return assumption is the linchpin of this entire process.

And according to one of the preeminent number crunching investment advisors, 8% is way above even the most aggressive investment profiles.

I’m a new insurance producer and am struggling with this. I can believe that the average return for financial investments would hover around the 5+% but what data do we have that insurance companies are going to be any better?

Hi Elisa,

Define better.