We’ve addressed the subject of sequence of returns risk in the past. We’ve even discussed it on the new Insurance Pro Blog Podcast. This subject has become a hot topic in more recent years as financial advisors now struggle to build retirement income plans for their clients and face the problem that few, if any, training programs touch. Why isn't their more specific training for advisors on this issue? Speculating about that would be an interesting topic for another day.

Today, I want to talk about how indexed universal life insurance is affected by sequence of returns risk especially in the context of using a policy to generate retirement income.

Life Insurance that Generates Retirement Income

It’s a “too good to be true” concept for some, and a source of newfound glory for others. Life insurance is a tool that one can use to generate retirement income—in addition to a multitude of other benefits. Income is created from the policy’s cash value, which is built up over time and can become substantial if approached and implemented properly.

Indexed universal life insurance is a unique flavor of life insurance because it tracks an index (usually a stock index) to determine the interest rate earned on the cash value in the policy. This presents the potential for pretty significant gain given today’s interest rate environment, but it also causes many to fear the exposure they face given the rise and fall of stock market indexes.

First, lets be clear about the fact that at no time is the money placed into an indexed universal life insurance policy actually invested in the stock market. The index is simply a mechanism measured for growth to determine what interest the insurance company will pay the policyholder on his or her cash.

Why use a stock index and not something else? Like the percentage change of rainfall in Seattle for the month of October from one year to the next?

The answer is largely because there are no financial tools presently in existence to directly hedge the change in rain fall in Seattle (or anywhere else), but there are financial tools in place to hedge the change in stock prices. Insurers use these financial products to produce the interest that they pay to an indexed universal life insurance policyholder.

So how does indexed universal life insurance fare given differing market results of both good and bad specifically focusing on the precise timing of those results? As we know, the timing of market returns can dramatically alter investment results when one holds assets that are actually in the market and subject to losses.

An Indexed Universal Life Insurance Sequence of Returns Risk Scenario

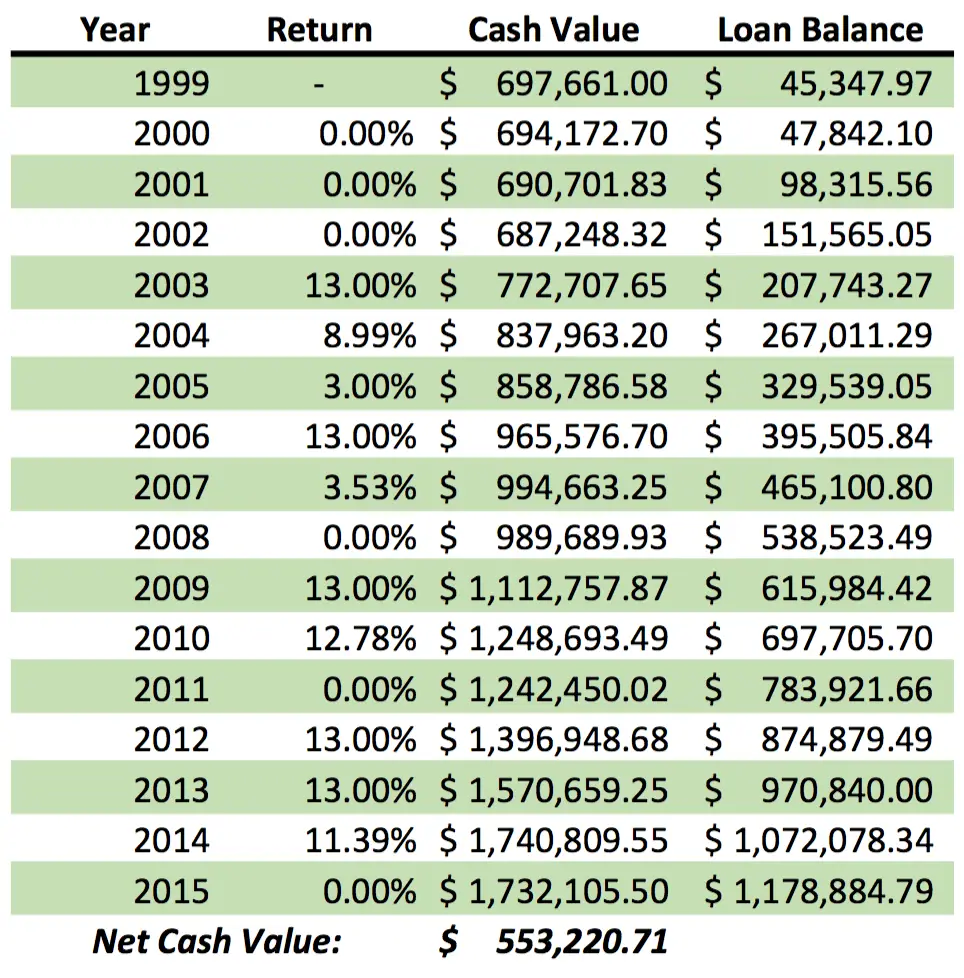

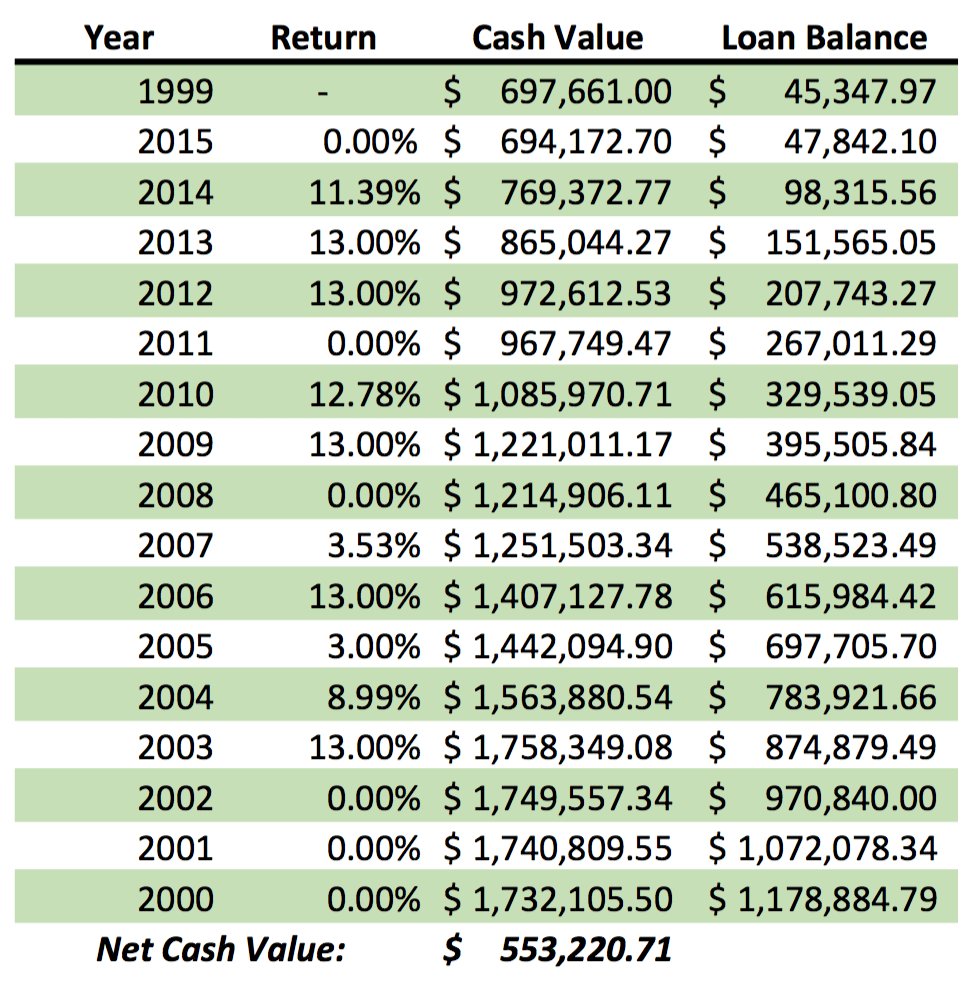

Using a 16 year timeline of 2000 through 2015 I want to evaluate how market returns’ timing affects the cash and functionality of an indexed universal life insurance contract.

We’ll use a hypothetical indexed universal life policy assuming an index floor of zero and cap rate of 13%.

This means the interest earned can be zero but there will never be a year that the policy holder earns a negative return due to market declines resulting in a negative interest rate because the lowest interest possible is zero.

This also means the highest interest rate that could ever be earned is 13% since that’s the cap. Any change in the index beyond 13% is simply ignored.

The index account assumed in this example is the annual point-to-point S&P 500 index assumed to begin January 1st of each policy year and mature December 31st of the policy year.

Using the expense figures we derived from an article we published last year on subject of universal life insurance costs, I’ve made adjustments to the cash figures to incorporate insurance expenses for the contract. However, I decided to inflate the expense assumptions to double those found in this article, just to be safe in my projections. So instead of c. 0.23%, I’ve decided to assume 0.5% of cash value.

I’m going to assume an income stream starting in year one of 6.5%. There’s a somewhat significant discussion behind this 6.5% income percentage, and keep an eye out for an article due to release later this Winter with the details. The assumed loan interest rate in all years is 5.5%.

The initial cash position at income commencement is completely random and just happened to be a number I took from another project I’m working on for someone. It just happens to be $697,661.

I specifically wanted a time frame beginning in 2000 because this time period most significantly highlights the brutal impact sequence of returns risk can have given the run of three negative returns on the S&P 500.

I’m going to use the actual sequence of returns given the underlying index and then flip them around just like we have in the past to highlight the impact of varying returns happening in different sequential patterns.

The Results

Scenario 1 2000 – 2015

Scenario 2 2015 – 2000

The ending result in terms of cash value is the same in either case. In other words, by this example, the sequence of returns do not affect the indexed universal life insurance policy in terms of performance during the distribution timeline.

The ending result in terms of cash value is the same in either case. In other words, by this example, the sequence of returns do not affect the indexed universal life insurance policy in terms of performance during the distribution timeline.

There’s a subtle but important reason behind why this happens. It’s actually two-pronged.

First, there’s the obvious fact that zero is the worst possible situation in any given year. Because the cash in the policy is not subject to a dramatic shift downwards, there’s no variance in geometric mean.

Second, less obvious and arguably more important, the distribution from the policy does not cause a reduction in the cash in the policy. This is a substantial point and the subject of interest in the before-mentioned forthcoming article I teased.

There are a few other interesting observations/advisories to this information.

I want to note the fact that, as others have pointed out, zero interest does not mean zero loss. We can plainly see in years where no interest earnings took place, the cash value declined. This happens because insurance costs are still deducted from the policy. There are, as we have mentioned in the past, ways to avoid this reality. And the importance of avoiding it continues to be a subject of debate.

Nonetheless, despite the loss in six of the 16 years (that’s a little more than 33% of the time) the policy ends the time frame studied in what most would have to consider very good shape (keep in mind that I doubled the expenses we know to be average among an indexed universal life insurance policy assuming standard risk classification).

One should not take this to mean that sequence of returns will never matter to indexed universal life insurance. There are scenarios where it would matter, and we’ll discuss those in later articles on the Insurance Pro Blog.

It is accurate to note that even when it does matter, sequence of returns are far less impactful on indexed universal life insurance than would be the case for several (if not most) other savings/investment vehicles when used for similar purposes.

I don’t Want/Need more Stock Market Exposure

Brantley and I are independent insurance brokers and we hold no allegiance to any company or insurance product type. When people come to us looking to buy life insurance for the purpose of cash accumulation, retirement income, etc. we talk about both whole life insurance and universal life insurance. The most common reason people voice about wanting to avoid indexed universal life insurance has to do with their desire to decrease their exposure to the stock market.

As we’ve mentioned before and have evaluated here today, indexed universal life insurance does not give someone greater exposure to the stock market. The product is market neutral and can insulate someone from some of the negative consequences direct ownership in securities can bring.

This isn’t to set the stage for an “us vs. them” debate. The above does not prove that indexed universal life insurance is superior to any alternative financial product. It’s simply intended to highlight one of the strengths indexed universal life insurance possesses and provides those who choose to own it.

Does this illustration reflect an endowed policy? How do the loans affect the COI if not? Does this illustration reflect direct or indirect recognition? Since sequence of returns has no impact on cash value, then historical avg returns should give same result?

Hi Dave,

Since “endow” has come to mean a few different things, you’ll have to elaborate a bit more on what you mean by that. Loans do not affect COI since loans do not change the net amount at risk.

Direct recognition and non-direct recognition are whole life concepts and we’re talking universal life insurance here, but to draw an analog the loan functions similarly to non-direct recognition.

It’s not correct that arithmetic average and geometric average (CAGR) would be the same.