We love paid up additions. That has never been much of a mystery around the Insurance Pro Blog. And we get a lot of questions about paid-up additions. The one questions that by far sticks out the most involves the variation in loads among various carriers. So in the interest of making this somewhat more readily available (though trust us, we’re more than happy to receive your emails so keep them coming), we figured we’d compile a quick reference guide for paid-up additions loads.

Details, Details, Details

Paid up additions are a chiefly important part to proper whole life as an asset design (unless you happen to be MetLife, but that’s minor detail). And since we’re sticklers for details (which happens to attract other who are sticklers for details as well) this is one of those tangential considerations that we often must answer for those who come to us looking for a policy proposal, and we’re happy to provide the details.

But, it’s important not to get too lost in the deep weeds. The paid-up additions load is important, but it’s not the ultimate consideration, and probably not a great deciding factor. It how however help us to understand why one company might lag another.

The List

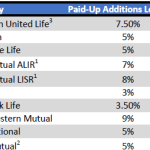

Without further ado, here’s the list (click to enlarge):

As we can see the loads range from a minimum of 3% to a maximum of 9% presently with one company holding the ability to raise loads to 11%. 5% is the most commonly found load among carriers.

And that’s the List

And that’s all there is to it. If you think someone is missing, please don’t hesitate to let us know. And if you’d like more information or to see a whole life policy designed for you, please don’t hesitate to reach out to us. When it comes to maximizing paid up additions, we certainly are experts.

I have Metlife whole life insurance. The load on PUA is also 5%.

Thanks for the update to that Ying!

Assuming one blends a cash value policy and funds PUAs up to the MEC limit every year, is it then counter-productive to choose a dividend option that buys PUAs also? If so what is a better dividend option to put them to better use?

Hi,

Dividend option to buy PUA’s is best. Some companies require a dividend option to buy term insurance for the blending option, but this option can be set up to use excess dividends to purchase paid-up additions and this is the optimal way to set it up.

The PUA load compare you guys did was super helpful. Was curious when you did this and if you have an updated one for 2020. Thank you

This was originally done in 2013. We have PUA load information to the ultimate guide to paid-up additions book we wrote.