Indexed universal life insurance is another strong contender to whole life insurance for the purpose of accumulating wealth and generating retirement income through life insurance. If you need a primer on how indexing works, you can find that here. To explain the concept in 25 words or less, we’ll simply say that it’s a product designed to use stock index movements as a means to determine the credited interest rate on a universal life product. And if you need help understanding the basic mechanics of universal life insurance, that post is here.

Indexed universal life insurance is another strong contender to whole life insurance for the purpose of accumulating wealth and generating retirement income through life insurance. If you need a primer on how indexing works, you can find that here. To explain the concept in 25 words or less, we’ll simply say that it’s a product designed to use stock index movements as a means to determine the credited interest rate on a universal life product. And if you need help understanding the basic mechanics of universal life insurance, that post is here.

So since indexed universal life insurance vies for your precious retirement-building-dollar, we figured we’d ask the same question we asked of whole life insurance just last week. How doe the income change as the assumed rate of interest changes.

Indexed Universal Life Insurance is Evil?

There are those who would suggest this product was a spawn of Satan himself. Sold by over-rambunctious agents wooed by overly stated returns—the ones that speak of the ills of the stock market out of one side of their mouths and then somehow become okay with it when it comes to indexed insurance products out of the other end.

While I certainly do not deny that such a circumstance exists, and still runs amuck within the industry, I’d caution you against anyone who categorically declares the product bad news. Those people are typically stockbrokers, and whole life insurance fanatics (the latter category is one in which yours truly used to be a card-carrying member, oh the ignorant days…).

Still, there are those who will die in the fight to convince us that the product is will send you on a one way bus to misery. And one such rockstar within the insurance industry to make such a suggestion is our very opinionated—and very old—friend R. Nelson Nash. In fact, we covered an opinion piece that a Nash lacky published in the IBC newsletter, which was also published in a book Nash rolled out recently.

I don’t really want to spend much more time discussing the assumed evils of indexed universal life insurance, or why someone who sells a book and other resources to life insurance agents promising them a way to sell more whole life insurance might take issue with the product. I do, however one to mention that they bring up one very important point that everyone should ask themselves about everything they do…what is we’re wrong?

Risk Management Pro Blog Style

I have a pretty big fascination with planning for and averting crises, or at least setting out with appropriate expectations so as to have some contingency incase things don’t work out as planned. When it comes to intertemporal decisions—those that we make for which benefit is floating off somewhere in our future—we can more accurately assess the benefits we should expect if we understand the risks involved along the way.

When managing the risk of a successful or unsuccessful retirement plan, it’s prudent to look at how change will affect our future prospects. This isn’t really new if you’ve been reading this blog for at least a week, as I pretty much said all the same stuff last week. And all of this applies as well to universal life insurance.

The Results

Before I tell you the results, I have to give you the methodology. Blame it on my background in statistics, or accept that it’s just more convenient this way—the choice is yours.

We used the following hypothetical attributes for policy design:

-

- Male age 30

- $20,000 Annual Premium

- Premiums paid to age 65

- Death benefit solved for carrier’s minimum possible death benefit for either TAMRA or DEFRA compliance, whichever came first

- Increasing death benefit to age 65 and level after that

- Income solve loans only on indexed (sometimes called arbitrage) loans…this is the non-direct recognition equivalent to a universal life contract

- Solved income from age 65 to age 100 assuming $1 in cash surrender value at age 100 and using overloan protection rider to keep policy in force

- Initial assumed credited interest rate of 6% then dropped to 5% to assess change

- Loan interest rate set at 1% below assumed credited interest rate, unless carrier product restrictions prevented it

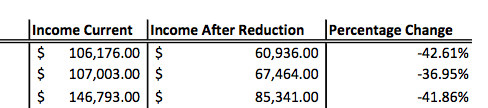

And here are the results, click to see:

The placement of companies in terms ranking projected income didn’t change much once we made the adjustment to assumed income. Lincoln National being the only notable surprise as it fell from 3rd place to 5th place, but that in part can be explained by the fact that Lincoln is the only carrier in the review that uses a fixed interest rate on it’s indexed loans and that fixed rate does not maintain the spread that many other carriers have to their advantage when it comes to projecting income. However, it could also be pointed out that in the real life scenario where the indexed performs as this level, it’s possible the other carriers would in fact have a lower loan interest rate, which would help boost performance.

John Hancock and Minnesota Life projected the least varying income, and I would say that’s a bit weird, but again the driving factor there is the loan interest rate. Other carriers were more impacted by higher minimum interest rate floors that made the spread between assumed credited interest and loan interest small or negative and this of course will make for a larger percentage decline in income.

It is interesting that the distribution of the rates of change among carriers is pretty small. We have a minimum of -32.45% and a maximum of -45.3%.

How Likely is 5%?

The 5% assumed credited rate is pretty low. There are a few reasons for suggesting this, but the most substantial has to do with evaluating stock market trends, including one we did—remember credited interest is based on stock index movement. This means the likelihood that we’d see this sort of change is a tad extreme. But that doesn’t mean it’s not worth looking at the scenario to know who would be the most impacted, or where a company shifts to position among other carriers if this sort of scenario played out.

Ultimately indexed universal life insurance is a stable product relatively speaking, but not without its own risks (however small they may be).