Oops!! Not sure what happened with our other post today…but hopefully it works this time. Thanks for your patience.

As a form of cash value life insurance that can be manipulated for asset building purposes indexed universal life insurance has many coveted features. But just like we noted in the whole life insurance company asset yield comparison it’s wise to take a moment and look at company asset yield performance as an indicator for company strength to maintain the yields we’re assuming.

While it’s not the whole story, the yield on assets under management can help indicate a company’s financial fitness in terms of being able to maintain current caps on its indexing account, which affects how well the policy, will perform longer term.

Indexing: How Interest is Credited

We’ve discussed the mechanics of indexing before but for a really quick introduction the essentials are that money in the account is generally credited a rate of interest that represents the percentage change in an index (e.g. the S&P 500) over a certain period of time (e.g. one year, one month, two years, etc.).

Because the indexing strategy is clearly spelled out at inception, life insurers who issue this type of product are somewhat more limited in their ability to adjust interest payments if they incur unexpected investment losses. With whole life insurance and what is known as current assumption universal life insurance, the insurer can simply reduce the dividend or the annual interest rate respectively.

Because the insurer cannot dictate the rate of interest under an indexed universal life contract it must do something else if it finds itself in a situation where it’s paying more in interest to policyholders than it is making. It can’t raise cost of insurance as it would need claims experience to justify the rate increase. It could (at least in theory) increase administrative charges, but those are relatively small and unlikely to make up for any substantial shortfall. So, the method of choice is to lower caps, which in turn reduces total possible credited interest, and over time will reduce the average rate credited per year.

Alternatively, if experience is better than expected (i.e. the insurer make more money than it had planned to make off invested assets) than it could increase cap rates to allow for more credited interest to policy holders.

Asset Yield, a General Indicator of Policy Yield

I want to focus on the term general when I declare asset yield an indicator to policy yield. Just like we noted in the whole life article on the same subject, it’s a large piece of the puzzle, but still only one piece and not a definitive piece. There are still other considerations that come into play regarding how an insurer derives profits from a life insurance policy.

So with that in mind I want to note that this indicator is helpful in the broad sense but mostly useless in the more laser-focused sense. Meaning if looked at a product with a very high cap and a very high corresponding assumed rate of return, we would want to ensure that the carrier offering that product had a relatively high yield on invested assets to support the assumed yield.

Derivatives Keep them in Mind

Keep in mind that the financial tool that is unique in most cases to indexed universal life insurance is the use of derivatives (puts and calls to be exact). Not that their use is completely unique, just that there is a higher prevalence of their use with indexed products. This use of derivatives greatly helps augment return, further highlighting my earlier point about the limited scope of this comparison—again works really well in very broad terms, but not so well in more precise ones, very intentional redundancy going on here.

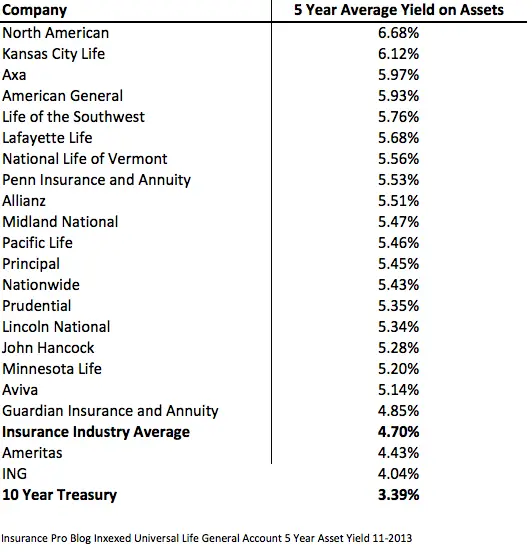

The Numbers

So here are the numbers when we compare 21 U.S. life insurers who issue universal life contracts with indexing options. I believe I’m correct in stating that we’ve included every major player and event a few obscure ones (yes, Guardian now has an indexing option on their VUL product).

[title color=”blue-vibrant” align=”scmgccenter” font=”arial” style=”normal” size=”scmgc-1em”]Click Picture to Enlarge[/title]

Just like last time we’ve included the industry average and the 10 year treasury average, as that is the general benchmark life insurers use to evaluate yield performance. Just like last time all of this information (except for the 10 year treasury yield) comes from Ebix/Vital Signs. The five year average includes the years of 2012, 2011, 2010, 2009, and 2008.

Compare to the Whole Life Results?

Nope we can’t do that. The main reason is simply that the whole life results were done prior to the 2012 numbers being finalized and as such was done on a 2007 through 2011 range. You’ll notice that the average yield of the industry has come up slightly.

Other Important Factors

Other important factors regarding prospects for sustained yield projections are:

- Interest Margin

- Return on Equity

- Profitability of Life Insurance Business to the Insurer

- Net Income

- Investment Risk Profile

- Operational Expenses

To come back to my earlier point, this comparison tells us that we can safely assume that companies like North American and Kansas City Life should be able to sustain higher yields than Ameritas and ING its relatively useless when wondering if Allianz will be able to sustain higher yields than Midland National.

Also, simply picking a company based on where it falls in this ranking is potentially disappointing. Kansas City Life for example ranks better for investment yield than Axa and American General, but manufactures a product that is quite expense heavy and as such there’s a pretty good drag on performance. Both Axa and American General have products that could (even with lower yields) potentially perform better.

Just like any life insurance product purchased for cash value building, choosing wisely is important, you’re going to be together for a while. Indexed universal life insurance is no different than the other life insurance product in this regard.

In Whole Life Insurance Company Asset Yield Comparison, Guardian’s averge yield is 5.68%; however, in this post, Guardian’s average yield is only 4.85%. Could you please explain the difference?

Hi Helen,

Technically two different companies here. The Guardian Life Insurance Company of America (GLIC) is the company that issues whole life and term life insurance while the Guardian Insurance and Annuity Company (GIAC) issues universal life and annuity products.

GIAC is a subsidiary of the GLIC and is technically a stand alone insurance company that manages its own assets and risk. So the average yield at GLIC is 5.68% while the average yield at GIAC is 4.85%.

Hi Brandon,

This seems a bit misleading, as it only takes the reader about 80% through the analytical process. It explains the very simple basics of IULs, but then it rather drifts, insinuating that the account owner’s final credits are somehow rank-able or directly related to the returns of the various general accounts… which is far from true.

The yield on the general accounts determines how much is available for the insurer’s option buying budget… but even that, alone, doesn’t tell the story because 3 different companies with the exact same amount of option budget will still not get the same end results, as each will also have different execution costs or trading access depending on their option trading counterparties (the major investment banks that take the other side of the option spread trades.) FURTHER, for obvious competitive reasons, many companies try to create unique blends of indexes to outperform the competition in one type of market or another.

Lastly, when using IULs for longterm accumulation and subsequent tax-free distribution, via policy loans, the loan terms themselves come into play. A company with offering amazing account crediting, only to solely offer a variable interest rate loan that rapidly consumes the remaining cash values in later years when the interest rates rise, is functionally no better than a low-growth account with a contractually fixed or low-capped loan rate provision in the end. Since companies that offer such low future borrowing interest rates know that they are also trapping themselves somewhat against future safety adjustments, they also tend to have higher earlier internal costs to make up for it… so for the true “bottom line” comparison a professional cannot compare on a “snapshot” basis, but has to build out a full lifetime projection for a particular client’s scenario, among each carrier in consideration.

Hi David,

In the kindest/gentlest way I must ask…did you read this article left to right top to bottom?

Or maybe you just missed the entire third paragraph that started with: “While it’s not the whole story…”

And/or the four to five other times I mentioned (putting it in bold at one point) that this is only one piece to a much bigger puzzle (even included a list of additional factors one should consider).

At no point in time does one reasonably read this article and assume this is the definitive or “bottom line” comparison IUL carriers.

In fact I even mentioned:

The point is simple, yield on assets are an indicator of a companies ability to maintain a certain level of anticipated yield. That’s it. I even went out of my way to point out that the list works well to look at extremes (top of the list vs. bottom of the list) but is useless in more moderate terms (see the Allianz/Midland example).

Thanks for commenting, but let’s try to keep our attention on the topic at hand, rather than trying to make up some fictitious argument that is substantiated on awkward vagaries unrelated to the main idea.

Brandon,

OK then… may I point out, then, that the current (let alone historical) yield on a company’s general account has absolutely zero bearing on the future yield of their general account. Since there is no way the relative rankings of the past has any bearing on the relative rankings of the future, the table of current general account yields is functionally meaningless for the purpose you specified; As “an indicator for company strength to maintain the yields we’re assuming.”

Assumed indexing returns are determined by assumed capes, against historical performance of the specified index. You are correct that a company’s cap adjustments in the future can significantly increase or decrease their indexing account performance… but studying today’s general account yield tells us nothing at all about who might face cap adjustments in the future.

For this, it is better to look to the strength of the company’s ratings, and its corporate culture of cap and guaranteed rate renewals. *THIS* is far more relevant for responsible projection, in my opinion.

Cheers!

Dave Donhoff

Hi David,

Again, one piece of a very large puzzle. Went so far as to provide a list of other considerations. This is one of many things we look at and report on. There’s an entire section to competitive analysis.

These aren’t today’s general account yields, they are averages over the last five years. You know as well as I do that we often look at past performance to get an idea of how institutional investors handled varying market conditions and how they fared (or maybe you don’t and that’s why you’ve decided to make this argument).

Riddle me this:

What are the three basic components to any non-forfeiture benefit life insurance contract?

1. Mortality

2. Administrative Expense

3. …I know you know it…investment return!

It’s entirely possible for the insurer to subsidize one with the other two but since profitability long term is often driven by investment yield (and since those derivatives are part of the overall investment yield) an insurer who is falling way behind vs. its assumed yield has a problem especially if it has a narrow interest margin and low ROE.

We’re not saying that a low investment yield is always a bad thing. Just that having a higher one puts you in a more comfortable position.

Hi Brandon,

You have a premise problem here;

” since profitability long term is often driven by investment yield (and since those derivatives are part of the overall investment yield)”

The derivatives trades have zero effect on the general account yield. The general account yield is used (relative to individual contract owners’ accounts) to buy option hedges for each unique, individual account. The derivatives are *NOT* part of a company’s overall investment yield.

Again, how a company did, as even a single 5 year average, has no predictive value in regards to how likely it is to maintain its caps or guaranteed rates through future events. The single average number simply doesn’t tell the strength or character of a company through past trials (especially unique, non-industry-wide company trials or hardships.)

If future performance is the desired determination, past consistency of cap & guaranteed rate renewals is far more valuable, along with the ratings agencies’ gradings.

Averaged general account yields at a single point in time may certainly give us insight into other things… but singular numbers often hide far more than they disclose.

Hi David,

This is not a yield exclusive to general account assets. And again (and again, and again, and again) I explicitly pointed out your point long before you made it–that this is only one consideration of a multitude of considerations.

What you’ve suggested here violates the fundamental actuarial design of non-forfeiture benefit life insurance. Yield on assets is a very serious consideration. Explain to me how a company develops an asset share if it completely ignores investment yield.

If you do not think that declining yield on assets does not potentially negatively impact an insurer’s credit rating and that some insurers would not act to reduce the negative impact (i.e. lower caps to manipulate expected credited interest rates) you are deeply mistaken.

Investment income is a large driver of profits for insurers. If the yield stumbles it sets the stage for potential cost cutting measures elsewhere. There is profit taking on the derivatives that are purchased to back indexed products. And an insurer can certainly augment those profits by lower caps if investment income is not meeting targets.

Again, this is not a definitive metric. But its one to keep in mind when thoroughly evaluating companies.

Great debate guys. Your points increased my understanding of the topic.