Podcast: Play in new window | Download

We’ve discussed “Sequence of Returns Risk” numerous times in the past, but most of those discussions focused on how this phenomenon affects your assets in a draw down period (i.e. a time when you are spending the money you saved to cover expenses and/or generate income).

Today we want to talk about sequence of returns in a slightly different light and note a problem it poses for all savers while they are attempting to accumulate more value in their portfolios.

Average Returns…We Hate Them

There is little doubt that we despise discussions about investment returns when one references the average rate of return as justification for an anticipated accumulation scenario.

In other words, anyone who tells you that you will have X amount of dollars in your portfolio Y number of years into the future because the stock market has on average performed Z percent per year is often making a huge error in their underlying assumptions about how a particular investment (usually the stock market) performs. This error is especially profound given its inability to adequately model real investment behavior with real asset movements.

Distilling this point to its most easily understood point is to suggest that one always ask when confronted with a claim about achieving a certain investment result based on a certain quoted “average” return is whether or not the individual making the claim is referencing the arithmetic or geometric mean when making claims about average returns.

Average Return vs. Geometric Return…Why it Matters

The best way to illustrate why you need to be aware of what “average” is being used to justify investment expectations is with an example:

Assume for a moment that you plan to make a $10,000 annual investment in a passive index fund tracking the S&P500. You plan to do this for the next 10 years and then retire. Consider the two following scenarios unfolding:

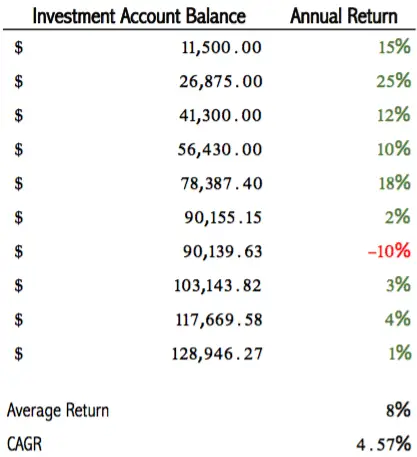

Scenario 1

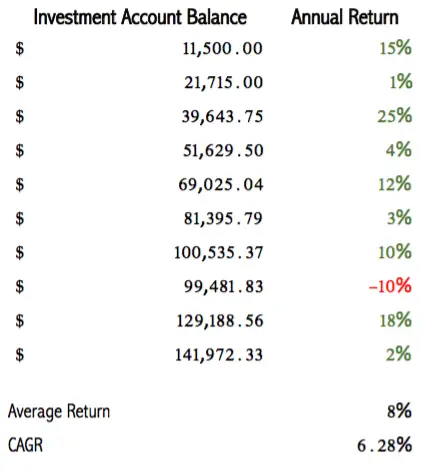

Scenario 2

To the untrained eye, these could just be numbers on a page showing two “different” possibilities for how the stock market could behave over this 10 year period. But look a little closer and you’ll notice that all of the annual returns are identical in both scenarios.

The difference is we simply flip them around. This means the arithmetic mean (average annual rate of return) is the same in both cases–8%. But the balance of the investment account at the end of year 10 varies greatly, by about $53,000 or 41%.

Now look at this scenario where we’ve simply mixed the returns, but have kept all of them throughout the 10 years:

Scenario 3

Again, our average return is identical to scenarios 1 and 2, but our ending account balance is again different. We usually explain this result as the difference between arithmetic means and geometric means, and that is a correct explanation. But that explanation is also somewhat esoteric and practically useless to the average American just looking to save some money for retirement.

I’d like to instead note that this phenomenon is a function of sequence of returns risk applied to your accumulation years.

Think of it like this, the only difference between scenarios 1 and 2 is when the returns took place. The reason scenario 2 ends with substantially more money is because you were lucky enough to have the better performing years occur when you had more money. When your account balance is small, returns of any size are less impactful. But once the account grows large, returns start to become much more significant.

A 10% gain on $10,000 nets you $1,000. The same 10% gain on $500,000 nets you $50,000.

It’s also critically important to realize that we don’t need sharply negative returns to end up with mediocre results. In scenario 1 the average return is 8%. The average return for the good years 16% and 0 for the bad years. Our actual return, however (geometric mean) is 4.57% per year (most people would identify that as horrible as far as stock market returns are concerned).

When You Get In and Out Matters, but Not Like You Think It Does

Timing does matter when it comes to investment returns and your actual results, but not in the sense that you need to time the market. Truth is, there’s nothing you can do about the sequence of returns–either during accumulation or spend down. But you can try to fight off the impact it ultimately has on you.

The key weapon against sequence of returns is diversification, but we need to be very clear that this is not diversification in the sense that it is generally discussed among investment advisors/sales people.

Diversification is both a concept about actual investments chosen and strategy.

The first notion is somewhat easy to capture today, the second is a tad more complex and will be a subject for another day. Put simply, diversification of assets in your portfolio is about more than just buying equity-focused mutual funds of varying objective and market cap. It’s also about a lot more than simply mixing in some bond funds with your equity heavy portfolio.

It’s about owning assets that are entirely different than what your investment guy can sell you.

Now, this is a website dedicated to advancing knowledge on the topic of using specialized forms of life insurance as an asset for the purpose of wealth creation and future income goals. Yes life insurance could be one asset used in the sense of diversification in the sense we are discussing it today. However, it is by no means the only option.

Real estate, certain commodities, small businesses, cash equivalents, annuities (non-variable in this case), lending instruments, and certain less liquid tangible goods (think fine art) are all possibilities with varying degrees of higher or lower benefit for accomplishing the diversification goal.

In the coming weeks, we’ll be discussing this topic in the sense of strategy diversification and how certain life insurance products can help minimize sequence of returns headaches as well as provide certain opportunity to you, so stay tuned for that.