Whole life insurance and universal life insurance are both known as permanent life insurance products. For most people that understanding is good enough, but by design there is something that must be done to make the policy permanent, and the design feature that makes these products permanent is the policy reserve.

They Overcharge to Undercharge

Most people intuitively understand the general concept behind a reserve. Those who have an elementary understanding of level term insurance have no doubt run into the idea that the insurance company overcharges for the cost of insuring your life for the first several years and then undercharges you after a while.

This same basic principle is in play with cash value life insurance, only in a much larger capacity.

Life Insurance is Life Insurance is Life Insurance

I’ve stated it before, and I do it again, here. There is no difference in the cost of insuring a life from one product to another. The probability of your dying doesn’t change because you opted for whole life insurance vs. universal life insurance vs. term insurance.

Therefore, it should come as no surprise to hear that the true actuarial cost of insuring your life is identical across policies. So, if the premium for whole life insurance is substantially larger than 20 year level term insurance, it’s pretty obvious that there’s a lot of extra money coming in to the insurance company when you opt for whole life insurance. What do they do with it?

If we were to believe those who campaign against permanent life insurance, we’d accept the suggestion that life insurance executives use that money to set up their posh office suites.

But it’s a bit more complicated than that—and a bit less fun for the executives. Most of that extra money (in fact all of that extra money) goes into the policy’s reserve.

So what Exactly is the Reserve

The reserve is a cash position that is intended to grow to eventually cover the death benefit in its entirety by some age (usually age 120 for today’s products, i.e. those issued under the 2001 Commissioner’s Standard and Ordinary Tables).

The process is a tad more complicated than it may appear at first glance. If we think about it simply as a level death benefit situation, we can go back to a really old graphical depiction of the endowment process for whole life insurance to geometrically explain what’s going on rather succinctly:

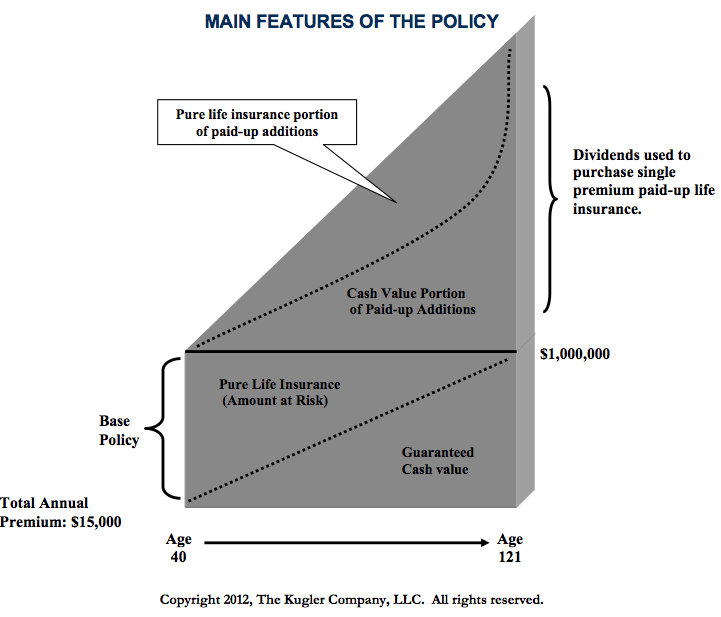

This depiction helps ensure a basic understanding, once we add the nuance of an increasing death benefit on the policy, things become a tad more complicated as the target (where we want the cash to eventually end up) moves and the calculations become much trickier. And here’s a graphical depiction of that situation when we’re talking whole life insurance using paid-up additions (PS: I took this from Frank Rainaldi’s Kugler System, a great resource for various subjects in life insurance)

I say all of this to point out one simple fact. The target the life insurer places for cash accumulation through the reserve will always be the total death benefit of the policy. That will always be where the insurer is trying to get (at the very least) with your money. There is some nuance to this when it comes to whole life insurance blending, mostly that the insurer may not be thinking of it quite in the same terms, but I assure you that as long as you are there is no problem (a future post coming in a few weeks will explain exactly what I mean by this).

Can Level Term Life Insurance have a Reserve?

The answer is yes. Though there is no non-forfeiture benefit so the insurer does not share the reserve with you the policy owner in the form of cash surrender value (outside of a return of premium for unearned premiums, e.g. annually paid premium where the insured dies before the end of the policy year—premiums can only be booked by the insurer on a monthly as-earned basis).

The same principles apply here, only the target is not the death benefit, since the policy’s level premiums has a much shorter duration. In this case, the insurer is targeting an expected value given the age of the insured and his or her risk classification for the time that the premium will be level.

The Big Takeaway

The fundamental design of level premium life insurance products, has a rather dedicated goal to accumulate cash through the process of building a policy reserve. For policies with non-forfeiture benefits (i.e. cash surrender value) this fact plays very well in the policy-owner’s favor as the insurer is seeking to build cash values that one day meets the insured’s death benefit. This places incentives for both policy-owner and insurance company in the same camp and let’s each party work well with one another.