One of the long-standing criticisms regarding whole life insurance is that fact that distributions are often made through policy loans, which bear interest. The common discussion goes something like, “and you can’t even have your money; instead the insurance company makes you borrow it so they can charge you interest on your money.”

One of the long-standing criticisms regarding whole life insurance is that fact that distributions are often made through policy loans, which bear interest. The common discussion goes something like, “and you can’t even have your money; instead the insurance company makes you borrow it so they can charge you interest on your money.”

I’ve always found it fascinating that people bring this topic up as a way to rail against whole life insurance. In large part because it’s only about 25% true, but more so because it’s either an intentional or ignorant (intentionally ignorant) way to keep your eyes focused on the magic while the truth is in operation behind the scenes to make the magic happen.

Still though, I did say 25% true and I do mean that. And to give credit where credit is due, the nay-sayers at least got part of it right, and often times they know that one quarter of the argument better than licensed agents do.

Do you have to Borrow?

Let’s go back to basics for a minute and talk about standard non-participating (i.e. sans dividends) whole life insurance. The cash accumulation component to a non-participating whole life policy is identical to the functioning of the guaranteed component to a participating policy. The cash accumulation is based on a guaranteed rate and will endow at the initial death benefit once the policy matures. This is all guaranteed.

And to ensure that you, the policyholder, don’t ruin this guarantee, the insurance company isn’t going to let you run off with a portion of the money prior to maturity. Instead, they’ll let you pledge it as collateral for a loan. The only other way to get the money is to surrender the policy.

As I noted above, the guaranteed component to a participating whole life policy works identically. To access that money, one would need to take a loan, or surrender the whole policy. No other options exist.

I should note as an aside that none of this applies to universal life insurance as one can surrender money from those contracts to their hearts content. Universal life insurance has no rigid distinction between what is guaranteed cash and what is non-guaranteed cash when it comes to accessing money, so one can choose to surrender to borrow money however they wish.

But before the Anti Whole Life people get too Excited…

So the anti-whole life people are correct? Whole life insurance is a con that makes me pay interest to an insurance company if I want my money? Not quite.

As I’ve stated before the guarantees aren’t all that special when it comes to whole life insurance when we’re focusing on cash value accumulation. There are some agents who will beat the guaranteed stuff into your head non-stop, but I prescribe to a different view.

Remember when we talk about whole life insurance for the purpose of asset allocation, we’re specifically interested in the heavy use of paid-up additions, and the cash value of a paid up addition can be surrendered at any time for any reason—no loan required.

Let’s not also forget that the participating feature is crucial. If it weren’t for dividends, whole life insurance wouldn’t be worth our time. Those dividends purchase paid-up additions as well, and those paid-up additions can be surrendered to access cash without a loan.

In other words, the cash in a whole life policy that is created by a paid-up addition can be surrendered from the policy (i.e. taken out as cash) without having to surrender the whole policy or taking a loan. The original policy stays intact and you need not pay anyone any interest.

But there is more to this

Often times you’ll want to pay the Interest

The fact that money is accessed through a policy loan where, yes, you pay interest is more a function of necessity in accomplishing a larger goal. The concept is similar to using other assets to secure a loan. And the practice of using assets to generate available non-taxable cash whereby secured lending is very well established. Only difference being that there’s no loan application, rigid repayment requirement, or credit consequences.

But let’s remember how distributions work in a life insurance policy, and a few other mechanics that may make loans more attractive.

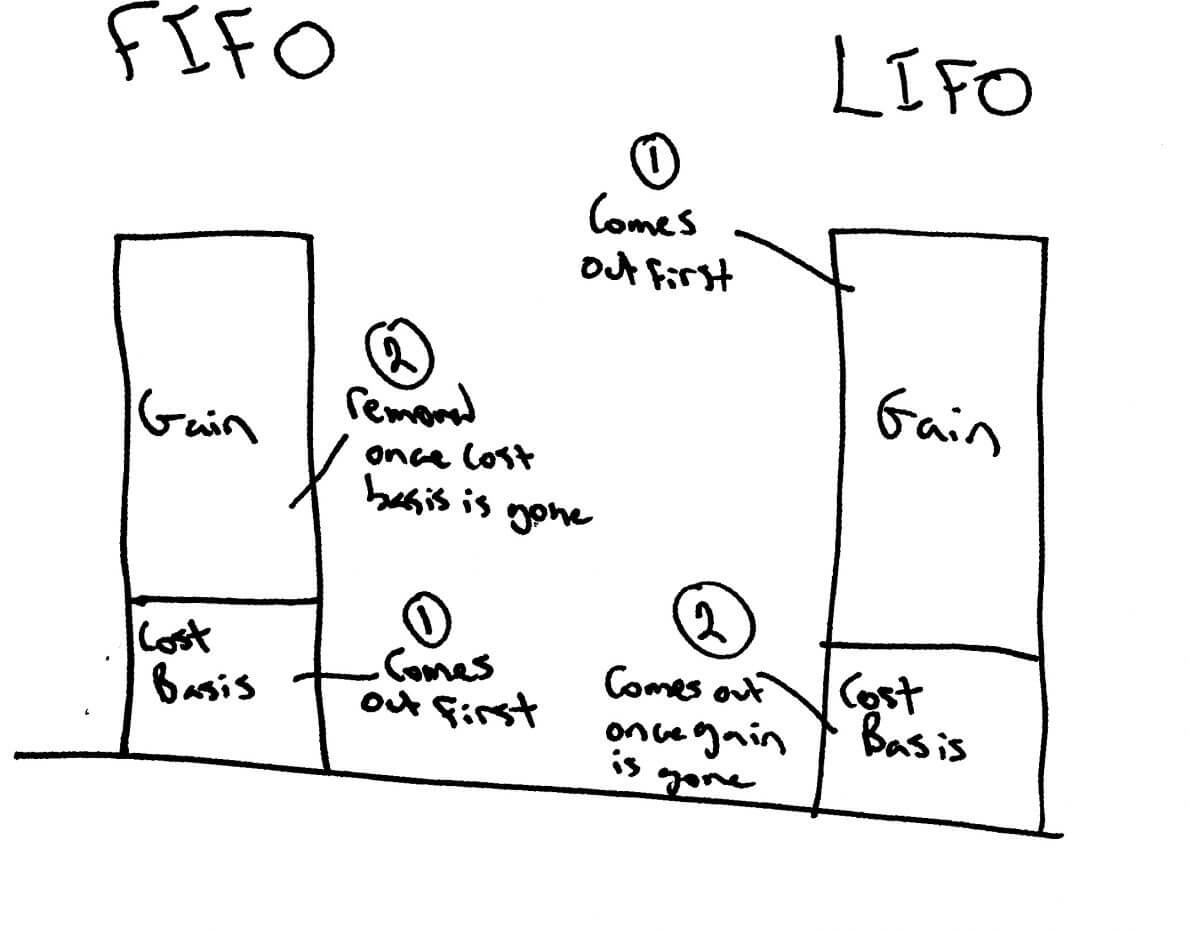

First in First out

Remember that life insurance benefits from the first-in first-out or FIFO accounting method for distributions. This means that all of your cost basis can be withdrawn before you must take out any taxable gain in the policy.

Once the basis is gone, any further withdrawals would require the policy owner to recognize the withdrawal as taxable income, upon which he or she would need to pay ordinary income taxes.

In order to keep the distributions from a life insurance policy tax free, the current standard operating procedure is to use policy loans to access policy gain because loans are not recognized as income and therefore have no taxable implication.

What happens when you take a Loan…

The thing to keep in mind is that when a policy loan is outstanding on a life insurance contract, the money that acts as collateral doesn’t go anywhere. It remains in the policy with all of the money that isn’t acting as collateral as the loan.

So to make a minor correction on the old “they make you pay interest on your money” bit, no you are simply paying interest on the money that the insurance company lent you, your money didn’t go anywhere. And it’s this fact—that it doesn’t go anywhere—that has some useful applications from a strategic point of view.

Since the money stays put, it continues to earn guaranteed interest and dividends—yes even the amount that is backing the loan. And regardless of the dividend recognition method used by the insurer this will be universally true.

So while the loan may grow each year if you don’t pay the interest—and most people who are taking withdrawals from a life insurance policy for income purposes aren’t usually paying interest—so too will the cash surrender value as it continues to grow at the guaranteed rate and earn dividends. In fact, it’s because of this fact that the cash surrender value tends to outpace the growth of the loan by a pretty sizable margin for most years.

Let’s think about this for a few minutes. Yes they charge you interest, but it’s on their money not yours and they are still willing to pay you money on the money that you’ve pledged as collateral, in fact in many cases more money than they receive in interest.

Well now it doesn’t Sound so Bad

Whole life insurance and universal life insurance work. They work for death benefit purposes and for cash accumulation purposes; if they didn’t the products simply wouldn’t exist. Any suggestion otherwise such as the claim that it’s only bought because insurance salesmen build the demand for it gives way too much credit to the average life insurance agent…way too much. Loans are not used to screw honest hard working American’s out of their money they are a viable tool used to accomplish a goal.

It’s easy to get lost in semantics and focus on the wrong thing. There are those who don’t understand and there are those who choose not to understand. There are plenty of good reasons not to opt for whole life insurance—its certainly not a magic bullet—but complaining about interest on policy loans simply isn’t one of them.

Excellent post Brandon,

If I understand you correctly, you saying borrowing from your own policy can be seen as a sort of arbitrage loan – borrowing at say 6% while earning 8% (note: these numbers were pulled from thin air for demonstration purposes) – IF dividends outpace the loan amount.

The other big takeaway I see is that a participating policy is crucial. Is there ever a reason to consider a non-participating policy other than it would be better than no policy?

Andy

Hi Andy,

Yes the arbitrage is possible, your example (completely hypothetical I understand) might be a tad extreme as the spread it unlikely to remain that far apart, but it certainly works.

Non-par can be looked at for permanent death benefit when there are no other options. I’m not sure I know of a situation where that would be reality, but that would be the only application. It should never be looked at or considered for cash accumulation purposes.