Podcast: Play in new window | Download

In today's episode of the Financial Procast we're talking about the Guggenheim group getting sued–kind of, ETF portfolios lag traditional mutual fund portfolios, retirement savings tax breaks may be cut for high earners and myRA's gonna save us all.

Guggenheim Partners Gets Sued for Racketeering

On February 11, a lawsuit implicating Guggenheim Partners, LLC and three of the life insurance companies it owns was filed in federal court. The complaint was filed by Clarice Whitmore and Helga Maria Schutski and included 105 pages (most of which I read).

The complaint details how Guggenheim began acquiring distressed life insurance companies back in 2006 including Wellmark (now called Guggenheim Life), Security Benefit Life, and Equitrust. None of the companies were insolvent but all three were certainly under pressure to “right the ship” with very thin surplus ratios etc.

Without diving off too deep–lets focus on the 30,000 foot view of this case. If you'd like to read it, here's the entire case:

Whitmore and Schulski v. Guggenheim Partners, LLC

The summary of allegations is that basically Guggenheim (a private equity firm) bought these life insurance companies, developed “to good to be true” products to inflate sales, and has designed an elaborately complex accounting scheme to systematically loot these life insurance companies of the cash.

Hmmm…I seem to remember a couple of guys voicing their concern about private equity getting into the life insurance business. Wonder what ever happened to them?

I should also mention that the case was withdrawn the same day it was filed. We're not sure exactly why but our guess is that there's some maneuvering going on by the plaintiffs' attorneys to file it in a different court.

We'll keep you posted as we learn more.

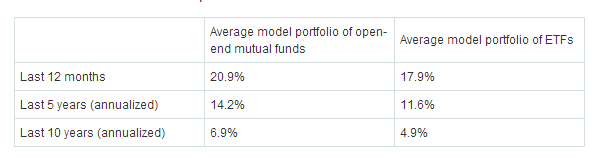

Hulbert Says ETFs Lag Mutual Funds

In a story released last week by MartketWatch, Mark Hulbert of the Hulbert Digest released some data that shows us model ETF portfolios are lagging similar portfolios of open-end mutual funds.

I thought ETFs were the way everyone should be investing in the market? They're cheaper, they can be traded intraday, and most of them are passive, that is that they are based on a particular index.

So why aren't they doing so well? Hulbert says, “I can only speculate, but my best guess is that ETFs' advantages are encouraging counterproductive behavior. Their low cost, coupled with the ability to get into and out of them at any time during the day, as well as the ability to sell them short, have seduced advisers into trading too often”

The President Would Like to Cut More Tax Breaks

Yes you read that correctly. President Obama is expected to present his 2015 fiscal budget to Congress and as part of that budget he's going to ask them to reduce some of the tax breaks that high income earners get for participating in employer-sponsored retirement plans.

In fact, he would like to limit the value of all tax deductions that are defined as defined contribution exclusions and deductions to 28% of total income. The estimates are that this would bring in an additional $1 billion a year of new tax revenue.

According to a story at Pension & Investments, “Based on current tax brackets, the 28% limit would reduce the tax advantages of retirement savings for people earning more than $183,000 or couples earning more than $225,000. The overall cap for all tax-preferred retirement accounts would limit them to providing an annual retirement income of $205,000, which would currently cap tax-preferred accounts at $3.4 million, but could go lower as interest rates rise.

It's not likely that this will make it through Congress but it certainly gives you another opportunity to gain perspective into the future of tax policy in the United States. Hint: It's not likely to get better.

myRA's Gonna Save Us All

No, probably not but it's fun to talk about. In case you haven't heard about it, the myRA was introduced to the country during the President's State of the Union address back in January.

According to what we've found, the myRA is “targeted at the millions of low and middle income Americans who don't have access to employer-sponsored retirement plans. That includes roughly half of all workers and 75% of part-time workers.”

Employers will not be required to offer the program…yet. It's not supposed to cost employers anything to administer nor will they have to contribute to the accounts.

How does it work? It's a Roth IRA that only invests in government savings bonds. Workers can keep the account when they switch jobs and they can contribute to the account from multiple part time jobs. The accounts will also have no fees.

Will it work? Well that depends on how you define “work”. The accounts can be started with as little as $25 and workers can contribute as little as $5 per contribution after that up to $5,000 per year.

When the account reached $15,000 they will have to transfer it to their own Roth IRA elsewhere.

So, I guess you could say it will work functionally, however, it's not likely that this is going to solve any real problems that Americans have with saving for retirement. The problem isn't that low and middle income Americans don't have access to accounts, it's that they don't have any money.

A problem that the myRA can't fix.

Not good news for the insurance industry (regarding Guggenheim).

I would say the annuity industry, and specifically lower rated annuity companies. The Life industry isn’t really involved.

Where is the article you reference above “Hulbert Says ETFs Lag Mutual Funds”, I’m not finding it and this is the first time I’ve seen this statement.

I searched on Marketwatch but it isn’t coming up (it could be me).

Thanks!

Hi Jim,

Here’s the link to the article: http://www.marketwatch.com/story/10-open-end-mutual-funds-to-buy-now-2014-02-12

I had linked the chart in the post back to the wrong article…oops! Thanks for stopping by.